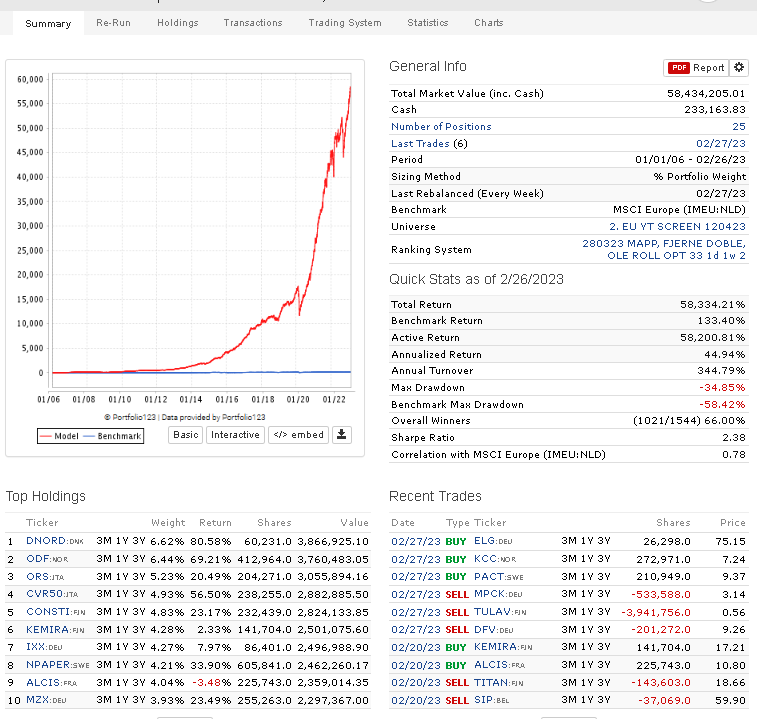

This is an interesting topic and I asked ChatGPT3.5 about this to try to learn more.

It is interesting that it has an understanding of the meaning and importance (or lack of importance perhaps) of effect size in this context without any prompting from me.

Here was my question: “Why is the effect size for stock returns constant?”

FWIW, here was the response from ChatGPT 3.5: "The effect size for stock returns is not necessarily constant. In fact, stock returns can be highly volatile and unpredictable, and their effect size can vary depending on a number of factors, such as market conditions, company performance, economic indicators, and geopolitical events.

However, some studies have shown that over long periods of time, the average effect size of stocks tends to be relatively consistent. This is known as the equity premium puzzle, and it refers to the fact that stocks have historically provided higher returns than safer investments like bonds, even though they are riskier.

One explanation for this phenomenon is that investors demand a premium for taking on the risk of investing in stocks, and this premium remains relatively constant over time. However, there is still ongoing debate among economists and financial analysts about the underlying causes of the equity premium puzzle, and it is not yet fully understood."

Edit: I am not sure that ChatGPT got that entirely correct. If I understand the equity premium puzzle (EPP) correctly it attempts to explain why the effect size is DIFFERENT for stocks and bonds. Not the same as it seems ChatGPT was, incorrectly, implying here.

Despite ChatGPT’s obvious error regarding EPP (and bonds) it does leave open the possibility that the effect size for stocks is fairly constant over longer periods.

And clearly ChatGPT got that the fact that the broader topic is widely debated with no clear answers (a puzzle not just for us or me at least). I don’t mean to imply that I have added much to the debate as far as finding an underlying cause for all of this. I have found the effect size useful in other contexts.

BTW, since ChatGPT 3.5 seemed to be incorrect I upgraded and asked ChagGPT 4 the same question. Notice ChatGPT 4 does leave out any reference to the equity premium puzzle which was the main error I identified. In addition, I think relating this to the efficient market hypothesis (EMH) is more accurate—especially since it calls into question whether the EMH is always correct and says there are probably anomalies or exceptions to the EMH. It is not dogmatic in its support of the EMH.

ChatGPT 4: "The assertion that the effect size for stock returns is constant may not be entirely accurate. Stock returns are influenced by various factors, which may change over time. These factors include economic conditions, market sentiment, company performance, geopolitical events, and investor expectations, among others. As these factors are dynamic and subject to change, it is challenging to assume that the effect size for stock returns remains constant.

The Efficient Market Hypothesis (EMH) posits that stock prices incorporate all available information and that it is impossible to consistently outperform the market. However, the EMH has been challenged by various anomalies and market inefficiencies, which suggest that stock returns may not be entirely predictable, and their effect size may not be constant.

There are different approaches to measuring the effect size for stock returns, such as the Capital Asset Pricing Model (CAPM) and the Fama-French Three Factor Model. These models attempt to explain stock returns using a limited number of factors. However, the stock market is a complex system with a multitude of factors that are constantly changing. As a result, it is difficult to generalize and claim that the effect size for stock returns is constant.

In summary, the effect size for stock returns may not be constant due to the dynamic nature of the factors that influence stock prices. Market anomalies and inefficiencies also challenge the notion of a constant effect size in stock returns."

This mere mortal does not have much to add to that  I think it is not bad.

I think it is not bad.

Jim