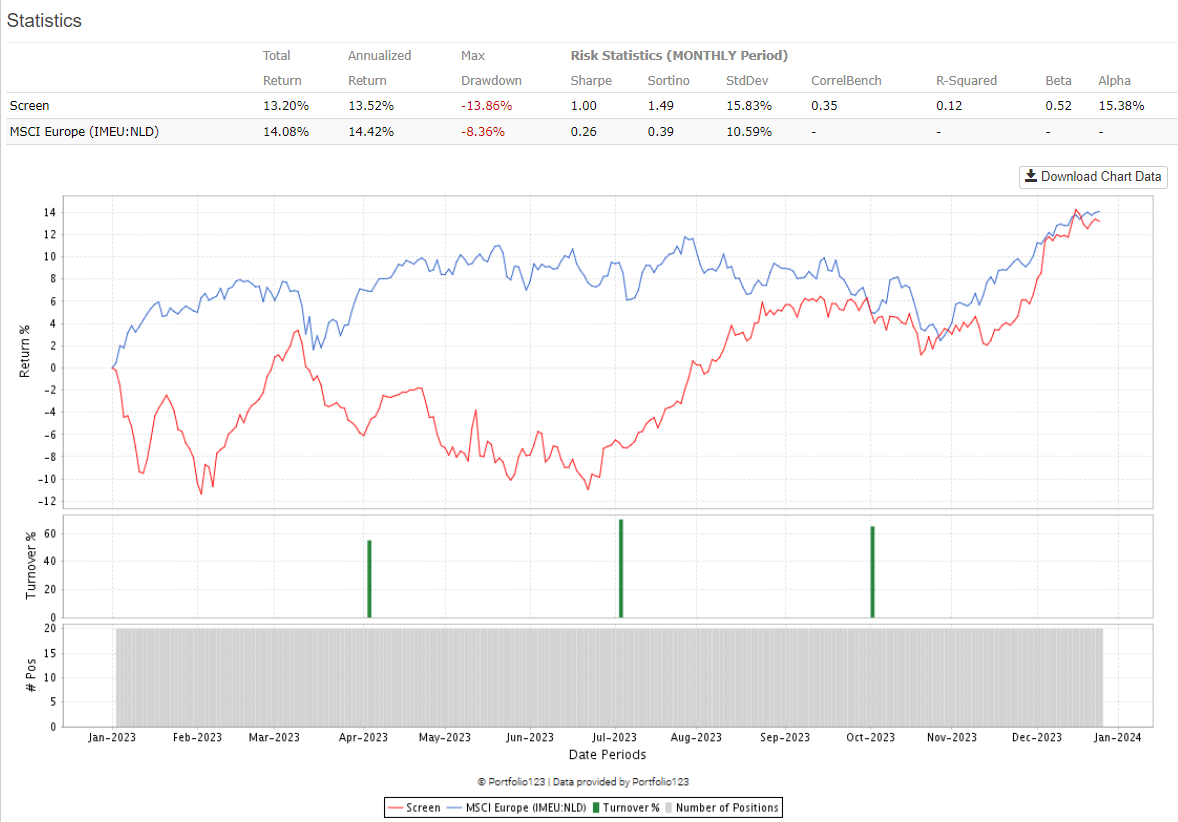

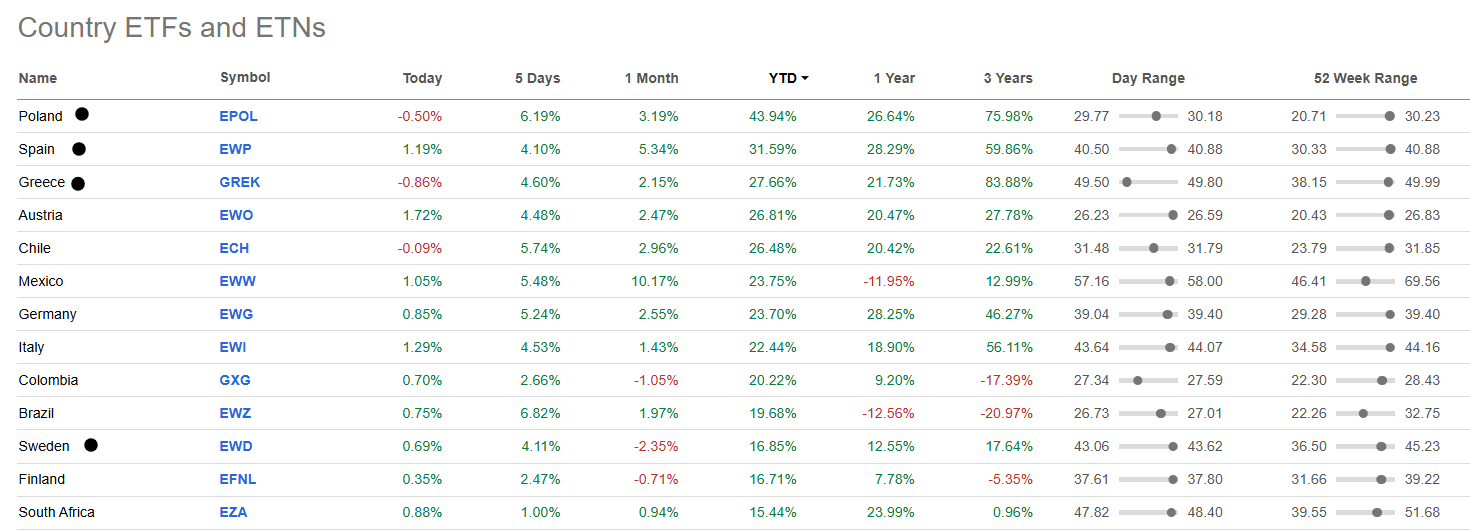

I was interested in the performance of core combination RS for Europe in 2023.

Quarterly rebalance, Easy to Europe Universe, select 20 stocks, currency EUR.

Nothing spectacular as you can see below.

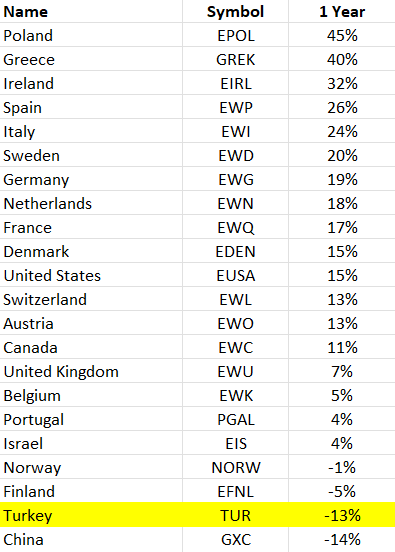

core combination RS for Europe (and possibly most of users RS) was not able to select stocks in the countries that performed best.

43.75% of stocks were selected from the worst country - this is sad. We know that Türkiye has very high inflation, (USDTRY 1-yr return was 57%), maybe this is something we should take into account in creating European RS.

Finally, we would need to diversify equities across the countries, and possibly select most promising countries to invest based on a country rank which would rank countries based on different factors: %gdp growth(higher better), inflation (lower better), median p/e, etc.

I have not tested, but I suspect that if you used a node weighting countries by corruption index you would get a much better result. Or simply don’t invest in the most corrupt countries, can’t really trust the data provided from corrupt countries.

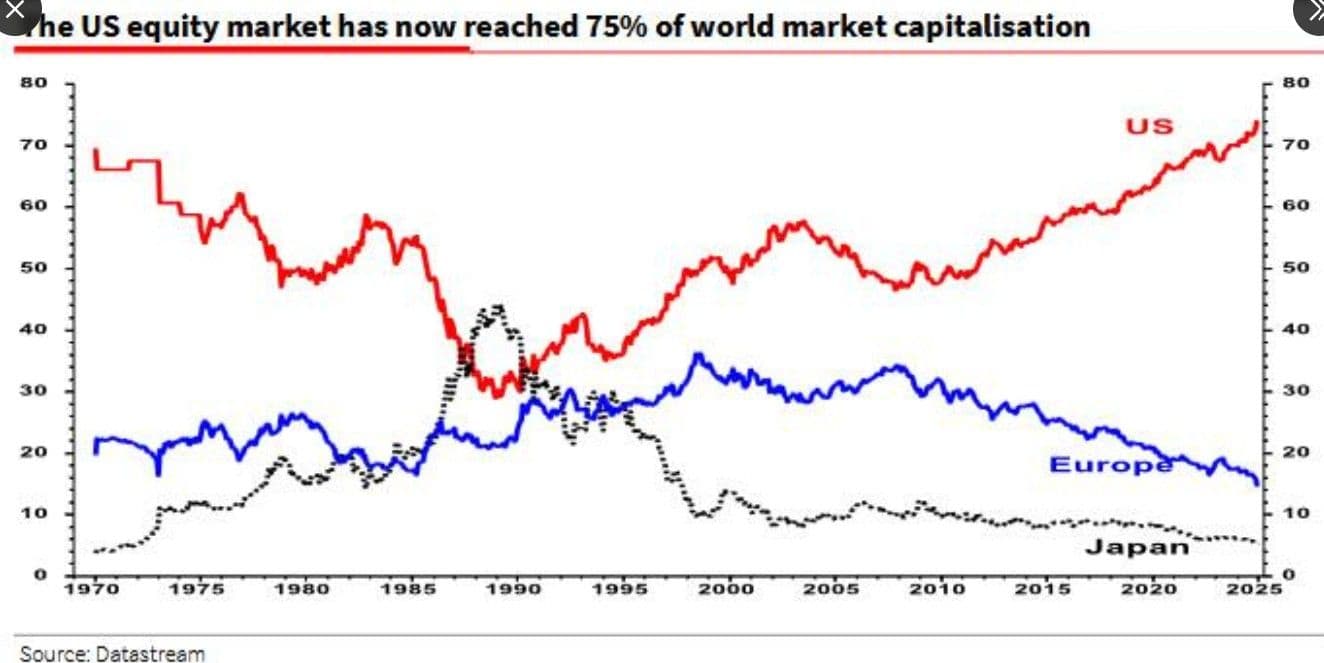

Using market capitalization-based ratios as a proxy for valuation is far from ideal. If all European companies were to list on U.S. exchanges tomorrow, it wouldn’t suddenly render the U.S. market more overvalued.

The real question is whether U.S.-listed companies can sustain higher EPS growth going forward. Applying a simple Gordon growth model with trailing PE for the U.S. and Europe and assuming a fixed equity risk premium suggests that implied growth rates in the U.S. are about 2% higher than in Europe. This is in line with the last 20 years of earnings data, which shows that European earnings, when adjusted for inflation, have barely grown.

While I agree that the pessimism around European companies' growth prospects is overdone, and some realignment of valuations is likely, I believe the scale of this adjustment will be more modest than most think.

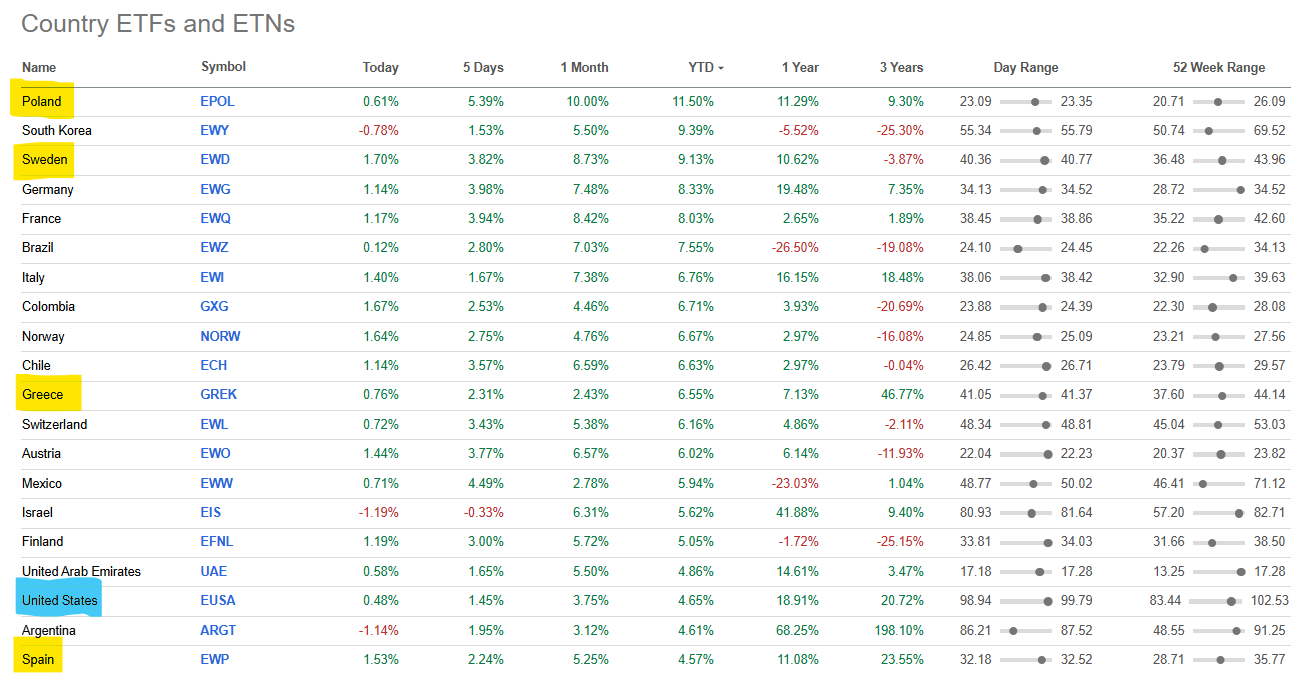

One factor contributing to this is also strengthening SEK and PLN vs USD.

Unfortunately in Poland, most of the rally is contributed to large caps.

There are two upside risk in Poland:

Presidential election in May (based on polls the candidate backed by current government will win which would accelerate socioeconomic reforms)

End of war in Ukraine - well ... many scenarios but most are positive for stocks valuations in frontline countries.

Users from Sweden may add more to the situation in their country.

In addition, some interesting development should be expected in Germany ahead of elections in month.

These models don't really make much sense. What is really meaningful is what the quant models tell us about the relative expected return differences (after deducting the overfitting component). And that's very small.

Otherwise, it would be too easy for people to get rich by trading futures.

The real rationale for diversification is to hedge the risk of factor returns in different countries or to take advantage of the greater predictability of foreign markets. The impediments are the cost of compliance, the cost of taxation and the cost of trading.

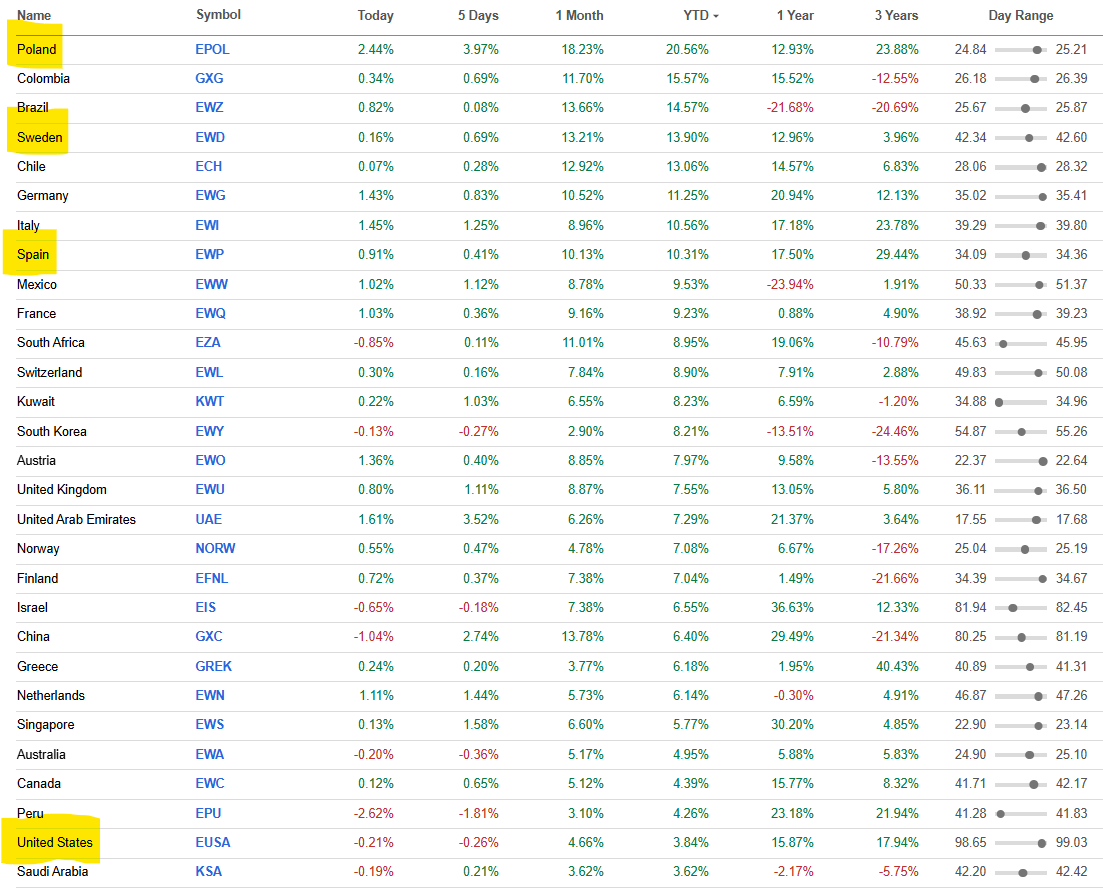

The European Commission on Wednesday proposed a 2 trillion euro ($2.31 trillion) EU budget for 2028 to 2034, with a new emphasis on economic competitiveness and defence and plans to overhaul traditional spending on farming and regional development.[Reuters]

Watch closely which countries will be Net Beneficiaries (in relation to GDP) for the budget 2028-2034.

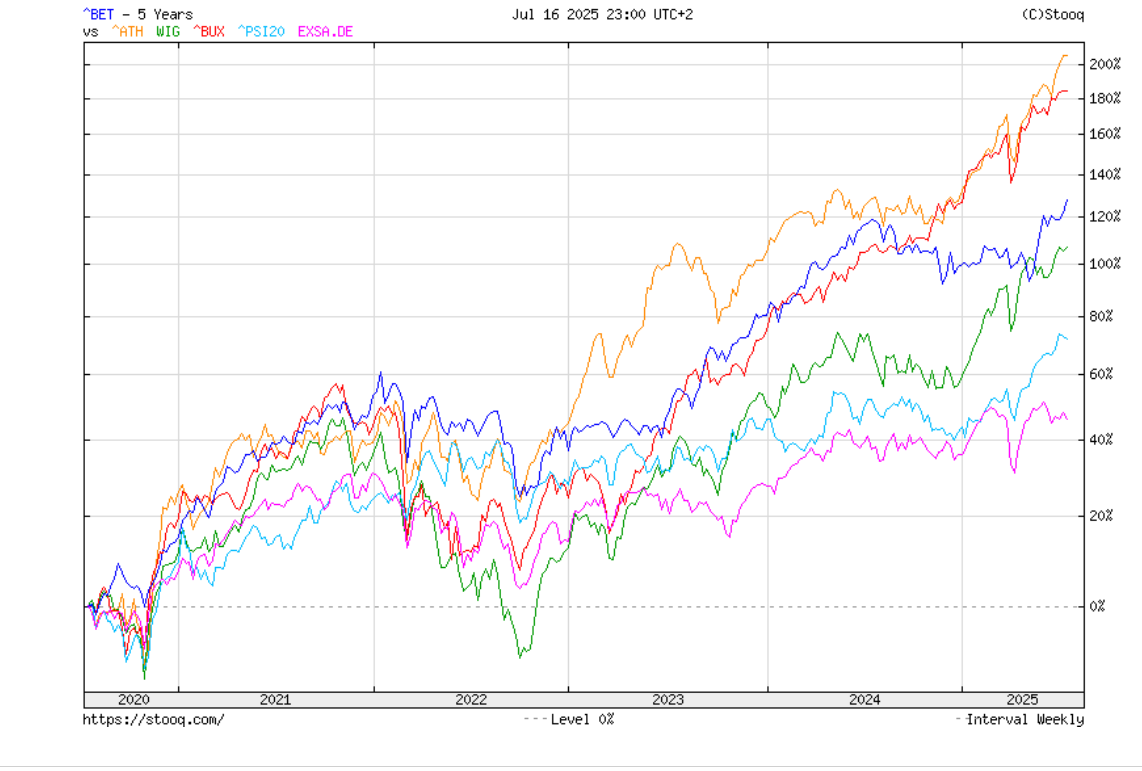

Top 5 Net Beneficiaries (nominal) for the budget 2021-2027.

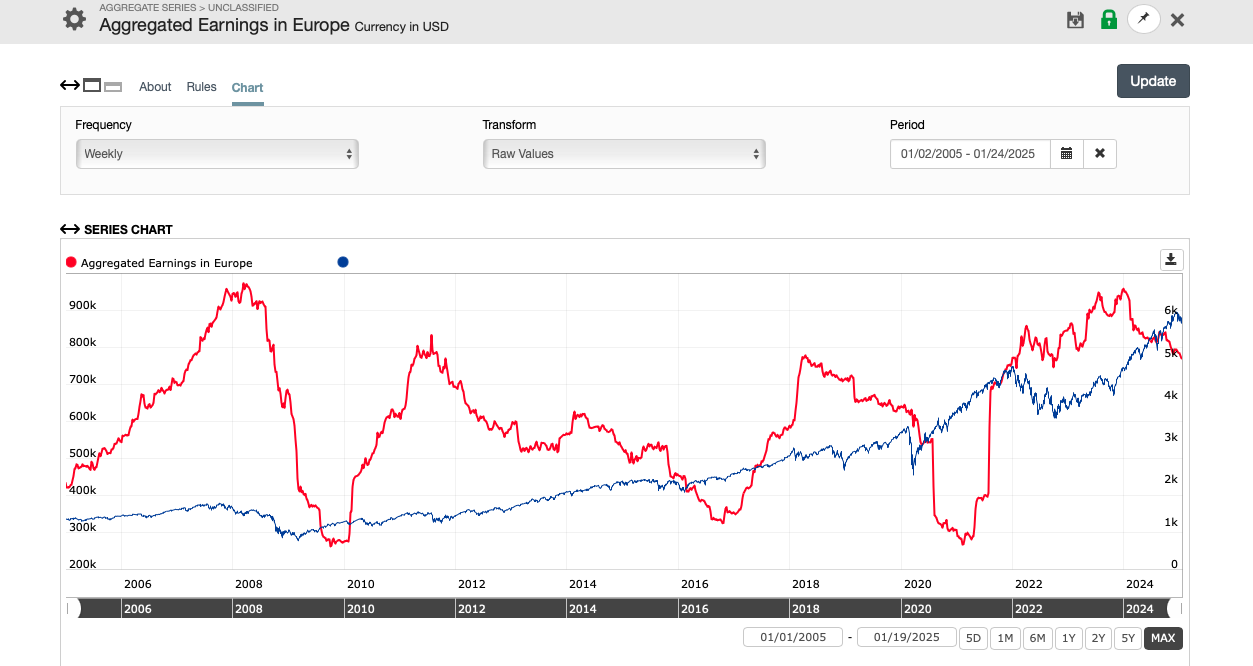

Stock performance of top 5 Net Beneficiaries (nominal) for the budget 2021-2027.

Benchmark: EXSA iShares STOXX Europe 600 UCITS in EUR.

Other countries in local currency.