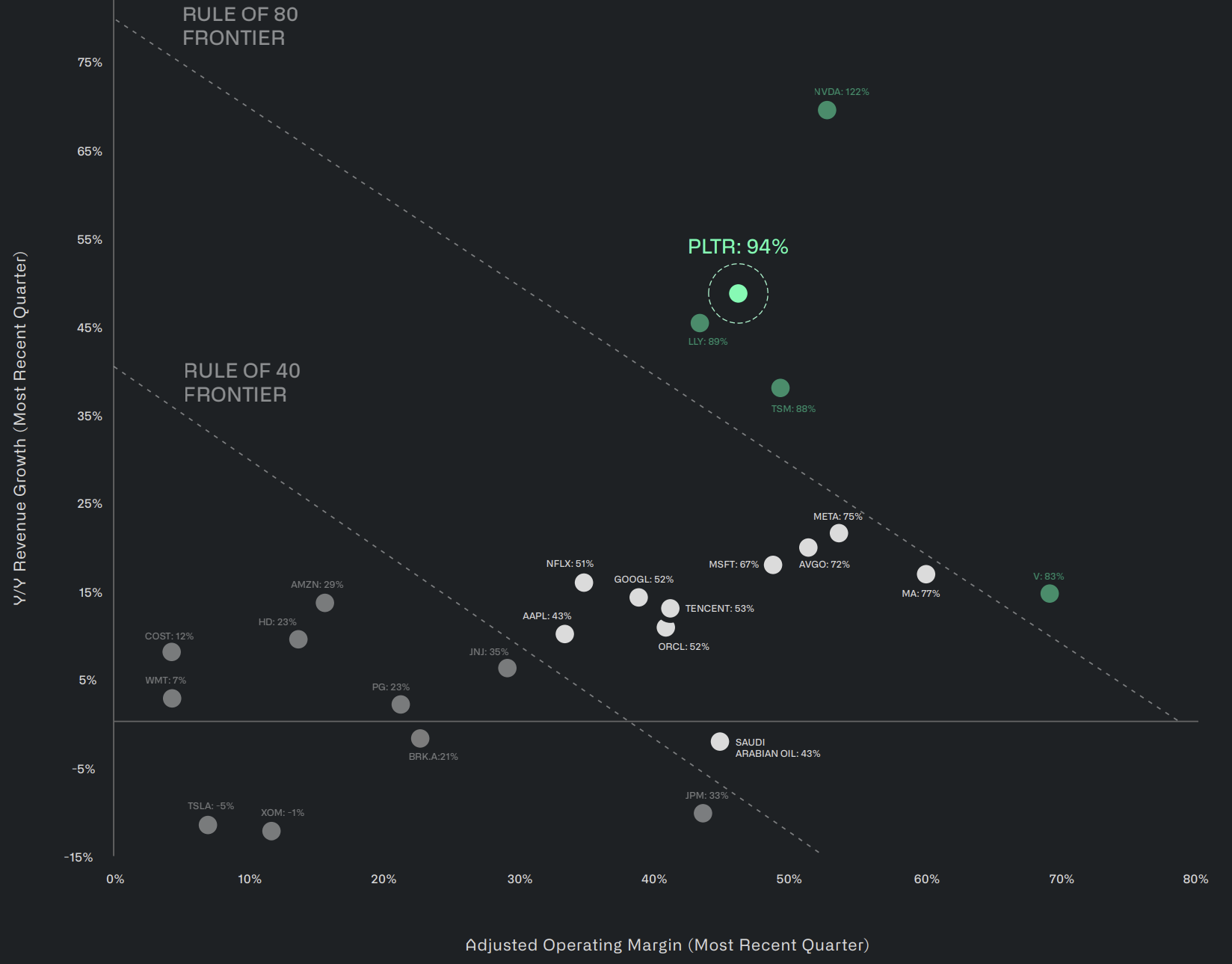

PLTR is making a big deal they have a 94% "Rule of 40" metric. I never heard of it before so I'm investigating if we can calculate it. Rule of 40 just says that a healthy SaaS has a score of 40+ calculated by adding the sales growth and profit margin, plus a mysterious Stock Based Compensation (SBC) related tax.

The figures PLTR are using are in their investor presentation and their filing. They use an adjusted profit margin that adds back SBC expenses to the operating income.

For sales growth they use 48% which we have with SalesGr%PYQ

For the adjusted profit margin they:

Start off with Income from Operations of 269M (which we have with OpIncAftDeprQ)

Add back 160M of SBC (which we have with StkOptCFQ)

Add back 35M for taxes related to SBC (which I can't find anywhere in Factset)

Long story short it feels like they are fidgeting a bit to show an ever increasing "Rule 40" value of 94%. With the data we have we would calculate either

48% + 43% = 91% // using StkOptCFQ of 160M

48% + 39% = 87% // using StkOptExpQ of 126M

Either way a very healthy number assuming the massive dilution they are doing to existing shareholders is inconsequential.

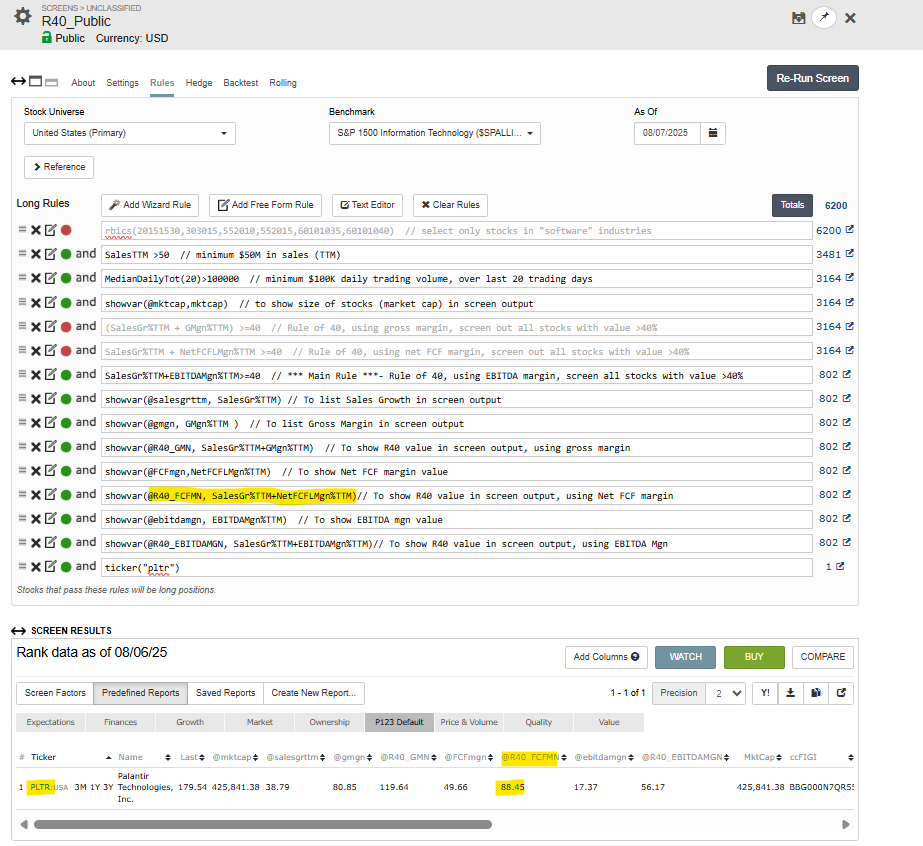

Overall the "Rule of 40" metric seems like a handy metric to add as a built-in. Here's the code you can use to recreate it in the screener.

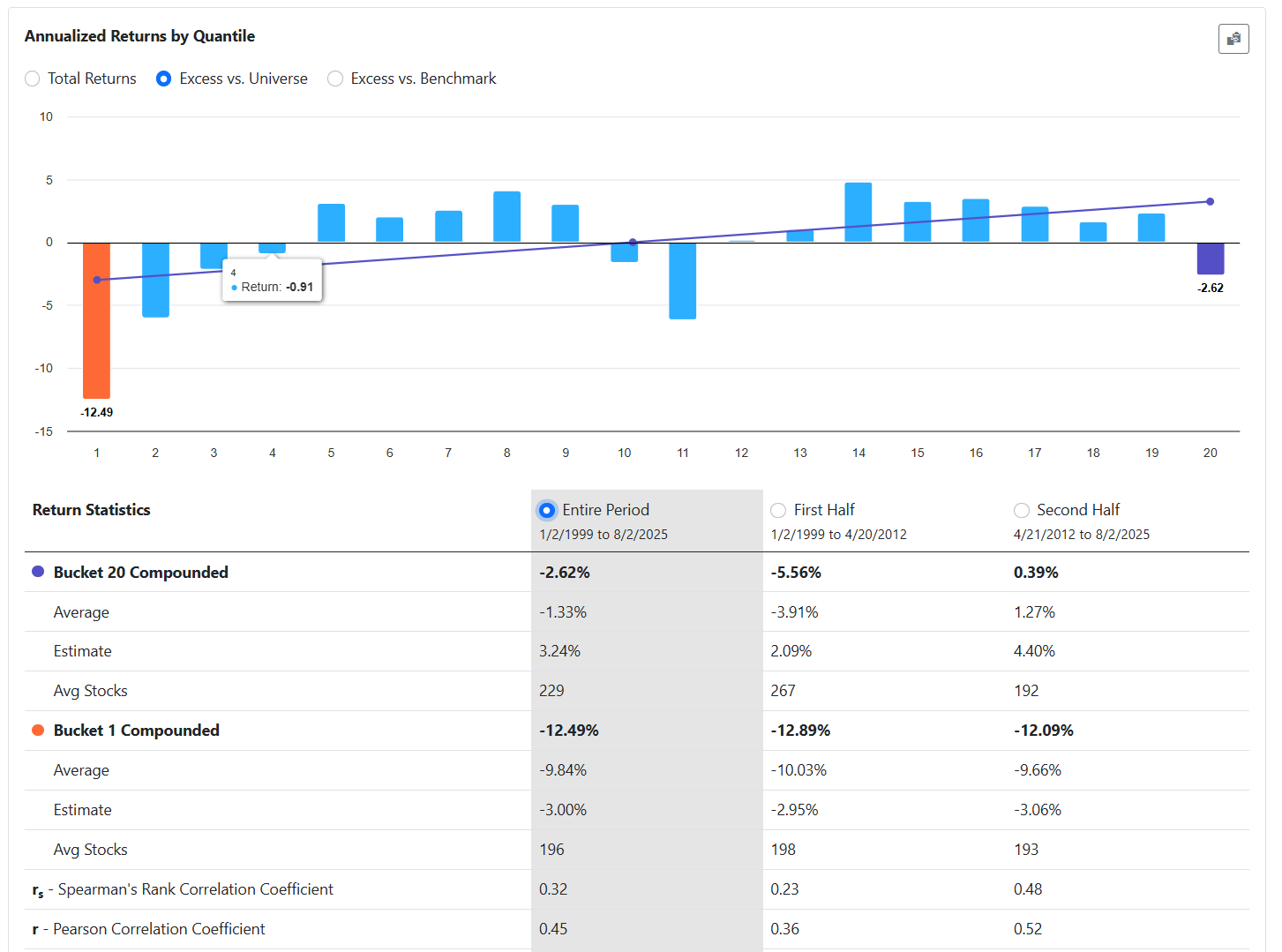

Shows that the rule avoids some companies with very low margins and very low sales growth (lowest two buckets), but that is about it. Being in the top-end is not necessarily a good thing.

It seems like a bad idea to me. Extremely high sales growth is unsustainable, high stock-based compensation is a warning sign, and companies with low profit margins are often poised for earnings growth (in fact, I've seen an inverse correlation between profit margin and future earnings growth).

First of all that is an amazing-looking scatterplot. Secondly, companies have been “adjusting” standard metrics to make themselves look better for a long time. Reminds me of the “Community-adjusted EBITDA” WeWork had before the collapse. Palantir is doing well but excluding employee compensation is a big no no as it is an operating expense. At its core it is just saying good margins and good growth are good but information is lost when you don’t know which is which. 80% growth and 1% margin? 1% growth and 80% margin?

100% agree. Exotic new ways of valuing stocks or measuring their companies' performance are a backdoor way of catering to investors' credulity. Palantir's margin and growth don't justify its stratospheric price. The company can't grow to infinity. The current valuations of some tech stocks and the prevailing discourse remind me of the late 1990s.