@Steve: I’m concerned that ADT is not adequate for estimating slippage for low priced stocks.

@Marco: Having a sliding slippage scale is an excellent idea. Portfolio123 has always impressed me as striving to give its users realistic tools.

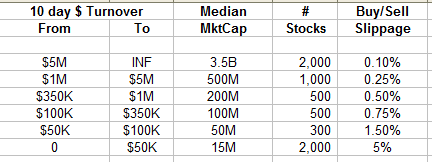

ADT by itself only gives 1/3 of the slippage picture.

Price gives another 1/3.

And the final 1/3 comes from trading at or close to the open (this final problem is already solved by R2G development rules).

First, ADT is a helpful guide. If one avoided stocks under $5 (or better yet under $10) then ADT would be sufficient.

Second, lower priced stocks need a much higher ADT to have the same level of slippage as measured by bid-ask spreads. Here are some examples from an extensive study I did of slippage a few years ago.

. For stocks in the $10.00-10.99 range, one needs to have average volume of about 7,000 shares (ADT of $73.5K) to get an average bid-ask slippage of 1.01%.

. For stocks in the $5.00-5.99 range, one needs to have average volume of about 35,000 shares (ADT of $192K) to get bid-ask spread of 0.95% – that is more than twice the ADT to get about the same spread.

. For stocks in the $1.00-1.99 range, one needs to have average volume of about 350,000 shares (so ADT of $500K) to have an average bid-ask spread of 1.1% – that is more than twice of the ADT of $5 stocks and it is five times the ADT of $10 stocks.

The same patterns appears for other bid-ask spread levels.

For example a spread of 0.3%: a $13 stock needs an average volume of 35k shares (ADT of $455K), but a $3.50 stock needs an average volume of over 500K shares (ADT $1,750K). – over three times the ADT.

ADT, by itself, will give an illusionary advantage to portfolios favoring low priced stocks.

Thirdly, for my study I “sampled” the bid-ask spread continuously through the trading day and discovered that the bid-ask spread took considerably longer to narrow for lower liquidity stocks that it did for higher liquidity ones. The higher liquidity stocks had their spreads narrow almost immediately after the market opened. Medium liquidity stocks would narrow over the course of several minutes. But lower liquidity stocks often narrowed very slowing, usually taking well over a hour to reach the average spread they would hold for the rest of the day. My understanding is the the R2G portfolio rules exclude using open prices for calculating back test stats and for real time stats that will unfold over time.

I have no idea if it is possible to make the slippage estimates more nuanced by including price as well as ADT, but it seems clear to me that stocks below $10 are in their own world, and those below $3 even more so. Here’s an idea that just popped into my head. If for ease of implementation, the slippage is based only on ADT, then it would be good to report the percentage of a R2G portfolio’s trades that fall within the following five price buckets: $1-1.99, $2-2.99, $3-4.99, $5-9.99, $10+. This would let a potential subscriber make a ball park estimate about whether he/she is interested in subscribing.

Disclosure: My spread study was done in the spring of 2007 so it is nearly 6 years old. I have no reason be believe the general pattern has changed, but I don’t have any proof for my assumption.

Brian