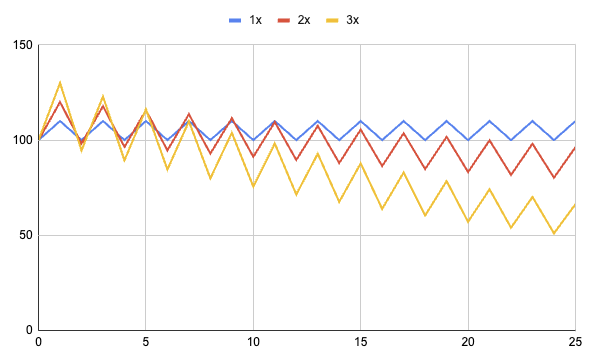

You are not wrong in thinking this could be a good idea given the results but I would advise you to stay away from 3x levered ETFs. 2x is much more palatable, but 3x gives too much away to drawdowns (“volatility decay”). Keep in mind small caps have done famously bad in recent times so a future time outlook might perform differently too. This is coming from someone who has used 2x etfs and 3x for years in his personal accounts and used to manage 2 levered etfs so I have nothing against them per se. Try repeating your test with a 2x ETF and a bigger position size to account for that and you might see a boost.

Thats funny, so you think the backtests of TZA on p123 are flawed? My thinking is that frequent rebalancing mitigates the effect of volatility decay. Its shannon's demon in action.

When you think about it a portfolio of puts is much worse, when the market stays flat it loses all its value. TZA doesn't.

I think you could boost the returns even more by reducing the “decay” and transaction costs by switching to a 2x ETF. About the performance/backtest, it is not about wrong or flawed or right but past vs future. You only get one throw of the die in real life so it better be good.

TZA has lost all its value. Its return since inception (11/08) is -100%. Its five-year return is -93%, which is pretty close. It's a vehicle of doom.

The issue with a 2xinverse ETF instead of TZA is that increasing the hedge to maintain the same level of protection also requires allocating more capital to it, which reduces the capital available for the long system — ultimately weakening the overall performance. (I tested this.)

The only valid counterargument would be if the Russell 2000 had been significantly overvalued for the past 25 years and only recently became deeply undervalued. But that’s not the case. Even if it were, such a pattern should have shown up in the 2000–2007 period — yet that timeframe was actually very strong for the hedged portfolio in my simulation.

If you have a short system using puts that performed well during that period, by all means, use it — I just don’t have one. ![]()

I assumed you had a margin account. If you only have a cash one it is different. Basically 2x inverse ETFs tend to track 2x performance somewhat closely while 3x ones tend to lag behind 3x performance so usually you leave some gains on the table for the given level of risk. If you compare 2x nasdaq 100 vs 3x nasdaq 100 (qld vs tqqq) they had about the same performance over 5 years.

[gridq]

[/grid]

I think it’s important to clarify the difference between volatility drag and volatility harvesting:

- Volatility drag occurs when you hold a single volatile asset (like TZA) over time without rebalancing against anything else. Daily compounding in a sideways market steadily erodes returns.

- Volatility harvesting, on the other hand, happens when you rebalance a volatile asset against another uncorrelated asset. This rebalancing exploits the back-and-forth movement to “buy low and sell high” repeatedly—even when neither asset has a long-term trend.

While Charles may face some headwinds from transaction costs due to frequent rebalancing, if he’s managing this in a live strategy, he’s more likely benefiting from volatility harvesting than suffering from volatility drag.

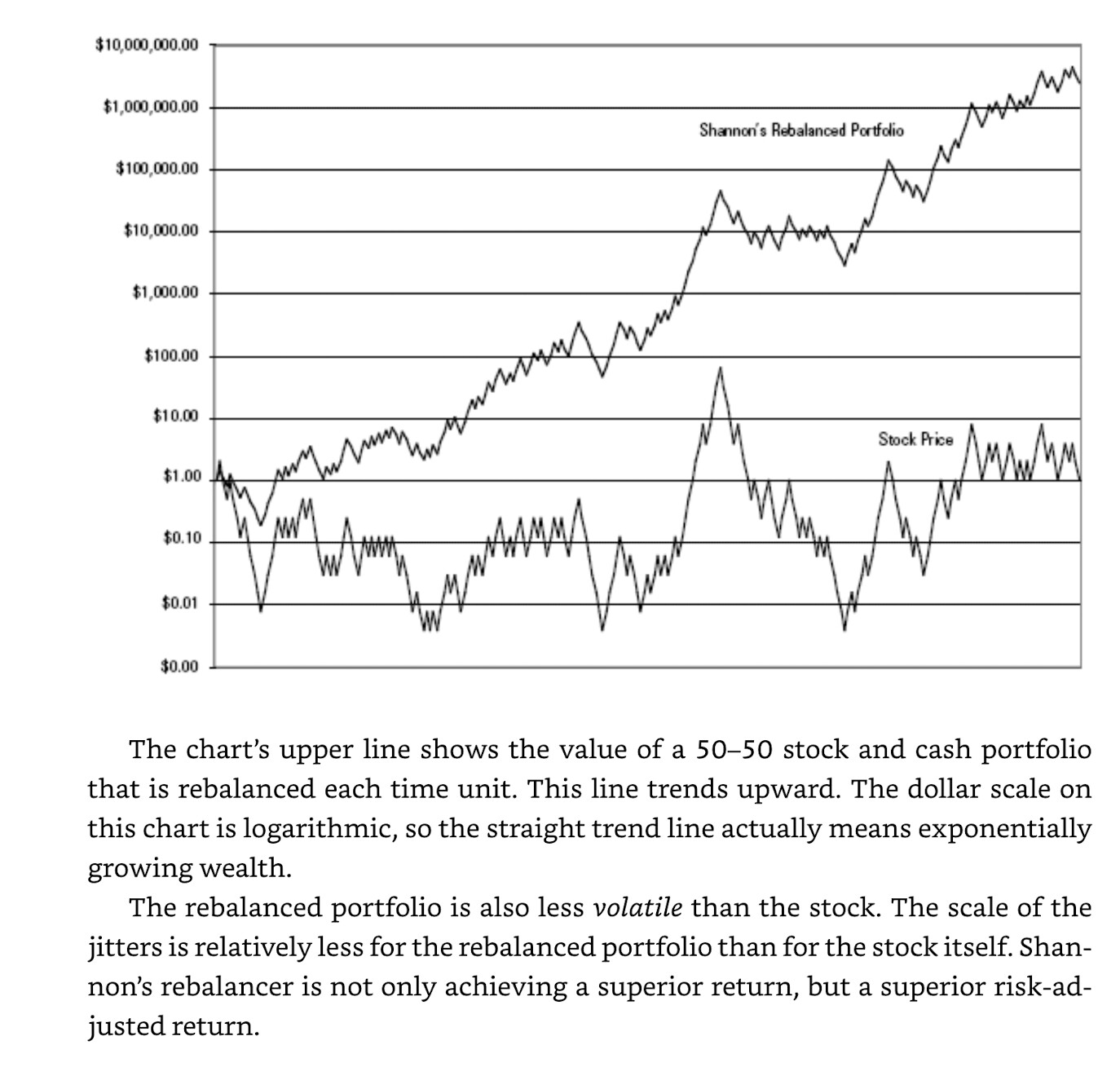

This idea is captured beautifully in the following excerpt from Fortune’s Formula, describing Claude Shannon’s famous “Demon” strategy:

Shannon’s main subject was an incredible scheme for making money off the fluctuations in stocks. You can make money off stocks when they go up (buy low, sell high). You can make money when they go down (sell short). You just have to know which way prices are going to move. That, suggested Bachelier, Kendall, and Fama, is impossible.

Shannon described a way to make money off a random walk. He asked the audience to consider a stock whose price jitters up and down randomly, with no overall upward or downward trend. Put half your capital into the stock and half into a “cash” account. Each day, the price of the stock changes. At noon each day, you “rebalance” the portfolio. That means you figure out what the whole portfolio (stock plus cash account) is presently worth, then shift assets from stock to cash account or vice versa in order to recover the original 50–50 proportions of stock and cash.

To make this clear: Imagine you start with $1,000, $500 in stock and $500 in cash. Suppose the stock halves in price the first day. (It’s a really volatile stock.) This gives you a $750 portfolio with $250 in stock and $500 in cash. That is now lopsided in favor of cash. You rebalance by withdrawing $125 from the cash account to buy stock. This leaves you with a newly balanced mix of $375 in stock and $375 cash.

Now repeat. The next day, let’s say the stock doubles in price. The $375 in stock jumps to $750. With the $375 in the cash account, you have $1,125. This time you sell some stock, ending up with $562.50 each in stock and cash.

Look at what Shannon’s scheme has achieved so far. After a dramatic plunge, the stock’s price is back to where it began. A buy-and-hold investor would have no profit at all. Shannon’s investor has made $125.

This scheme defies most investors’ instincts. Most people are happy to leave their money in a stock that goes up. Should the stock keep going up, they might put more of their free cash into the stock. In Shannon’s system, when a stock goes up, you sell some of it. You also keep pumping money into a stock that goes down—“throwing good money after bad.”

Look at the results. The lower line of the chart shows the price of an imaginary stock that starts at $1 and either doubles or halves in price each time unit with equal probability. This is a geometric random walk, a popular model of stock price movements. The basic trend here is neither up nor down. The lower line therefore represents the wealth of a buy-and-hold investor who has put all her money in the stock (assuming no dividends).

Shannon’s Demon

Poundstone, William. Fortune's Formula: The Untold Story of the Scientific Betting System That Beat the Casinos and Wall Street (pp. 202-203). (Function). Kindle Edition.

3 Likes

Since it’s already come up: this level of volatility may actually allow for some volatility harvesting to occur. In any case, when an asset is rebalanced regularly with another, the average return—or even the CAGR—can be misleading indicators of its utility for the entire portfolio.

Which is a good thing, in my view. Like Charles, you are probably not having a problem with volatility drag and may be benefitting from volatility harvesting.

Yes, that's one of the reasons it's so important to rebalance one's hedge and to keep it as a constant percentage of one's portfolio. But first you have to choose your hedge wisely. Anyway, good points, Jim!

1 Like