I come from a quant commodity trading background. There we sized trades based on a risk budget. That works something like this:

AUM = 10,000,000

risk/trade = 1%.

risk = dollar risk to stop loss, or alternatively can be some dollar amount of volatility

So let’s suppose I had a new entry to buy crude oil at 60 with an initial stop at 55. So the dollar value of risk is $5000/contract. My 10M acct is risking 1% so trade risk = $100,000. Therefore I will buy 100,000 / 5000 = 20 contracts. The notional value of the trade is irrelevant but it is $1,200,000. I mention notional because imagine I also have positions in copper, gold, beans, bonds, Yen, cocoa, etc, and the combined notionals are probably well over $50,000,000.

I mention all this because as far as I can tell there is no way to manage trades like this in P123, which I think is a major short coming. Any account that uses portfolio margin can easily achieve the same level of notional account size.

P123 allows either static weight or dynamic weight and regardless of which you use the results are very similar. I think on day one when using dynamic, a sim will size trades that are meaningfully different than when using static, but going forward as one trade comes off and a new one replaces, the trade sizes are nearly identical because the sizing algo always wants to make the account fully invested based on whatever margin setting you use (including of course no margin). Correct me if I’m wrong.

So basically we are sizing trades based price. Which is fine if that’s what you want, but I think it is kind of dumb. You will be sizing a trade in a super low volatility stock the same as a high vol stock which doesn’t make sense. Better would be the ability to size trades based on the risk to your stop being hit, which would also incorporate the relative vols of different stocks.

My thought is a new weighting option should be enabled called Portfolio Margin. It will have inputs like:

% of account equity to risk per trade __

risk is based on __

maximum % sector risk __

maximum % total account risk ___

Taking it a step further, adding the ability to reduce positions based on a max risk level being breached would be great (maybe a trade that was initially sized at 5% of equity now is at 25% so reduce it to 20% type thing).

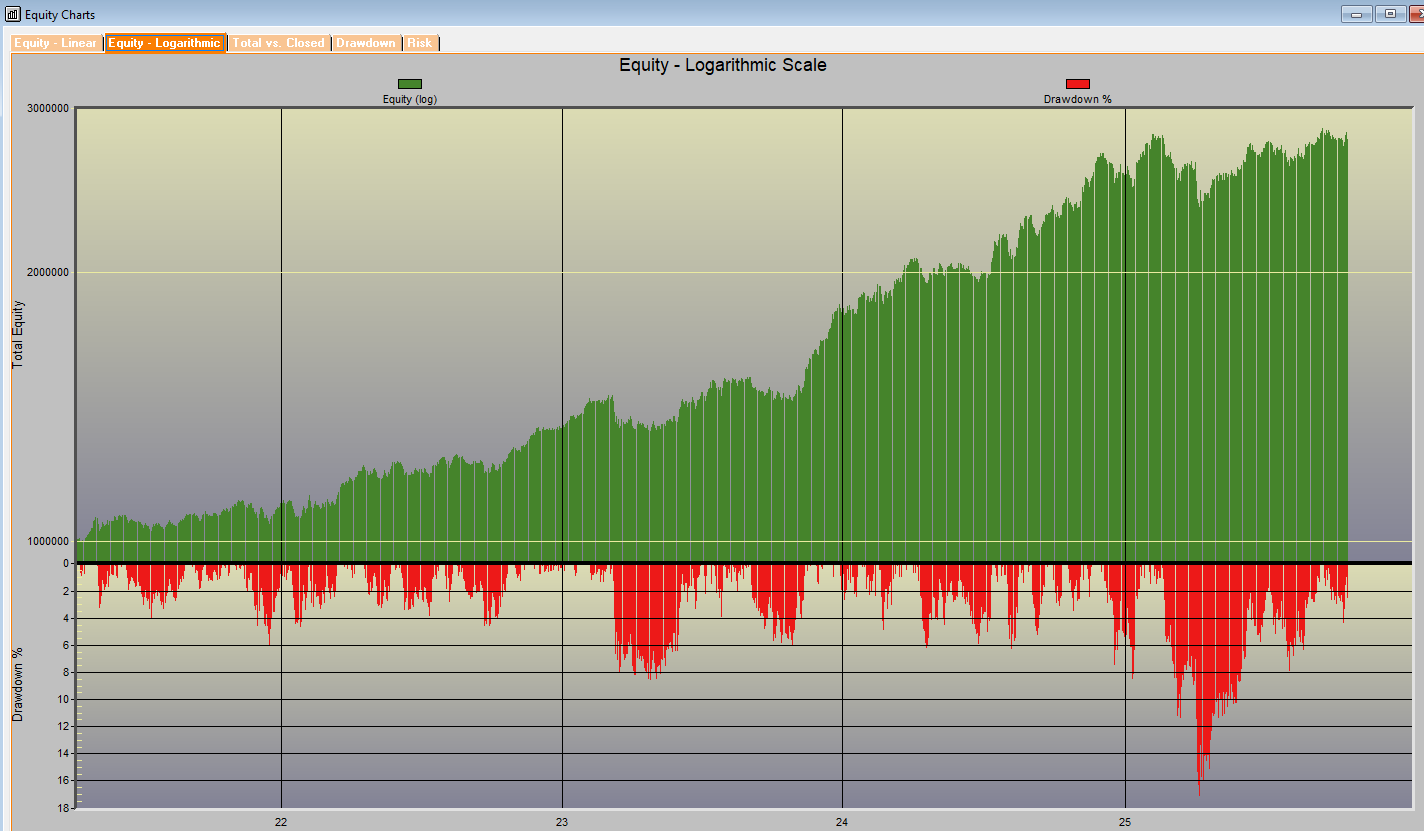

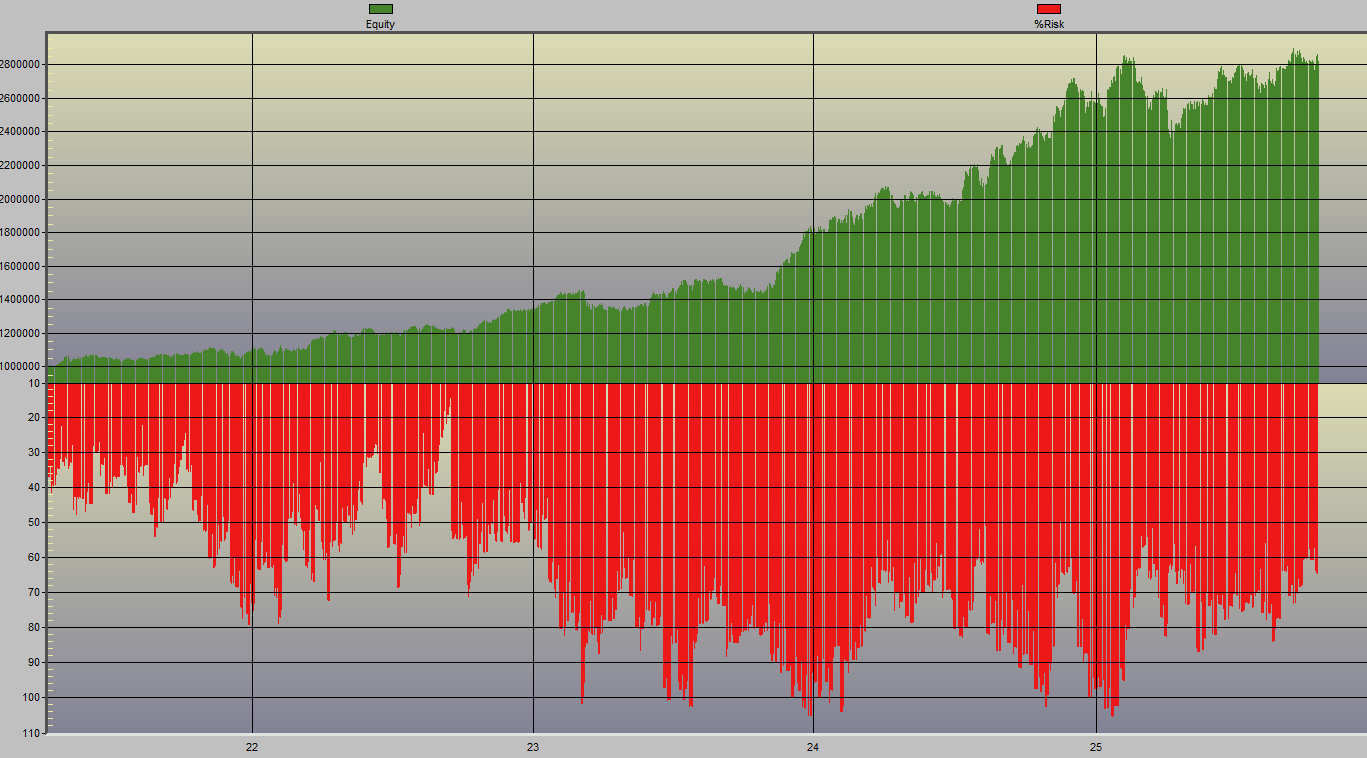

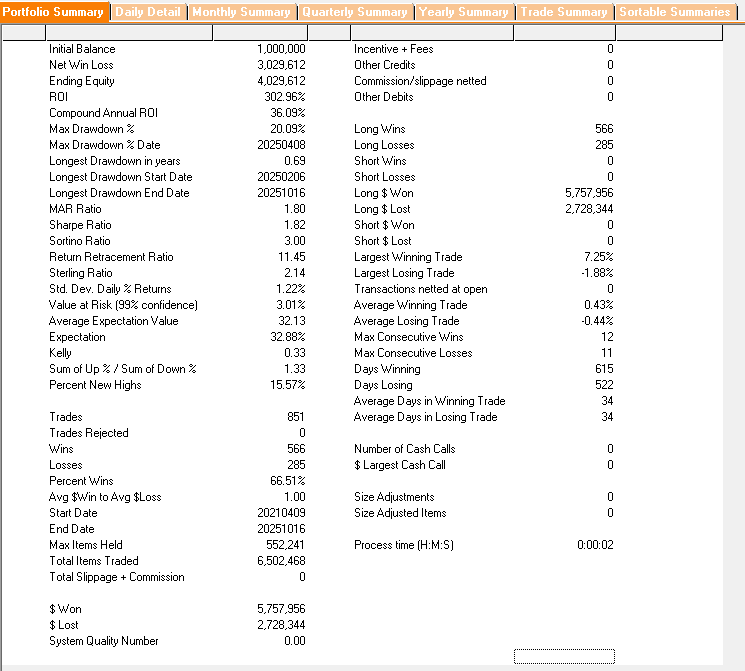

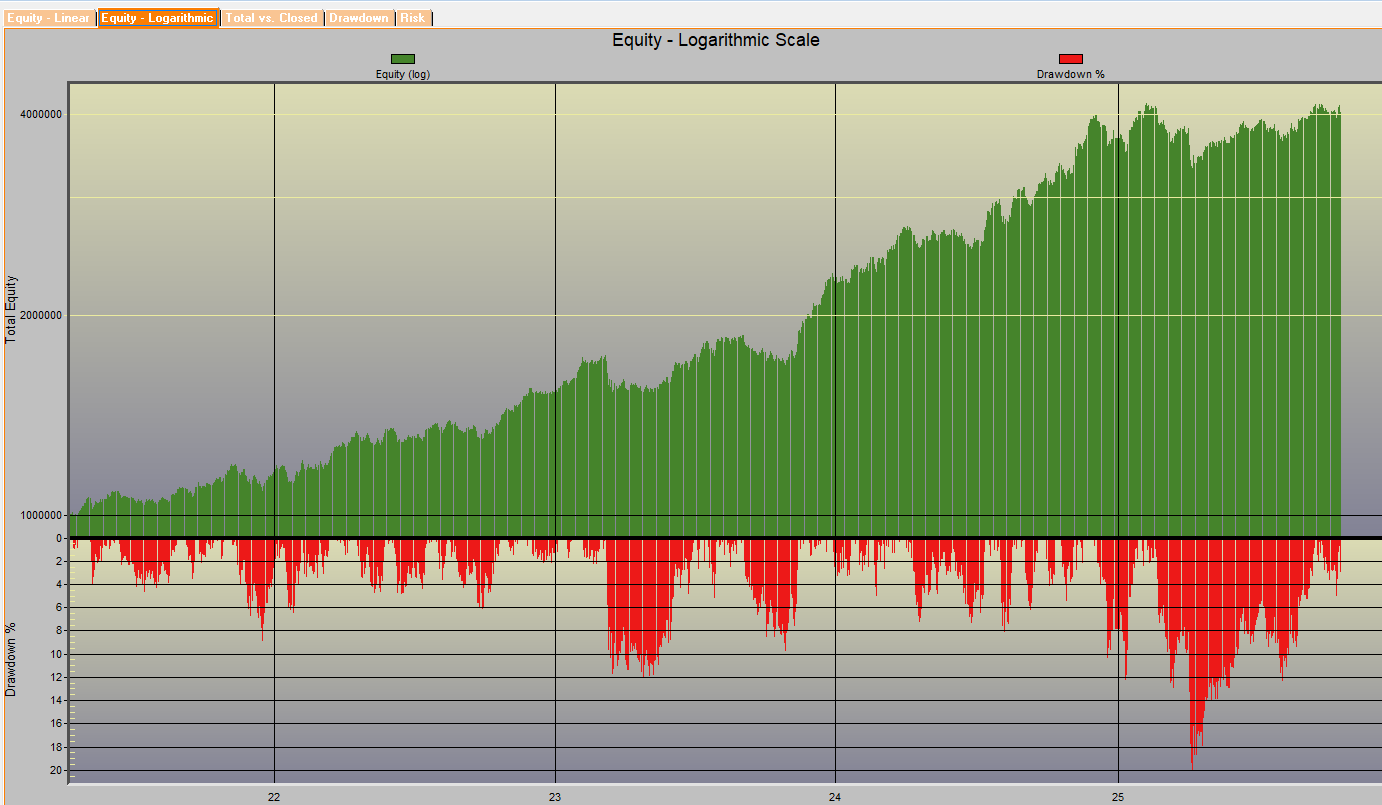

I know with 100% certainty that this kind of trade sizing does a far better job of managing account volatility and would be a good improvement to P123.

Thoughts?