All,

I went ahead and paid the $500 dollars for API credits. Plenty of credits for what I needed.

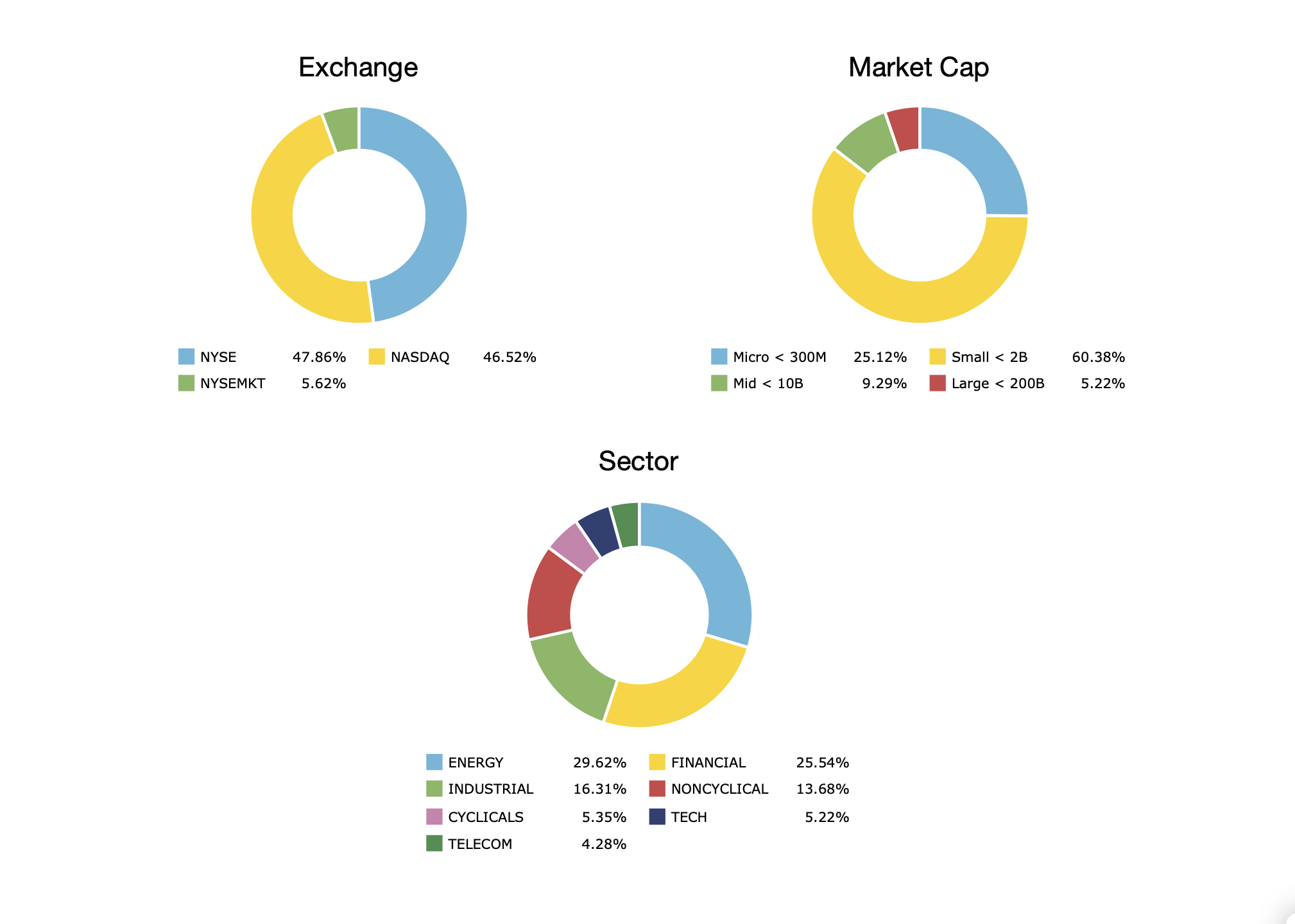

Here is a k-fold validation with an test sample and embargo period of 3 years (pretty aggressive embargo period) comparing recursive feature elimination and no recursive feature elimination. As you can see the results are similar. I have done other analyses.

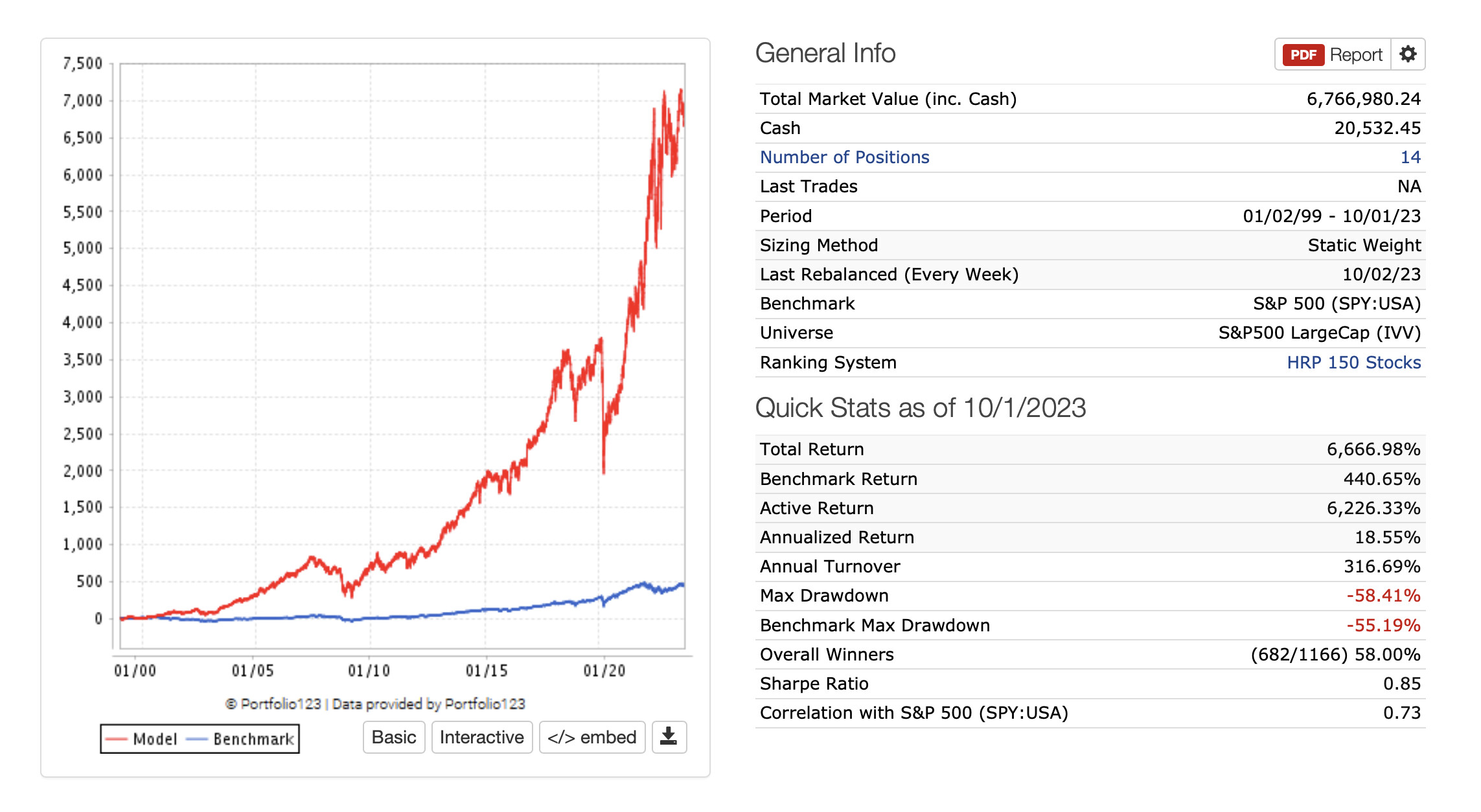

But I did a k-fold validation on all of the data after this with no recursive feature elimination (also no test and embargo period). Here is the backtest with the resulting 20 stock sim (using the purely ML derived ranking system):

Everyone (including me) can discuss, worry and/or speculate about what my out-of-sample results will be.

But here is my first point: I emailed a friend this morning and mentioned to her there is no need for me to discuss this in the forum anymore.

I do not need to make a feature request to do pretty much whatever I want to. And I might add that I am more likely to get a direct answer from ChatGPT than the present P123 forum regarding machine learning.

I will also note that only recently has there been a DataMiner download with accurate forward returns. Maybe a month or two? One could say I could have gotten here earlier but could I have with incorrect future returns? And one could say I should have if I were a better programmer. But the simple fact is I am not that great of a programmer.

It has been a struggle for me to get to this point. But I am pretty much done.

I would not mind daily updates of overnight data with in the DataMiner download but I can actually do that now with the API if I need it.

While I am done essentially, P123 will be starting just now with machine learing. I will add this to something P123 will need to consider with regard to the forum.

And this. There are a lot of machine learners at P123. Few of them bother to post. I have noticed more than a few that come discussing their neural-nets usually. But very quickly stop posting.

I leave this purely as a question that probably someone else will have to answer. As I said, I am now one of those machine learner that pretty much can do it on my own now.

I mean that purely as a positive thing for P123.I am thankful for the data. If I have any motive at all it would be that P123 survives as a business for as long as I am investing with machine learning

I am not claiming to have any answers on marketing or what to do in the forum today. I think I will stop with unsolicited advice at this point. I do not get paid for my advice and as I said, I have what I need.

I will leave that now to those who get paid to answer those questions going forward. My only interest being that it ultimately does work for P123 so I can keep using their services.

Jim