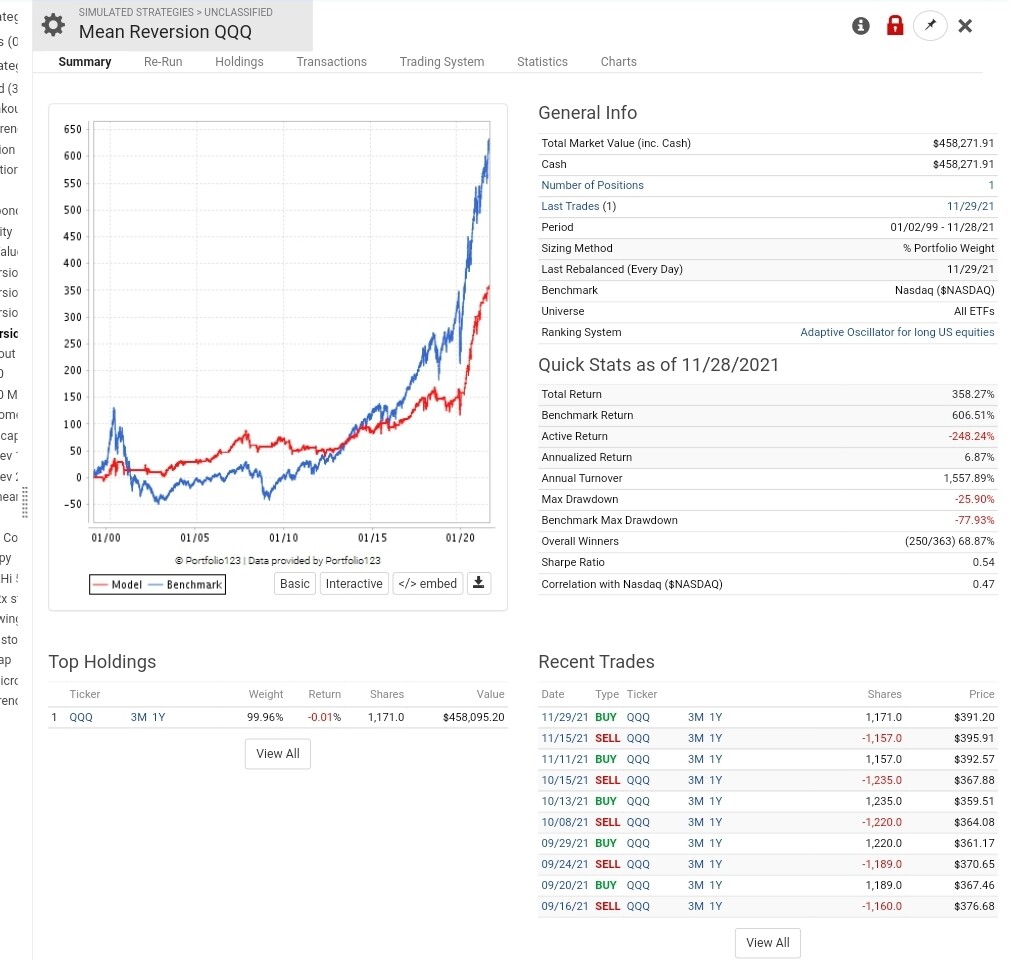

Hey there. Looking to replicate a QQQ trading system from @QuantpT on Twitter. Basically the rules are…

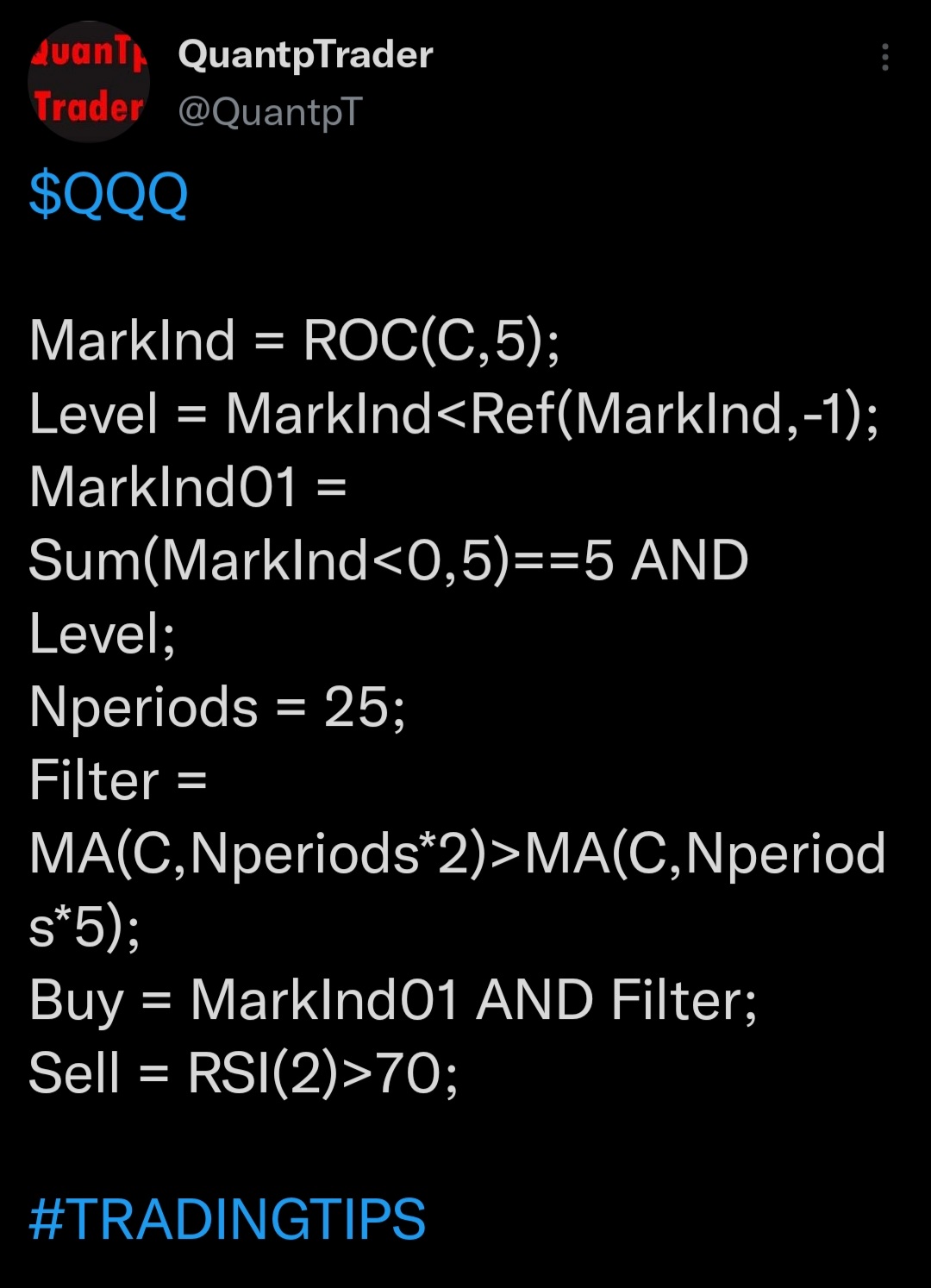

Buy if QQQ

SMA(50) > SMA(125) &

ROC(5) < 0 for each of the last 5 days &

ROC(5) close < ROC(5) yesterday’s close

Sell if RSI(2) > 70

I’m getting a worse result than the author who runs the system on Amibroker and I wonder if my code is correct for summing the number of consecutive days with the ROC(5) < 0. His system may be selling the close with RSI(2) > 70 which I don’t think I can replicate here?

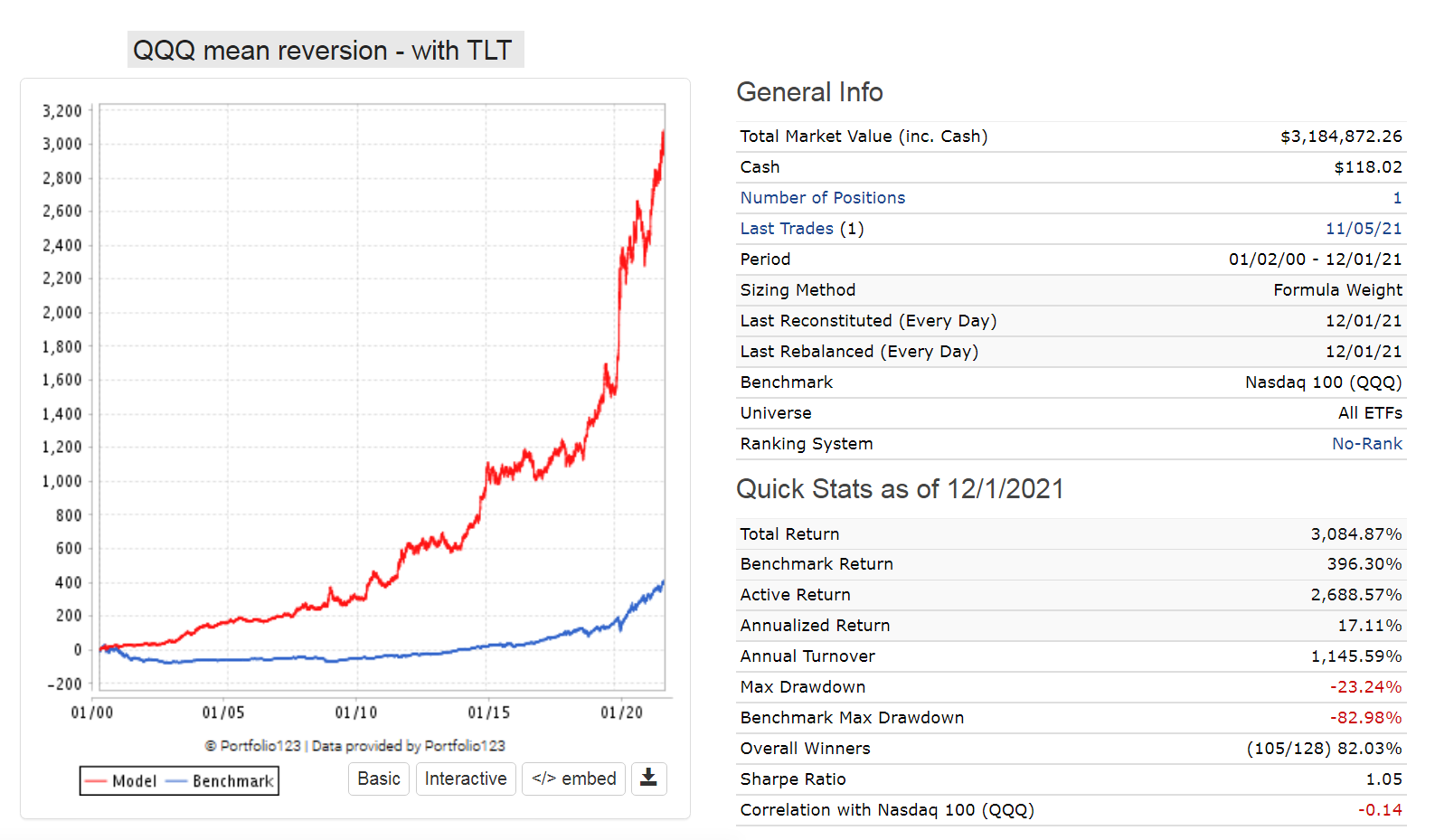

Roger that. TY. I only have the simulation level sub, so it won’t let me use position weighting, but I appreciate the result with TLT. My image was that the low exposure to equities would give a decent result if we allocate to treasuries when out of the market… I don’t suppose there is a way to run this without the simulation level subscription?

I’d like to run it with a basket of bonds when not in QQQ using trend following to pick duration.