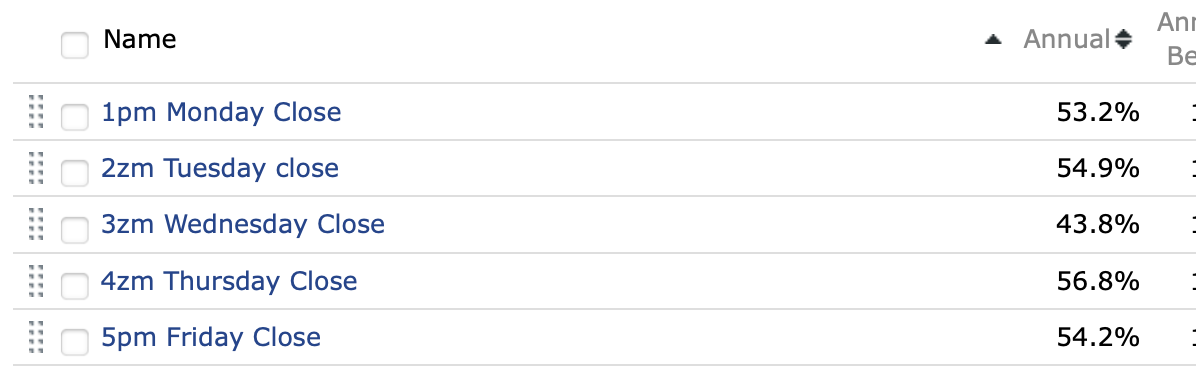

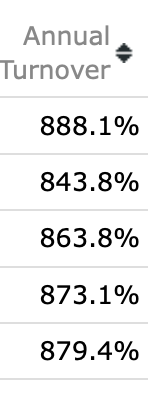

Monday was rebalanced on Monday each week and only Monday. Once per week rebalance, like many Designer Models.

Tuesday was rebalanced on Tuesday each week and only Tuesday.

Wednesday, Thursday, and Friday followed the same pattern.

Prices are automatically adjusted by P123 to reflect the closing price (reducing the chance of data-entry errors). I do have to take about 15 seconds each day to click “rebalance” to collect this data.

—

Symmetry and My Assumptions

I have a bit of a physics background, and much of modern physics relies on symmetry assumptions. For me, this study boils down to two alternate views:

- Symmetry: The days are essentially the same, with no meaningful differences in performance.

- Broken Symmetry: There’s something unique about certain days—perhaps a bunch of people trading Designer Models on Mondays or activity from platforms like Zacks influencing specific days.

To me, it’s a bit like the breaking of matter-antimatter symmetry in the early universe, which led to our very existence.

Okay, maybe that’s a stretch—but it illustrates the idea that while symmetry might be the natural assumption, symmetry can and does break, sometimes without any messy human interactions.

—

My Inclination

I tend to lean toward assuming symmetry unless there’s evidence to suggest otherwise. However, I find the idea of P123 members (and maybe a few people at Zacks) collectively moving the market on certain days intriguing.

That said, my study doesn’t provide enough data to definitively support or reject either hypothesis.

—

Bayesian Perspective

In a Bayesian sense, this new data doesn’t shift my prior belief much. There’s simply not enough data to make a strong case one way or the other. It’s the only data I have, but I’m very open to seeing additional studies or perspectives.

—

I hope this answers your question and provides some context for my approach and thoughts.

Jim