Bear in mind, here, is that the equity risk premium. although a critical theoretical construct, is something that defies precise measurement because it’s an ex ante thing. In other words, we can look back and observe that the market may, over a period of time, have delivered a minus 5% risk premium, we would have to recognize the difference between ex ante, what investors expect ahead of time, and ex post, what investors actually wound up getting. Risk premium is an expectation, so when carried into the real world, sometimes the expectation is met or exceeded and sometimes life just-plain sucks.

Given the nature of what we’re dealing with, the best way to “measure” it would probably be something along the lines of how a sports media personality described the old incomprehensible and horribly confusing controversial NFL catch rule: If 20 guys watching the game on a TV in a bar think the receiver cleanly caught the ball, then its a catch. In finance, the 20-guys in a bar notion translates to an unspoken gentleman’s agreement that its about 4%-5%.

But is you want to math up here, it’s probably best to keep Occam’s Razor in mind (which should push you toward the simplest solution).

ERP = D*(1 + G) / P + G – Rf is needlessly complex because it relies on the cluster-fu** infinite growth rate assumption, twice no less, used by nobody outside the classroom to offset deficiencies in the dividend-yield start point. And the current number that comes out of it, 7.22%, would not likely be accepted by any of the hypothetical 20 guys in the bar until about 3:55 AM, when they’re completely sh**-faced and the bartender and manager are trying to shove them into Ubers over the objections of drivers who expect them to puke in their cars.

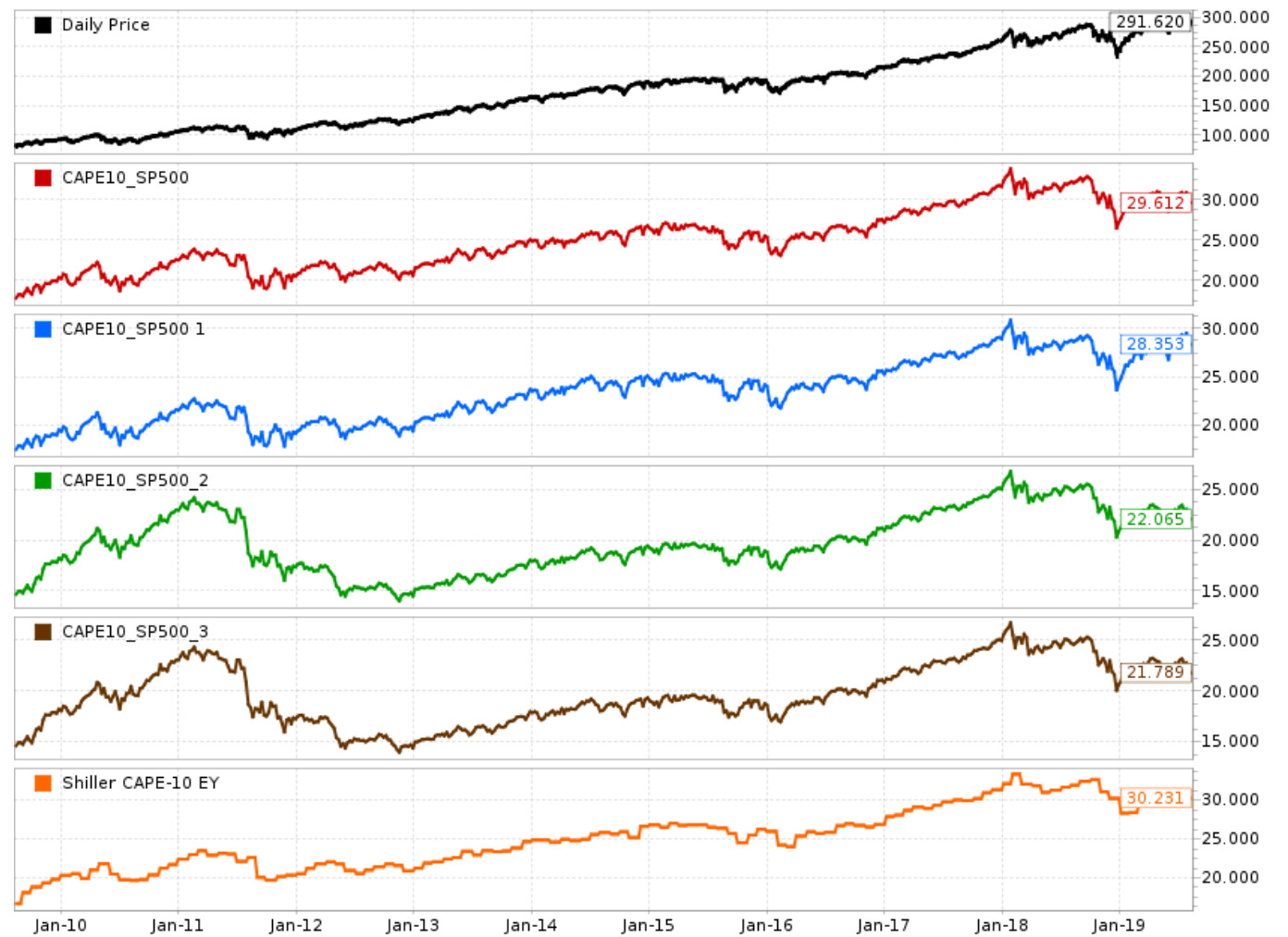

(1/(Close(0,#SPPE10)))*100 - (Close(0,##UST10YR)) is, when translated from p123 into plain English but illogical. CAPE is an inflation adjusted number. UST 10YR is not. CAPE is also a backward looking number. Risk premium is a forward looking concept. And as with 7.22%, the guys in the bar need to be ready to puke in the back seats of their 4AM Ubers in order to think 1.64% makes sense.

But at least the latter formula has some potential, assuming we correct the logical problems. If we turn CAPE around so its forward looking and and remove the inflation adjustment to make it consistent with UST 10YR, we might wind up doing this.

UST 10YR = 1.74%

SP500 Median Proj PE CY = 17.68 which flips over to an egs yld of 5.66%

SP500 Median Proj PE NY = 15.88 which flips over to an egs yld of 6.23%

That means our alternative ERPs would come in at

5.66% - 1.74% = 3.92%

6.23% - 1.74% = 4.49%

How 'bout that!

Not only would the 20 guys in a bar accept this even when they first arrive at 9 PM, if you use the Proj PE NY version and come in at 4.66%, close to the middle of their 4%-5% range, they might even pay for your drinks. And Occam won’t turn over in his grave.

One final “smell test,” (the most important test of all): Does this idea of the ERP being consistent with general ideas long held mesh with the observations of many that the stock market valuations are now very stretched. Actually, it does . . . perfectly. If you dig into macro valuations you’ll find that the main reason for the high valuation is the prolonged multi-decade collapse in interest rates which drove Rf to extremely low levels. Given that Rf is and remains within hailing distance of zero (I’m still waiting for a request I made a while back to a negative interest rate advocate to contact me off-line with a bid as to the annual rate he’ll pay me to refinance my mortgage), there are significant concerns that Rf has pretty much bottomed and will rise. That’s the problem. ERP isn’t likely to leave its current 20-guys-in-bar range unless or until there’s a major structural change in the equity market relative to other asset classes. It’s the Rf component that leads to the valuation concerns.

P.S. While I use the UST 10Y as a proxy for Rf, as do those who posted here, bear in mind this is not universally accepted. There are many who believe the term should not represent a theoretical investment horizon but be one that eliminates secondary market risk as well (i.e. the possibility the investor who needs to sell before the end of the 10th year might incur a loss in the secondary market) and per Rf at the rate of the shortest-possible term of a treasury instrument. If the 20 guys in the bar want to debate that, I choose to just find another bar in which to drink in peace.