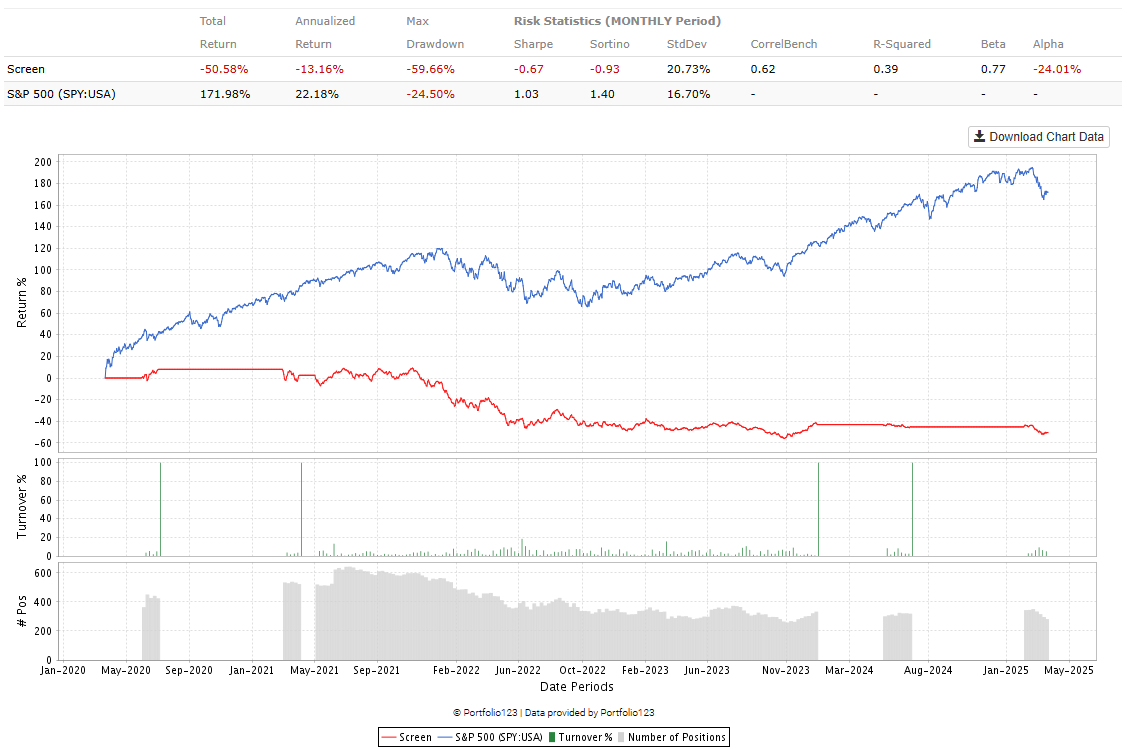

Over the last 5 years, backtests suggest a sharp underperformance of high price-to-sales (P/S) stocks—specifically, those with P/S ratios above 8—when inflation expectations exceed 3.2% (as measured by the University of Michigan). Over the past year, this cohort declined by about 50.58%, compared to a 1.73% gain for the broader Russell 3000.

Screener (R3000):

close(0,##INFLEXP)>3.2

Pr2SalesQ>8

Why Does This Happen?

- Discount Rate Effects: In high-inflation regimes, the required rate of return (discount rate) typically rises. For high-P/S stocks with distant cash flows, a higher discount rate can drastically reduce present value.

- Repricing of Growth Assumptions: Elevated inflation often reduces real economic growth. Investors become skeptical of aggressive revenue projections, prompting a “rerating” to lower multiples.

Notable High Price to Sales Mega Cap Stocks

NVDA, MSFT, AVGO, LLY, TSLA, NFLX, PLTR

Current Positioning

Given that tariffs and supply-chain bottlenecks could further drive up inflation, a defensive stance (e.g., holding more in cash at short-term Treasuries with ~5% yield) helps preserve capital while earning a modest return. Historically, once inflation peaks and begins a sustained decline—often signaled by lower CPI prints or downward revisions in University of Michigan expectations—equity markets tend to rebound quickly as the discount rate normalizes and investor sentiment improves.

Conclusion

The data underscores the sensitivity of high-valuation stocks to rising inflation expectations. While staying in cash or short-duration Treasuries may seem conservative, it can be a strategic move until inflationary pressures abate. As soon as inflation trends lower, expect a faster reversion to higher equity valuations, especially for growth-oriented stocks whose future cash flows become more attractive once the discount rate recedes.