When I first came to P123, my knowledge of quantitative analysis was more limited, but I did know about “momentum” and “value” as being factors likely to deliver above average returns (alpha).

Specifically, from reading books such as “What works on Wall Street”, I determined the best factors for value were price-to-cashflow and price-to-sales, perhaps because they are less often looked at than P/E ratios. Anyway, my own research suggested that 6 month relative strength was the best “momentum” factor, with shorter and longer factors also work reasonably well.

I used to screen for stocks based on price-to-cashflow, price-to-sales and 6 month momentum, and typically had a 20% trailing stoploss.

With this in mind, I went about creating a ranking system that I have retro-actively called “First Generation” ranking.

Although I have sinced moved on, and now have the more sophisticated “Third Generation” ranking (see: http://www.portfolio123.com/mvnforum/viewthread?thread=2837 ), I have decided to revisit the first generation ranking.

The main motivation is that this ranking system was first created nearly a year and a half ago, and this presents an interesting opportunity to study “in sample” vs. “out of sample” performance.

In creating the ranking system, I attemted to verify (or falsify) what I already knew: - the best momentum was 26 week, and the best factors were price to sales and price to cashflow. You can see the ranking system here:

http://www.portfolio123.com/rank_details2.jsp?rankid=26995

You can see the “old” factors that I considered that have now been zero weighted. One thing I did not know prior to P123 was the relative importance of “most recent quater” vs “trailing twelve month” data. There are arguements in favour of both - TTM data is unaffacted by seasonal varations, and is less “noisy”, it isn’t destroyed by a single “freak” quarter. However, most recent quarter data is more “fresh” and empirically it appears to be a better indicator, so I always use that now.

The sim that I used was based on a 20 stock portfolio, with simple rules, a 20% stoploss (from high) and a rank< 90, rough in line with how I used to trade prior to p123. Here is the portfolio:

http://www.portfolio123.com/port_summary.jsp?portid=338089

Its quite a reasonable performance, and I thought it looked fairly satisfactory, there had not been a great deal of optimisation - just some common sense and a few “tweaks”. So I decided to create a portfolio to “paper trade” it and observe the results. Here is that portfolio:

http://www.portfolio123.com/port_summary.jsp?portid=186885

As you can see, quite disasterous. In many results this should be taken quite seriously by everyone following quantitative strategies - even ones that appear to have little curve fitting can it seems simple “die”.

Or can they?

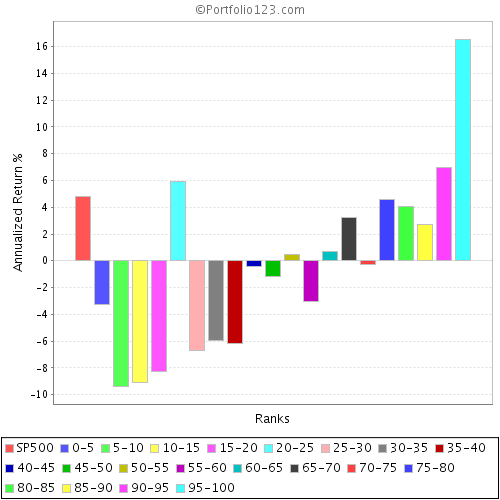

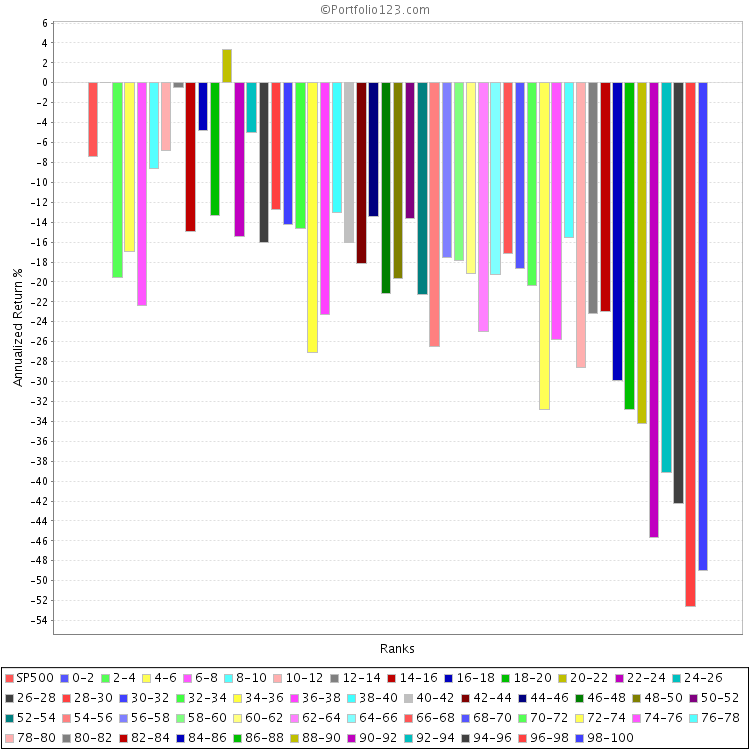

I had written off this process as being “too simplistic”. But then I looked at the ranking buckets of the system in 2007. With 20 buckets, in 2007 the top bucket did outperform the next one down, and so on and so forth (see picture). This leads to a very interesting conclusion:

The portfolio had failed to deliver real time performance but the ranking system had not

This to me is a paradox: The portfolio had not delivered above average returns, yet the ranking system itself was still predictive of “alpha”, and was still able, in 2007 to rank and select stocks likely to deliver above average performance.

This actually has been a complaint of many attempting to follow “value” strategies. They have noticed that buying stocks with low p/e ratios etc. is often a losing strategy, yet acedemics insist it should be a winning one. Perhaps the issue is this, if you really want to get the performance of the bottom decile of value stocks/or whatever, you need to buy all the stocks in the decile.

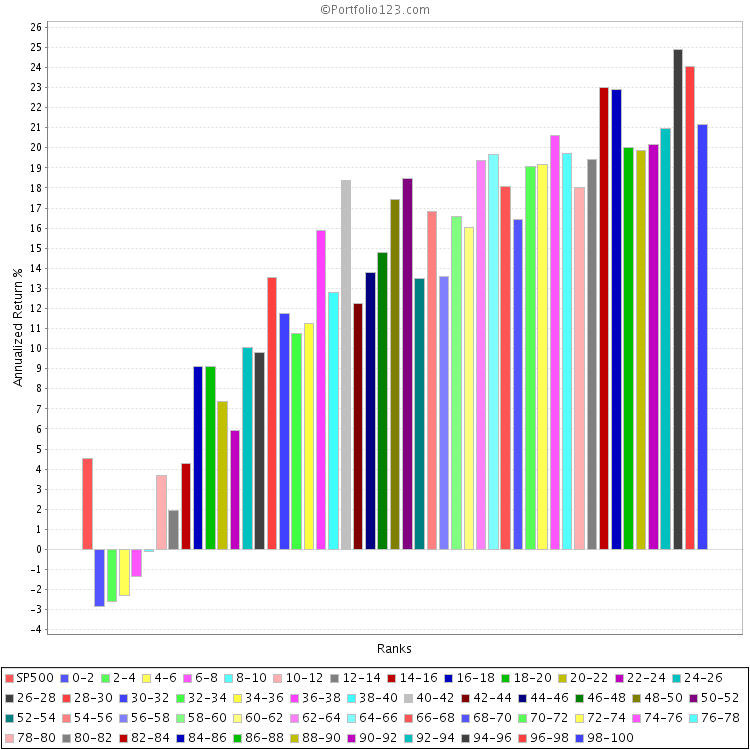

Given a stock universe that is sufficiently liquid is probably 5,000-7,000 stocks one twentieth of 5,000 is 250. At least 250 stocks are sitting in the buckets when looking at 20 buckets.

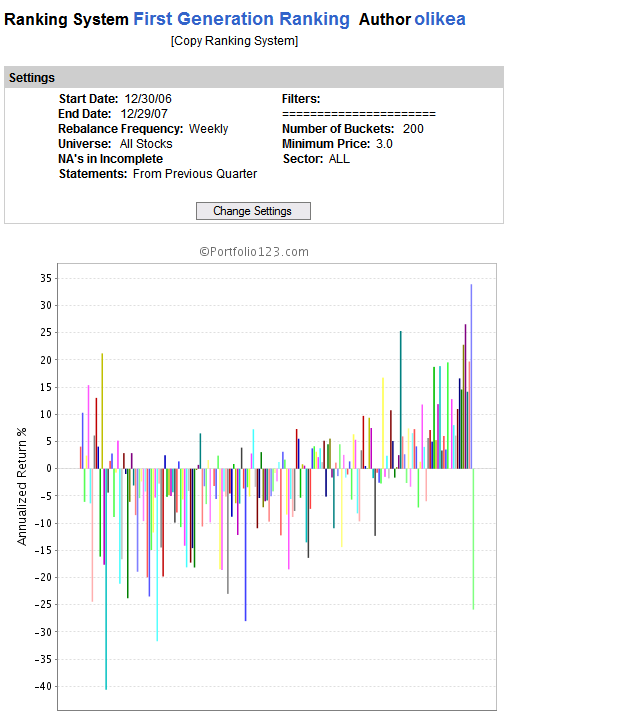

Of course, you can visually see that if you ask for more buckets, such as 200 buckets, the results are much more variable - more random. Although it may be tempting to optimise and create a top 199th percentile bucket, the fact is a lot of the perforamance may be down to luck.

Nevertheless, I decided to test by re-running the simulation over the out of sample period (2007) but varying the number of stocks being held, all the way from 20 (in the original) to 300 (which should be the top 5th percentile bucket).

Here are the results:

http://www.portfolio123.com/port_summary.jsp?portid=338056

Above is the “original” port, with 20 stocks. It total return was -16.68%, an “active” return of -20.33%. In short: Pretty miserable. It lost more money than every index over the year. Arguably a better benchmark would be the Russell 2000, or even the Russell 2000 value, but for simplicity I stick with the S&P500, besides I don’t believe you should simply change your benchmarket to cover up poor performance!

http://www.portfolio123.com/port_summary.jsp?portid=338058

This is a carbon copy but with 50 stocks. Total return: -3.6%, “active” return: -7.2%. Still a poor result, but better than the 20 stock portfolio.

http://www.portfolio123.com/port_summary.jsp?portid=338059

Ditto with 100 stocks. TR: 5%, AR: 1.3% - this portfolio interestingly performed almost exactly in line with the market. By now you should be seeing a trend:

http://www.portfolio123.com/port_summary.jsp?portid=338060

In a tough year for value strategies, the 200 stock port convincinvgly outperformed the market: TR: 10.7%, AR: 7.0%

http://www.portfolio123.com/port_summary.jsp?portid=338061

I went to 300 stocks as well, but it looks to be “over the peak” as it were, with TR: 9.2% and AR: 5.5%. But interesting how the 300 stock portfolio did outperform the 100 stock portfolio.

This really is interesting - it implies that “alpha” is possibly far more elusive than we give it credit for. You really have to make a large number of bets, and on a statistical basis, hope to outperform.

Perhaps this shouldn’t come as too much of a surprise. If it were really easy to generate alpha more people would be doing it, and in turn destroy the very inneficiencies that they seek to exploit.

This does tend to re-affirm my increasing belief that quantitative analysis works best with very large stock portfolios, picking up on innefficiencies that are too small and too subtle on a stock-by-stock basis for the majority of investors to spot.

That is my interpretation, but I am quite keen to hear other views on this (important) issue. Have I missed something?