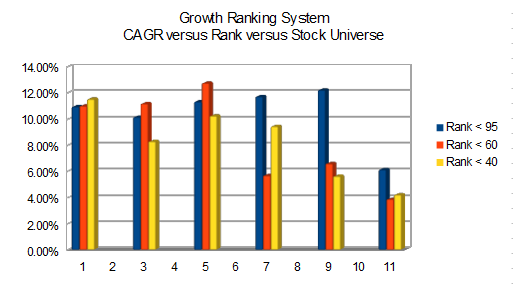

While attempting to assess the impact of different rank sell rules (“Rank < 95”, “Rank < 60”, and “Rank < 40”), I encountered some quite unexpected results. Although I made the discovery while looking at a version of momentum, I was able to duplicate the phenomenon using the Core:Growth ranking system.

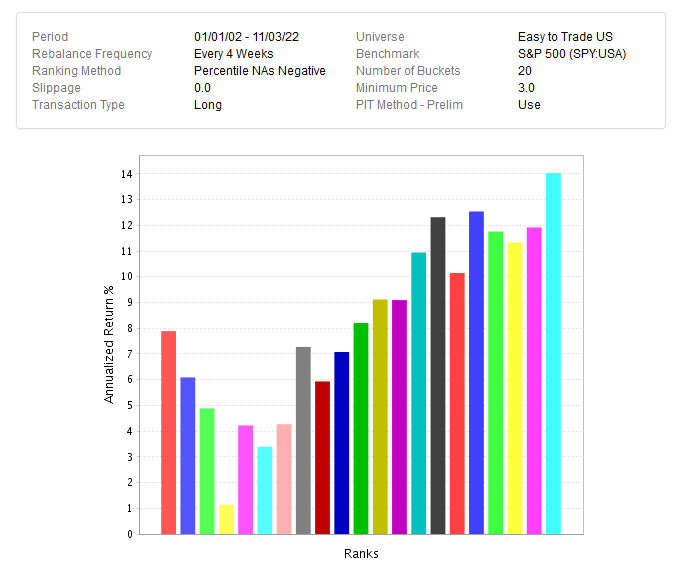

The phenomenon I observed was the big difference in performance between the ranking system performance screen and the simulation screen. I looked at the 6 different stock universes of (1) S&P 500, (2) S&P 1500, (3) Pr 1000, (4) Pr 2000, (5) Pr 3000, and (6) Easy-to-trade. When looking at the ranking performance screen for the S&P 500, here is what I got for 01/01/2002 - present.

Now contrast the ranking system results above to the results of using the simulator over a similar period for a portfolio of 50 stocks, using 3 different sell rules, for the 6 different stock universes:

So my biggest question is why is there a big fall-off in performance, especially in the “Easy-to-trade” universe?

I suspect the explanation is: The “Easy-to-trade” universe contains a large set of much smaller/less liquid stocks than the S&P 500, so it’s important to properly simulate slippage. The rank performance model has no slippage (from your screenshot), and so gives too large returns versus a simulation.

By the way: I don’t think there exists an optimal sell rule (rank<40,50,etc) that’s valid for all ranking systems, I suspect we have to find the optimal rule for each ranking system.

Hi Cary,

If you wanted to compare the ranking system performance results to the simulation results, then you need to setup the simulation so that it replicates the ranking system test as closely as possible. There will always be some differences because the number of stocks per bucket cannot be matched exactly in the simulation.

Easy to Trade US has about 4000 stocks. So the top bucket of a 20 bucket ranking system test holds about 200 stocks.

Sim settings:

Sell rank<95 (to match bucket 20)

Commission and slippage = 0

Ideal Size of a New Position = .5 (200 stocks)

Ranking system = Core: Growth

Allow Immediate Buyback = Yes

Buy rule: price >= 3

01/01/2001 - 11/03/2022

Annualized Return = 13.7%. That is pretty close to the 14.1% for bucket 20 in the ranking system performance test.

Bucket 19 in the rank performance test shows 12.3%. I changed the sims buy and sell rules to replicate bucket 19:

Buy rule: rank < 95

Sell rule: Rank < 90

Annualized Return = 12.2%.