Dear all,

Here is something interesting.

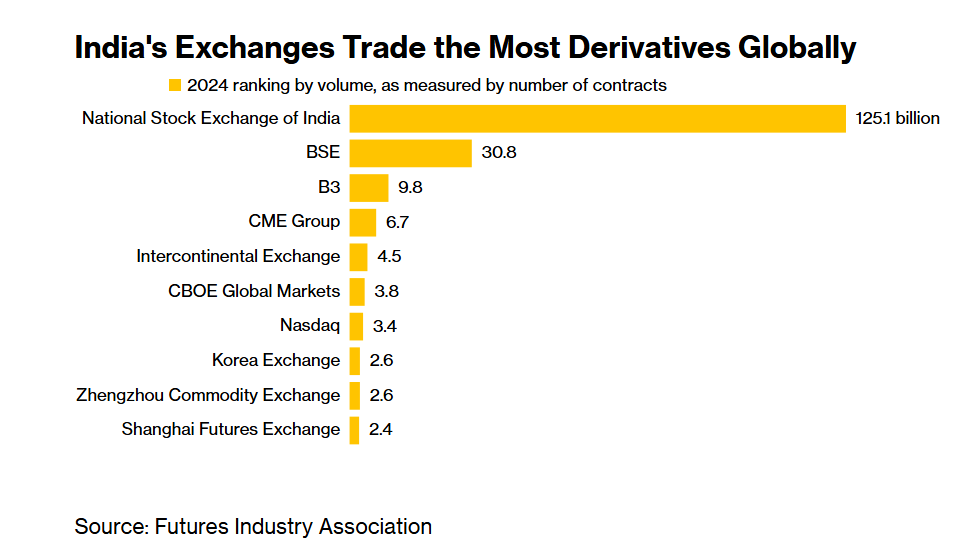

India is currently the largest derivatives market in the world by far.

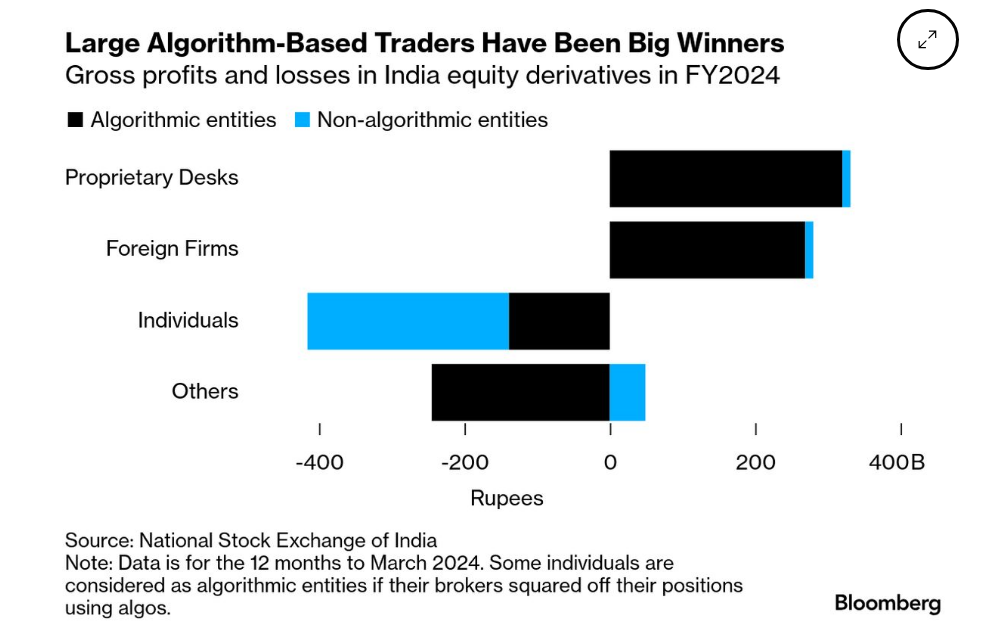

According to SEBI (the market regulator in India), over 90% of futures and options traders lose money. Among the small percentage of traders who were profitable, profits were highly concentrated. The top 1% of profit-making traders takes approximately 51% of the profits while the top 5% received approximately 75% of the total net profits respectively.

The study also finds that large algorithm-based traders running proprietary desks and foreign firms are big winners while individuals who trade using algorithms lost money (the losses are less than non-algorithms individuals).

It shows that it is necessarily to be in the top of the game in order to make money in futures & options. (the same applies to perpetual futures in cryptos). Unless you are at the very top, it is probably a better idea to pay someone else to run the books than trading by yourself in futures & options.

Regards

James