https://www.quantopian.com/posts/quantopians-community-services-are-closing

“Our mission was to break open quant finance and make it accessible to everyone”.

Wrong mission that ate up $50M in venture capital. Not everyone has been wanting to do quant finance. And learn to program in Python. Even with our simplified approach this stuff is hard for 99% of the DIY investors, and demands time to learn.

We’ve been fortunate to find a niche market for our core USA products, but entire sector of investing tools has slowed down. This is the main reason why we haven’t bought European data, and why we have been diversifying our product line up.

Also the returns of “value” approach , which is typically the target of quant finance, has been atrocious. In the end people want to make money , or at least beat the indexes by any margin. And they have very little patience.

I have not spent a lot of time at Quantopian. But is seems they were always having contests for ideas to sell to hedge funds or other institutions.

I wonder if part of the failure is simply due to the fact that the models did not work.

Remember this paper that showed models developed at Quantopian do not work out-of-sample? All That Glitters is Not Gold

Maybe they just stopped wanting to pay for something that doesn’t work.

Jim

All,

Weird that people missed this. I confirmed something. Quantopian’s business model is (or was) completely different than ours.

I do not think the assumption that Quantopian closed because Python is too hard can be supported by any evidence.

People who signed up for the free version of Quantopian (like me) could never use it for investing. At least not if they wanted to use the “holdout sets.”

From Quantopian’s site:

“Quantopian provides dozens of datasets including pricing, fundamental, and alternative data. Much of the data is available up to the present day, but some datasets have the last 1-2 years of data held out. Full datasets updated through the current day are available in Quantopian’s enterprise offering.”

So if you wanted to make any predictions using much of the datta you needed to pay and go here: Quantopian Enterprise

Granted if you used just pricing data (and perhaps some other types of data) you could make some predictions.

But I refer you to this post to show you how well time-series data works in practice: One Anecdotal Look At Time-Series Data using Machine Learning

To be sure, Earnings Estimates Data is withheld for non-paying customers at Quantopian. I suspect that as far as “full datasets updated through the current day” for use in the morning (like P123) Quantopian was lacking in many categories.

So here are 3 possible reasons Quantopian is closing:

- Time-series data alone does not work. Probably true from my experience. So non-paying customers may not find value in this.

But non-paying customers were never the source for the revenue stream (by definition). So this means one of the following are at least part of the story:

-

Pros funding the competitions never found value in the models because they never worked out-of-sample.

-

Maybe some of the competition winning models did work out-of-sample but the institutions have already harvested the best models.

This last is probably the best P123 can hope for. It would be good if we believed that some of the models did end up working out-of-sample. But is gives me little comfort knowing that the successful models are now in the hands of institutions (who paid for the competitions).

I do not think the business model of Quantopian has anything to do will what P123 does. I wonder what people from P123 who said they were able to use Quantopian were doing over there.

I do not know if Quantopian Enterprise is closing or not. But probably good for P123 if it is.

Maybe P123 can capture some serious investors who were not just playing with Python code to win some prizes. I doubt if P123 code will be any problem for them and if they want to use Python they may find some rolling-backtest data in DataMiner useful.

Best,

Jim

This is nice to know, instead of you guys just stringing me on this whole time.

We’ve actually negotiating for years. First with S&P. Then we did the crowd-funding and 150K were promised from you guys towards European data. Then S&P abruptely pulled the plug on historical data and wanted all sorts of new restrictions. So had to switch to FactSet which was major effort. Is the 150K still there now that it’s FactSet data ? Guess we could do the crowd-funding again to find out.

Jim, could you correct the URL for this link? Thanks! - Yuval

Yuval,

Yes. Seems to work now.

Thank you for letting me know about the link. And thank you for your interst in my post.

***Edit: okay The link works now and is in the propper spot in the post. Sorry.

Best,

Jim

It seems Quantconnect has done a migration tool for ex-Quantopian users: https://www.quantconnect.com/forum/discussion/9585/quantopian-shutdown-migration-2020/p1 However, last time I had a look at QC, about 1 year ago, it was a less friendly and less sophisticated platform than Quantopian, regarding both data integration and programming framework. And very far behind P123 in UI/UX.

I’m just a european small-time investor, but my impression is that a portion of investors like me are mostly interested in the local stock markets. Home bias is a thing in Europe just like anywhere else. I suspect that by adding ex-Usa data you would attract new customers that are not interested your present datasets.

Quantopian lost their #1 client/partner in February: https://www.bizjournals.com/boston/news/2020/02/20/fintech-firm-quantopian-is-returning-investors.html

And it seems their “challenge” business model didn’t work out to keep the free version. I don’t know about the Pro version.

This is absolutely correct. P123 is on a better product path, for sure.

My guess is that their platform couldn’t compete with High Frequency Traders. There was a time when I was at home doing some day trading from my computer and the HFTs were running circles around me and my trade instructions. The problem with Quantopian is that developing algos based on simulated real-time trading just doesn’t work when you put it into practice, when you have active HFTs working against you.

Marco,

So just to be clear: you are now saying that European data is not going to happen, as things stand? On another thread, it had been promised this month…

Roger

If Europe Data needs some cash raising, put it on, I am in (as I was in the first round).

One Idea would be that you raise the cash an pull forward subscriptions e.g. the ones who want

Europe data chip in with a subscription for the next 5 years.

I am with Roger here, the communication and expectations need to be managed in a better way, otherwise

EU Data is a running gag…

I think P123 could be agnostic as to how the data is used. Let people debate their preference in the forum forever.

If someone wants to use a spreadsheet, SPSS, Python, R, C++ why would P123 care?

This does assume that people will use things like ranks that are not limited by the data provider. I think a lot of people can use this.

Once you have what you want in a csv spreadsheet (the way you want it) Python can even be run for free on Colab. So anyone now without a home at Quantopian could migrate easily to P123 with the proper downloads.

As far as the PIT-ishness of the data you can provide a lag to some of the data and P123 could facilitate this. Members can lag data by a day now using Weekday = 3 in the buy/sell rules.

Could be a great opportunity for P123. P123 should get serious, however.

As an example of not too serious: ‘PIT-ish.’ Cute, IMHO. Like being 'a little pregnant.’ I nearly died laughing. But does not belong on a site for pros, I think. Even if it is a good joke I already heard it.

Honestly. Just advice. I am not sure it matters to me at this point. I am ready to get serious with my retirement money. And stop debating whether I should use multiple iterations of spreadsheets (like some do even at P123) or Python with my downloads.

Jim

It seems to depend on who / when you ask. Yuval said it was happening Oct 2020, then said it was for sure happening soon when Oct 2020 didn’t happen. Marco has now said that it didn’t happen because their investing tools sector has slowed down so they didn’t want to buy the European data. I wouldn’t hold your breath, this back and forth has been happening since 2016 or 2017.

Sorry about the mixed messages. We had decided a few months ago to go ahead and purchase world data, and finance the whole thing ourselves. We were very close to pulling the trigger. Several things have happened that made this a high risk proposition, and potentially a money losing / cash draining project:

- Huge amount of uncertainty as the world is headed for another lockdown. The first thing people cancel to conserve cash is these types of memberships

- Slowdown of the entire sector : quantopian closing for example, but others are complaining

- Performance! people in the end want to make money but quant/value strategies have been underperforming. Buying an index was a wise move for the past 5 years. Buying the QQQ would have been brilliant.

- Being the only ones to have S&P data was a real differentiator. Having to switch to FactSet has not been good to us.

So we decided to hunker down for a bit. Maintaining our cash reserves during this uncertain times is more prudent.

But I suppose there’s no harm in doing the crowd funding again to see if the demand is real. But we’ll bump up the minimum a bit. Here are the terms:

If we raise $200K we’ll go ahead with Europe. If we raise $300K we can do the world. Using around $1200/year for each region we would need

For Europe:

166 users pledging $1200 for 1 region for 1 year

or

83 users pledging $2400 for 1 region for 2 years

For world:

250 users pledging $1200 for 1 region for 1 year

or

125 users pledging $2400 for 1 region for 2 years

We’ll get the campaign up and running again for the next month. The amounts would be non-refundable and only usable towards the new regions.

NOTE: the last time we did this we had 150K pledged I believe. We gave the go ahead to S&P but then they backed out from their previously agreed upon terms.

Cool! I’m in.

My 2 cents.

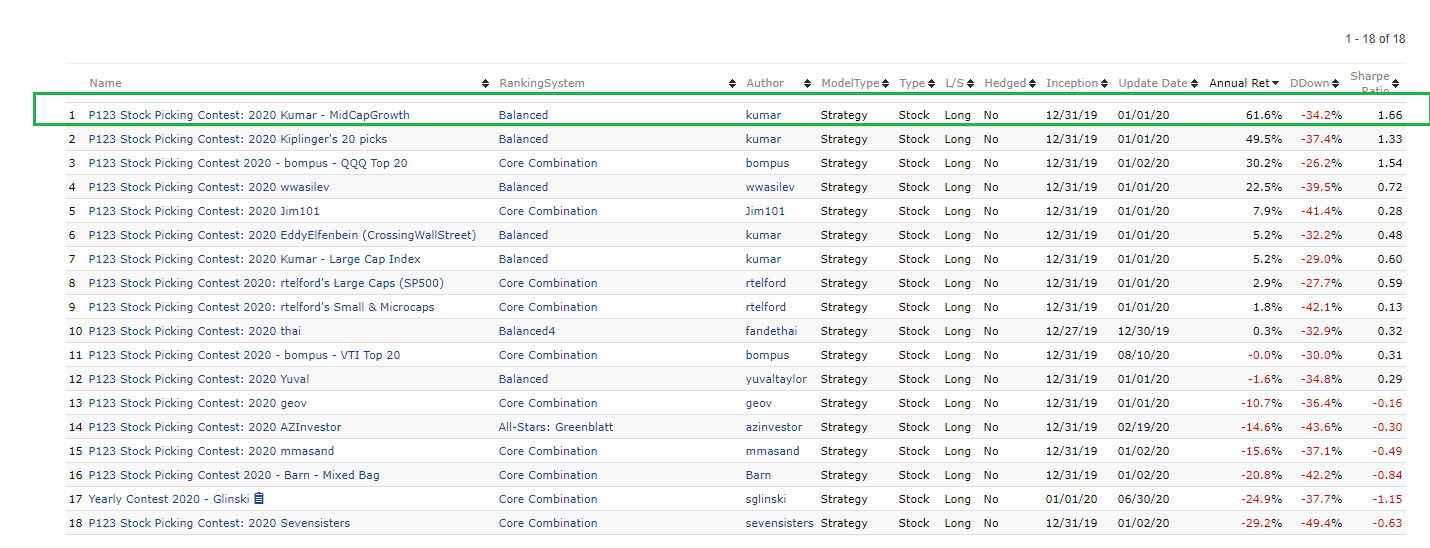

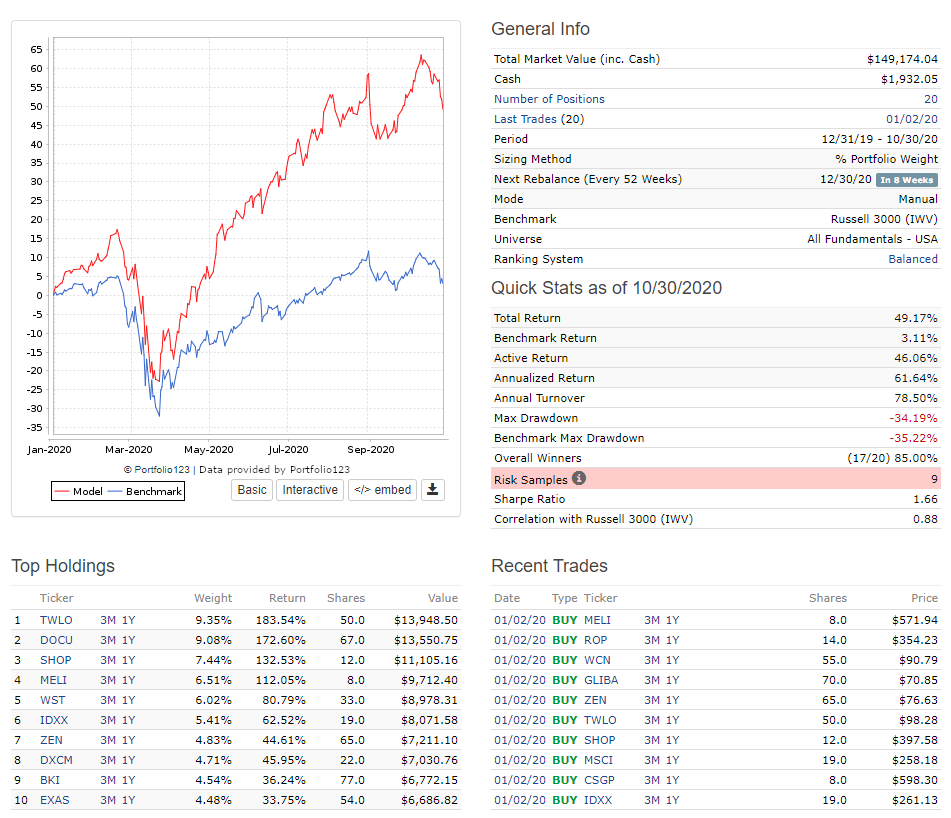

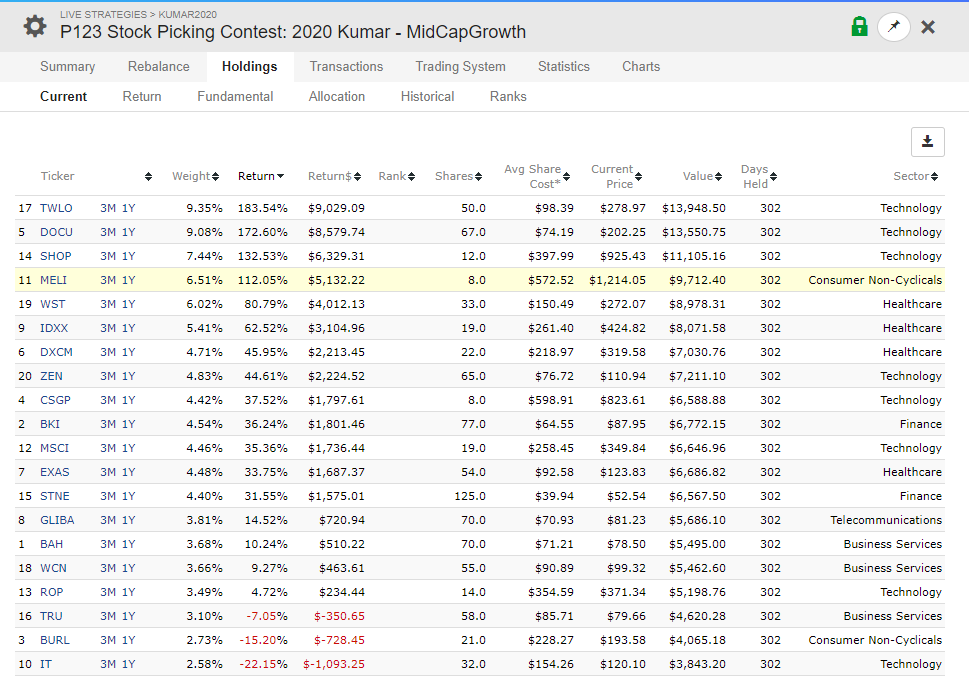

I believe p123 should have manual stock picks for quarters and yearly strategies for paid service to attract stock picking experts and with reasonable amount of liquid stocks as i am running my P123 competition free model with 20 stocks. I am very successful in 2017 35%+ return, 2019 40%+ return this year 2020 60%+

It will help to P123 to grow not only by Quant automated computer system, even by the successful experience of investors cherry picking stocks using over long period of time methodology.

Expert can demonstrate performance using P123 for their manual stock pick model; as they performance are tracked, it will help improve the experts skills practicing in out of sample and rewarded by subscription profits for many years to come.

==============

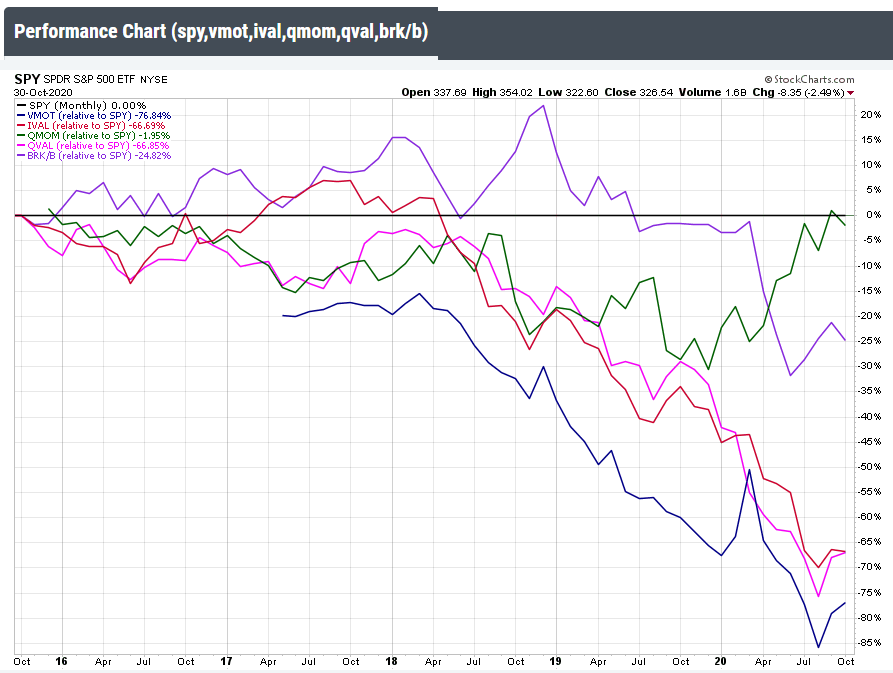

Here, Quant ETF performance for last many years (5 years) underperformed bench back; this quant system are designed and managed professionally with team of Phds with full-time dedication;

Now, P123 system only focusing on this Quant system which has poor track record for last 5 years; If P123 want to become successful; they need to keep foot on Manual stock picking strategy and regulate them

as useful to the subscriber to grow their wealth year by year.

Thanks,

Kumar ![]()