Haven’t been on the site as much lately because I’ve been letting my strategies mostly run on autopilot the last couple years while still trading them, but came across this post.

I know personally I easily spent hundreds of hours coming up with strategies I felt I could comfortably trade which showed promise in rigorous backtesting to yield outperformance relative to index funds. That probably doesn’t include all the research and books I’ve read to understand all the fundamentals. So far it’s working out but perhaps these strategies will be arbitraged out at some point.

I’ll second what has been seconded numerous times already. It is hard to find workable strategies that actually yield outperformance. You have to find this interesting and in a lot of ways it’s like seeking the holy grail. If you just want to make money without lots of effort you aren’t going to like Portfolio123. And also if that’s the case just invest in index funds. There’s already enough people losing money investing in individual stocks who don’t want to put in the actual hard work. People often fail to realize the stock market is a competition between banks, hedge funds, institutions, and other retail investors. Being average is easy. Trying to be better than average more often than not yields below average. Being above average is super hard, but not impossible.

I had a friend who said just give me the 5 minute overview on how to pick stocks. I told him I can’t because to do better than everyone else you need to get beyond what everyone knows. It’s just like everything in life. If you aren’t working harder and smarter at it than most others you won’t do better.

When I get more time I definitely want to examine new ideas and perhaps that will be more pertinent as we enter a new economic regime in the world.

Simply select all the stocks in the market, i.e. index funds. Period. 15 seconds.

So far it’s working out but perhaps these strategies will be arbitraged out at some point.

The speed of technology iteration in this field is far away from that in IT. Even now, good COBOL programmers or C programmers can still get jobs.

Edit:

harder and smarter

"It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent."

Munger himself didn't do that, though, and his investments were heavily speculative, just a free endorsement Buffett used to attract speculative investors.

Because I used to have this thought of "no where to hide" using p123, I thought I'd share some of my recent findings in hopes it can be mutually beneficial.

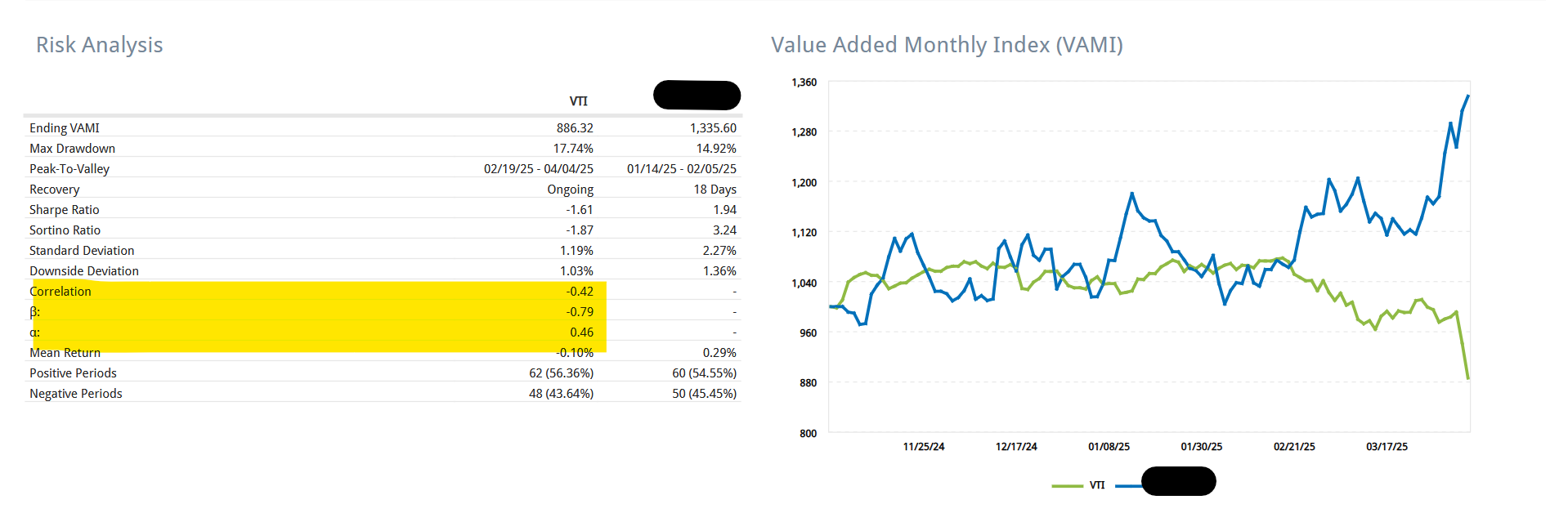

Long/short strategies developed here continue to demonstrate real potential—especially in turbulent markets like the one we're experiencing now. I'm attaching a report from IB to illustrate this potential clearly and to encourage Portfolio123 to continue investing in innovation and in tools that support long/short strategy development.

Broadly speaking, I agree with the sentiment expressed by others here: Portfolio123 must keep innovating aggressively if it’s to remain a platform where users can genuinely outperform. Access to better data, smarter technology, and more sophisticated tools is key. There's bound to be some lucky ones always claiming their secrete sauce is what's generating the out performance. I think the designer models are the best test / evidence of this hypothesis.

On that note, one area that deserves attention is transparency. It would be helpful for the community to know when contributors are affiliated with P123 or compensated for promotion, so all voices can be weighed appropriately. After 10 years here I just became aware that some of the most vocal proponents here are paid by p123. That's not inherently a bad thing, but it should be clear on all posts.

Lastly, I want to revisit the topic of the risk model. We previously heard there might be progress by the end of 2024, but we’re now in Q2 2025—facing one of the sharpest short-term drawdowns in history—and there's been no update. A strong risk model could have made a significant difference in navigating this environment.

Looking forward to any updates the team can share, and hopeful that long/short strategy support / risk model remains a high priority.

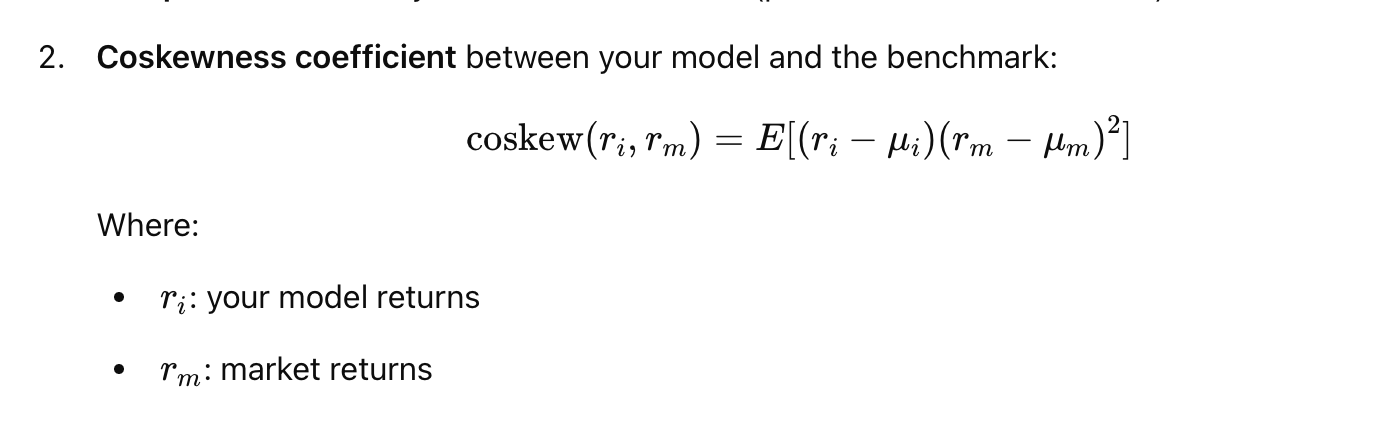

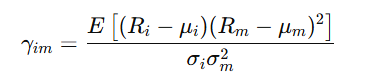

Dedicated Short Bias type hedge funds actually fail, and are significantly worse than market neutral funds even when only alpha is considered. The factors that are efficient in the stock market tend to have negative coskewness, i.e., they underperform in this current situation. For example, BTAL even fell on Friday. The only thing that works in this situation is options or going long the VIX, but they are expensive. Individual strategies may be successful sometimes, but the success or failure of a large number of strategies shows the viability of the direction.

Trend-following strategies may perform well in long-term declines like 2022, but not for short-term plunges like March 2020 and the current one. Market maker type strategies may work in wild swings, but the cost of their infrastructure and expertise is well beyond what retail investors can afford.

That said, I think VIRT is actually being sold off incorrectly. Because it actually benefits rather than suffers from the high volatility environment. I wouldn't touch I,t though. It is too big.

Ongoing with redoing long/short, risk management, risk model, and few other things. We're collaborating with some of the smartest P123 users!

Not sure who you are referring to. Kurtis and Andreas? They were proponents before they started getting paid.

We have the formulas written. We had a delay because we needed ETF constituent data. Still no UX design and formulas have not been translated to our backend language. Some form of MVP by Q3 is my best guess.

I am Kurtis. You can see on my LinkedIn very clearly that I run an independent consultant service and I also use Portfolio123. It has worked very very well for me and the people I consult with including ETFs, family offices, WorldQuant and others. I'm pretty transparent about loving and supporting Portfolio123.

Thanks for sharing this—could you elaborate a bit on how you arrived at that conclusion? I used to think this but it's really just coming to realize that common factors we trade are risk factors as well - like market beta. You get paid for beta but with about 16% annualized volatility and scary drawdowns, like this.

Just to clarify mine: I wasn’t trying to argue, but rather offer a perspective that might help others think differently about the tools we have.

The strategy in question was intended to have an ex-post beta of zero. In practice, due to the absence of a risk model, it ended up with a negative ex-post beta of -0.79. Still, beta only accounts for about 8.98% of the total return (33.56%), so it still leaves substantial excess returns even in this environment.

What I was really hoping to do was highlight that alternative approaches to trading—leveraging some of P123’s capabilities—can be both valid and insightful. Instead of dismissing ideas prematurely, maybe we can focus more on solutions.

Using my model's mean which is pretty good makes it easy for otherwise solid performance to be seen as below average —especially in market rallies. That seems to naturally lead to negative coskewness, even for models with strong performance.

My Omega ratio is positive, which makes sense: Omega isn't penalized by a high mean or median return, and focuses on the gain/loss ratio above a threshold (in this case, the benchmark's mean return).

That said, my model has had a significant drawdown recently, which is important to acknowledge. So while I may question coskewness as a fairness metric for high-alpha models, it is capturing something real about tail risk or participation asymmetry.

I'm just trying to better understand exactly what it's telling me. So far, I think it’s a useful but nuanced diagnostic—especially when interpreted alongside other metrics like Omega and max drawdown.

Happy to learn more including what I am missing about this metric.

Coskewness is meant to measure the optionality embedded in returns, not the overall return-to-risk ratio. Therefore, it is not called “penalizing high average returns”.

Also, its ability to predict performance during rapid short-term declines is not much affected by higher average returns.

Empirically, this captures the significant declines in factor-based market-neutral/beta-neutral strategies in March 2020, currently, or in other similar short-term, rapid declines in history.

Omega and max drawdown

Omega can't distinguish between diversifiable idiosyncratic skewness and less diversifiable (and expensive to hedge) coskewness. MaxDD can't distinguish between short-term declines and long-term declines, and can't capture rapid declines smaller than MaxDD.

nuanced

The key is non-diversifiable, costly tail risk/optionality, and coskewness is one way to measure this risk/cost.

For the rest, you only need to consider simple Sharpe ratios or t-values of alphas/Jensen ratios.

Common metrics are not well suited to capture this.

Edit: Because idiosyncratic skewness can be mitigated by diversifying across multiple strategies.

You can try to include a lot of “(non-diversifiable) tail risk: small” factors.

But it comes at a cost.

Edit: This is because even though many of these factors may not be particularly significant alpha reducers on their own, they dilute many of the other factors for which positive alpha can be obtained.

So this is really helpful—especially for thinking about options (and maybe other tail-risk tools too). If I’m understanding you correctly, it sounds like the kind of options needed to hedge this coskewness exposure would typically be pretty expensive—and probably a bit out of reach for me at this point.

It also seems like this is the kind of risk we often don’t fully appreciate at P123 until it shows up—so this perspective is really helpful for seeing that kind of vulnerability ahead of time.

Yes, because it's non-diversifiable or less diversifiable.

This is the cost of chasing alpha or reducing volatility through diversification in normal times.

out of reach

VIX futures are a simpler way to purchase this insurance.

the kind of risk we often don’t fully appreciate at P123 until it shows up

It's not easy to see, but it's not as completely unforeseeable as the overblown metaphor of the “black swan”.

In fact, Taleb's optimistic bias towards the “new normal” or neoliberalism has led him to insist that a crisis only 25 years after the last major one (72-82) can be likened to some kind of “black swan”.