Dear all,

I remember Doney's post and just want to follow up on it with the following two articles from Bloomberg about retail trading in options.

As most ppl here already know, like all derivatives instruments, trading options like futures is a zero sum game and using it to hedge the portfolio as Yuval suggests is one thing. The odds of trading equity/index options on a naked basis are against retail and favor the market makers (who played around with small difference in implied volatility in the pricing) and institutional players including large hedge funds which are usually on the other side of the trade.

Pls check out the articles below if you have time.

Regards

James

At 10 AM, Stock Options Soar as Retail Traders Unleash New Bots

May 31, 2025 at 11:00 PM GMT+8

When people talk about algorithmic traders, it evokes images of rooms full of math PhDs creating complex models that place huge trades in milliseconds after economic or earnings data is released. But now, it’s retail traders who are turning in droves to automated trading, building the kind of programs in their basements more associated with Wall Street banks than the Reddit thread r/wallstreetbets.

Using these systems, though, has a downside: they can result in predictable, herd-like behavior, with data from Cboe Global Markets showing trades clustered at certain times of day. There’s a risk that more sophisticated market participants could exploit the predictability of small-volume traders at specific moments when retail demand for options spikes.

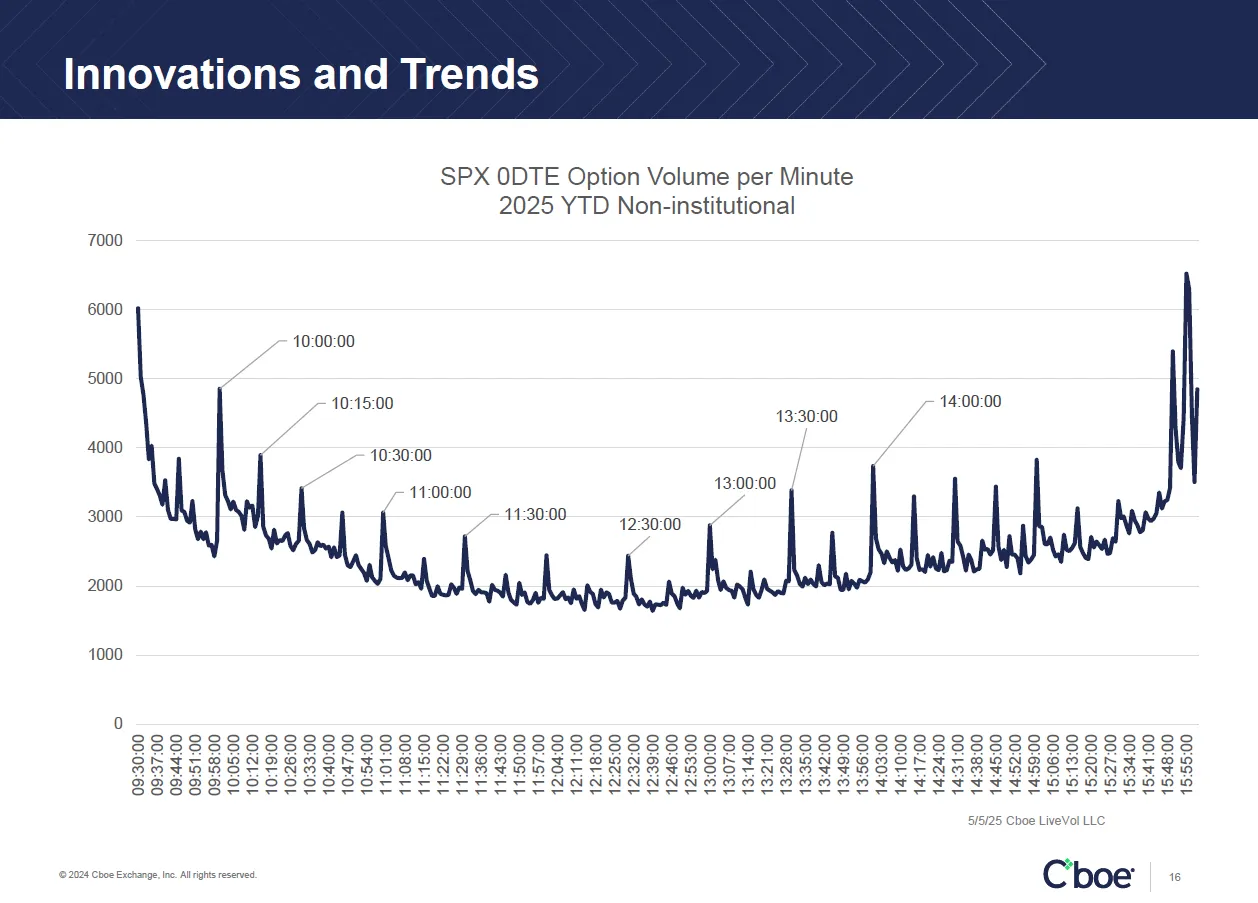

Speaking at the Options Industry Conference in Florida earlier this month, Henry Schwartz, vice president of market intelligence at Cboe Global Markets, showed a slide that surprised many of the traders, analysts and exchange executives in attendance.

On the slide was a chart showing how many zero-day-to-expiry options — the uber short-term contracts that have grown to more than half of the overall volume in the S&P 500 Index on some days — were traded every minute of the regular trading session so far in 2025. It showed that retail volume spikes at exactly 10 a.m. New York time, with smaller spikes at 10:15, 10:30 and 11 a.m., and a larger spike at 2 p.m.

S&P 500 Options Volume per Minute in 2025Source: Bloomberg

Schwartz attributed the spikes in volume to systematic trading strategies by retail investors all programmed to run at the same moment. “Customers turn these systems on to sell condors and manage them and they pick their time intervals, and they tend to pick round minutes,” he said, referring to one of the more popular retail options strategies.

The pattern has been showing up in S&P 500 intraday data for at least a year, Schwartz confirmed in a follow-up interview with Bloomberg. The pattern was no longer visible when trades smaller than 10 lots were excluded, indicating that the trend is driven by the smallest participants in the market.

Kevin Darby, vice president of execution technologies at CQG, which builds algorithmic systems for investors, said it’s normal for market makers to change quotes based on patterns in order flow.

“If you’re going to make a bet, you have to think about what it would be like to be the bookie,” he said. “And so, in this particular scenario, if I’m the bookie, and I know that the 12:30 orders are about to come in, I’m going to move my odds a little bit.”

Read more: Wild Stock Swings Magnified by Headline Bots, Strained Liquidity

To be sure, the competition in a liquid contract like the S&P 500 may limit how much the influx of retail orders could shift the market.

Schwartz linked the tendency of retail trades to cluster at certain moments in the day to an “explosion” of software providers offering to help customers automate options trading strategies.

These software providers connect to retail brokers via Application Programming Interfaces (APIs), which allow different types of computer programs to communicate and share data. Brokers like Interactive Brokers Group, Inc., WeBull Corp. and Tradier Inc. all allow clients to plug in custom built trading software.

Traders can buy such tools off the shelf or build their own, sometimes by delegating the code writing process to artificial intelligence.

“In the last year we’ve had more requests from retail customers to build to our APIs than I’ve seen in the last 10 years combined,” Tony Zhang, chief strategist of options software and training provider OptionsPlay, said in a separate panel discussion at the conference.

While the clustering of trades raises the question of whether larger professional firms have noticed this and are lining up to pick off the retail crowd, advisors to the smaller traders defend the practice.

Options Volumes Soar

Volumes have exploded since 2020, driven by a boom in retail trading

Source: Options Clearing Corp.

The popularity of particular times may be linked to common settings on backtesting tools, which allow a trader to run a scenario and see how much they could win or lose, based on historical data. Option Research & Technology Services and Options Omega are among the providers of such backtesting services.

Options Omega was co-founded by three retail traders based in Knoxville, Tennessee, who originally built backtesting tools for themselves before realizing there was broader demand for the product.

Troy McNeil, one of the firm’s founders, argues that the phenomenon of spikes in retail S&P 500 options volume at certain times of day is driven as much by small traders taking opposite positions. “I don’t know that everybody does Iron Condors at 10 a.m.,” he said. “People are doing a lot of different things — they’re selling, and they’re buying.”

Some strategies deployed by retail, such as automated covered call selling, are more akin to the kind of yield harvesting efforts associated with structured products, sophisticated financial instruments created by banks and sold to wealthy investors.

“They’re kind of in-housing their own structured product,” says Amy Wu Silverman, head of derivatives strategy at RBC Capital Markets. “Instead of buying the cookie, I’m going to buy the flour and the chocolate chips and then make the dough.”

Still, seeing the trading patterns illustrated so starkly was eye-opening to some in attendance at the conference. Matthew Amberson, founder of ORATS, said he was surprised that flows from retail bots were so visible in the S&P 500 market.

“It was shocking to see how many of those bots were in the market at the same time,” said Amberson. A group of traders all instructing bots to do the same thing at the same time is a “silly way” to trade, he told Bloomberg.

Options Trading Is Rigged Against Average Investors

Payment for order flow allows brokerages and big traders to team up against the little guy.

December 7, 2023 at 8:00 PM GMT+8

Would you gamble your life savings on a few hands of blackjack? Probably not. But as a former manager of options trading, I’ve seen amateur investors — encouraged by posts on Reddit and X of massive, easy overnight wins, and offers of “zero-commission” trading online — lose much of their net worth on risky bets.

What bothers me most is that some big trading firms are actually paying brokerages to take the other side of these trades, knowing they have better information than the small investors and so will profit big. These payments are known as “payment for order flow.”

In 2022, large trading firms including Citadel and Susquehanna paid a total of $2.9 billion to brokerages such as TD Ameritrade Corp. and Robinhood Markets Inc. to trade against their customers’ orders, according to SEC data compiled by Alphacution Research Conservatory. In short, they are paying for the privilege of taking advantage of the unsophisticated investor.

This is akin to a few Vegas casinos paying travel agents to send them droves of unsophisticated players. The travel agent, like a brokerage, is paid by volume, and so wants to promote as much betting as possible. Other casinos, like the trading firms that don’t pay for retail orders, would have reduced access to these profitable inexperienced players.

Trading by retail investors has recently reached as high as 60% of the total market volume in options, according to new research by Svetlana Bryzgalova, Anna Pavlova and Taisiya Sikorskaya of the London Business School, with dollar volumes increasing by more than 10 times in the last decade. (The firms I worked for did not pay brokerages for orders, but benefited from increased volumes in retail trading.)

And the surge is only accelerating. Last May, exchanges started listing options that expire on each day of the week rather than three days, and they have exploded in popularity. With the potential of making 50 or even 100 times your investment in a day, they are the cheapest and fastest way to potentially win big, the biggest dopamine hit available for sale on the exchange. According to research at the University of Münster, 75% of retail’s S&P 500 option trades today are of this variety.

For seven years I ran options strategies at large trading firms, so I understand that options trading can make you rich, fast. But even though many players claim a winning strategy, the vast majority lose money. I quickly learned that the small bettors tend to choose the worst investments. And the house always makes money.

Buying an option provides you the opportunity, but not the obligation, to buy or sell a stock at a certain price. Let’s say a stock is trading at $100, and you think the price will go up. You might pay $5 for the right to buy the stock for $110 at any point in the next six months. If the stock doesn’t reach $110, the option expires, and you lose $5. If the stock goes to $150, you make $45 on only a $5 initial investment.

If our model said an option was worth a dollar, we’d buy when the price hit 99 cents or sell for $1.01, collecting the invisible theoretical penny difference. We repeated this process with thousands of different options, every time a customer wanted to trade. Those small amounts added up to big ones.

Roughly a dozen other trading firms used similar strategies, competing to offer the best price to the customer. Collectively, we made up the house. This can be highly lucrative: In my last three years running the desk, we didn’t have a single losing month. Several other firms post equally impressive results each year.

The most important rule of market making: Not all customers are the same. Sometimes, shrewd hedge funds had better information than us and also had enough money behind them to move the market in their favor. Trading against them would be a losing proposition, so we avoided these orders.

On the other hand, customers trading small sizes consistently lost money. They had no informational advantage, and their orders could never move the market against us. Taking the other side of these trades was highly profitable.

Supporters argue that platforms like Robinhood allow everyday people access to profitable strategies. However, research at MIT indicates that retail traders lack enough private information to win. And according to London Business School research, buying $100 of the popular “zero days to expiration” options would cost up to $6 to $12 just to enter the position. Little surprise then that retail traders gave up an estimated $6.5 billion in trading cost between November 2019 and June 2021, even though most paid no direct commission to their brokerage.

What can be done to protect them? First, regulators should prohibit payment for order flow, creating a level playing field where all trading firms can compete by offering the best price.

Regulators should also continue to penalize dubious advertising practices that platforms have used to attract uninformed options customers. In 2021, the financial regulatory body FINRA fined Robinhood a record $70 million for “systemic supervisory failures,” accusing the company of allowing users to make riskier trades than they were qualified for. Robinhood continues to present the riskiest options — the ones that expire almost immediately — to the user first in the options trading menu, without any mention of their dangers.