To accommodate users who are unhappy with the changes we recently made to the production website, we will be offering a temporary secondary website, alt.portfolio123.com, that will roll back some of those changes. It will be launched on March 24 at about 11:30 CST. Please use this site to test your systems to verify that any undesirable results seen after the last release have been resolved. This is not like the previous beta site: changes made to your systems on this website will be permanently saved to the production database. This website will behave like portfolio123.com except that using the North America region will not work: users should use the US and Canada regions like they used to.

For this website, we will be rolling back the two changes that are the most likely to have affected your systems: bars will once again exclude holidays, and the -Ind factors will once again include non-primary listings and will no longer be based on the new regional universes.

What will be the plan from here, having two websites permanently or rolling back the industry part for the main site too?

The question is, will this new site only be for adapting ones models or will the industry changes be rolled back for good?

Since my models are hit big time by the change in the industry part I would really love to see this bee rolled back on the main site.

The alternate site is to figure out what can be done to make the transition smoother for some and to give you more time. Also to help us decide new functions that exclude holidays. For the Ind factors we’re not going back; only Primary stocks for the region will be used in production. But you can create your own using Aggregate that replicate the old way as long as the starting universe includes all listings including non-primaries.

“But you can create your own using Aggregate that replicate the old way as long as the starting universe includes all listings including non-primaries.”

And how do I do this?

Any why not flip that around?

Let the functions as they are but ask users to build their aggregate to obtain the new functionality?

I am also getting the “No server available for request” error.

The Alt website is also showing as not having up to date Price and Fundamental data. Is this going to fixed? I would like to be able to use the Alt website to manage my trades next week, since I’m not confident in the main website.

I get almost the same hits on my ports from 7-10% with this site.

PLEASE ADVICE how I can built a logic so I get my old industry groups logic:

“But you can create your own using Aggregate that replicate the old way as long as the starting universe includes all listings including non-primaries.”

dnevin123, atw, sorry about that. The alt site only has a FactSet engine. We’ll add a S&P engine soon.

The alt site only rolled back two changes: the holidays in the prices and the exclusion of non-primary stocks for the pre-built Ind factors. The time series (that affects technical factors) for industry classifications like sector & industry have not been rolled back. We will review it.

We’re trying to build something unique , that can scale globally, that is cohesive, with features that exist nowhere else as far as I know. The new Primary, non-Primary definitions for listed stocks in regional universes (USA, Canada, North America for now) are new. Now that we’re looking at the big picture it forced us to review everything like Industry factors . And sometimes there is no clear right answer. Thanks again for your feedback and patience. We’ll get there.

Thanks marco. Is there any chance the alt site will be ready to work with Compustat and have up-to-date data before the weekend? I would like to be trade my Live Ports on Monday, and similar to Hugh don’t feel I can do that with any confidence the way things stand currently.

After testing a bit, I like the new functions and they also sound more stable and sensible. When I backtest industry momentum, the new functions seem to give more robust results than the old functions (tested using the aggregate function).

I do understand where you are going; one big data base with a ton of countries in one big trading system. You will not only be able to capture a stock and industry factor, but you will be able to capture a country as a whole factor (country momentum would make really sense then, it works really well!). This would be great alpha machine! Super great approach, way to go!

I have a rebalance on Monday and my models are hit with 5-10% degrade of performance.

I really do not know what to do.

I need either the old industry logic or I need a workaround so that I can mimic the old logic (my assumption is I need all primary and non-primary stocks in the industry definition, my models seem not pick any non-primaries with the new logic).

Please help me!

Design decision to include non-primaries in the (US) industries (as long as we do not have a ton of countries in the one big database):

From what I have understood is that non primaries are not included in the US industry with the new site.

But: It makes perfect sense that an industry factor is build based on all stocks that are traded in the universe of a country (no matter if they have their main listing somewhere else). That is one of the biggest advantages of the US Stock market: I am already trading international stocks! The US sucks in capital from all over the world and the bad countries (China!) I can exclude via a buy rule on the system.

If a model trades on industry momentum (which is one of the strongest trending factors after small size / low liquidity and stock momentum) and the non-primaries are not included, it is clear that performance gets hit because your baseline number of stocks gets reduced, since the international stocks (besides Canada) are not available and by definition we will never have all countries available in one big world universe (or at least not now or soon).

Have a look at the performance of ICL, Israel Chemicals (my model picked that based on strong industry performance and other factors). My models captured that stock extensively (for months and months this year and last year). The stock made me very good money.

Why should ICL not be anymore in the CHEMSPECIAL Industry of the US (at least I do not have the Universe of Israel). The factor the industry is loaded with (which gets captured by momentum) is right now more important than the country (which we do not have or at least not soon).

The US is extensively loaded on growth; international stocks (which are traded as secondaries in the US) can produce alpha if value (value-momentum) is outperforming growth, because they have more value / cyclical / inflationary sensitive (e.g., going up when inflation is going up) stocks. And that context is captured by industry momentum (but only if secondaries are included).

If you stick to your design decision…

Which is of cause up to you, then please give an alternative to users that want the non-primaries in the US industry definition.

Please, that would be super great!!!

Andreas, have you tried implementing industry momentum through the aggregate function? For example this for 26-week momentum:

“Aggregate(“close(0)/close(130)”,#industry,#Avg)”

You say you get 5%-10% reduced performance, have you tried a 50-stock rolling screener test before and after the change? I don’t think a 10-stock simulation is a good way to measure performance for a small change in input data.

Thank you!!! I will test that out!

All models that are hit have by definition 20 Stocks, they do not have always 20 Stocks because they raise cash based on

a rank filter and some are using EPS estimate filter.

But that does not mean they are not robust, it makes sense that they do raise cash if they can not find stocks in the micro cap space, if those stocks do not have high ranks (Rank > 96 or even 98) or in other systems do not have positive earnings estimates.

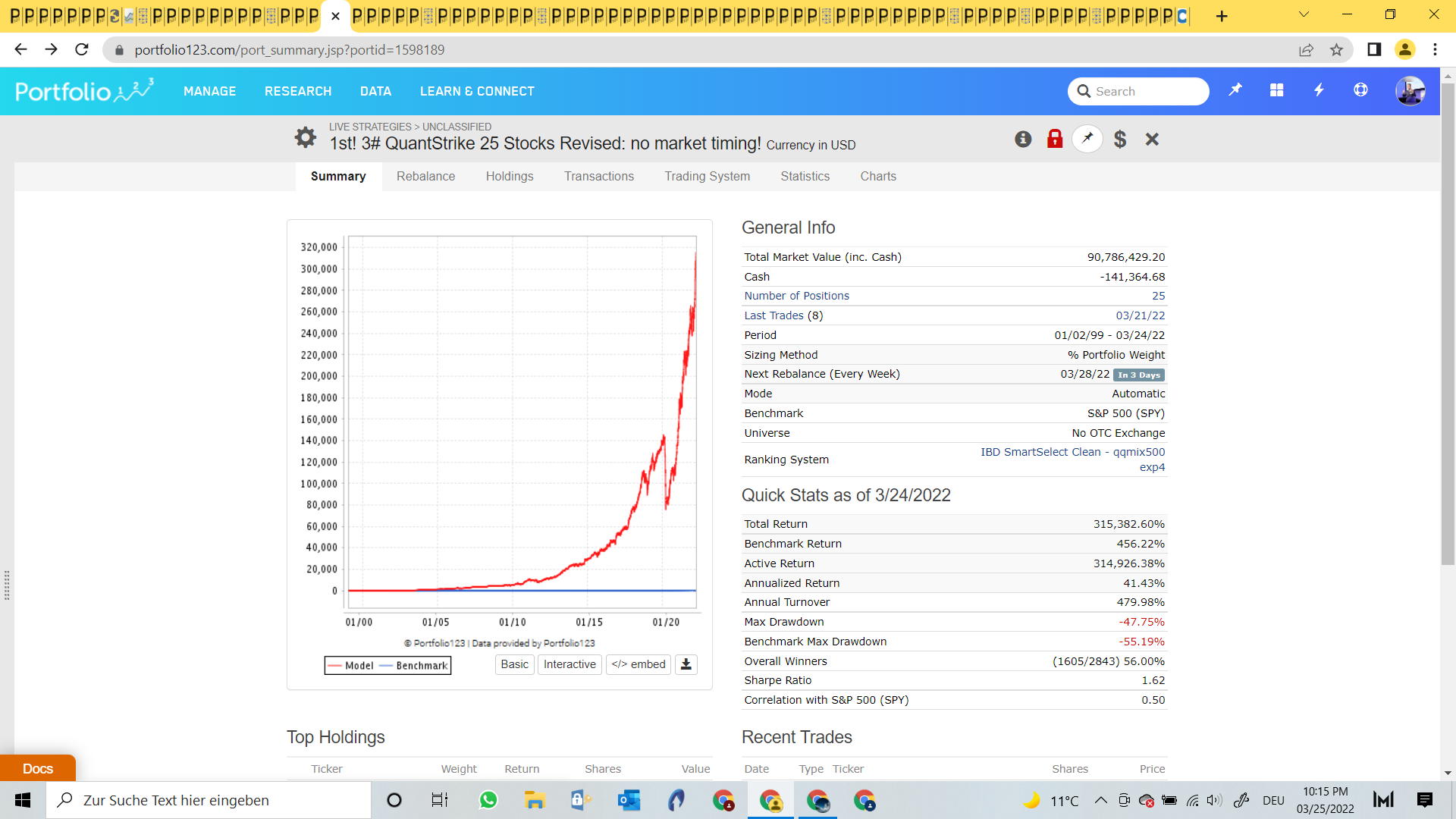

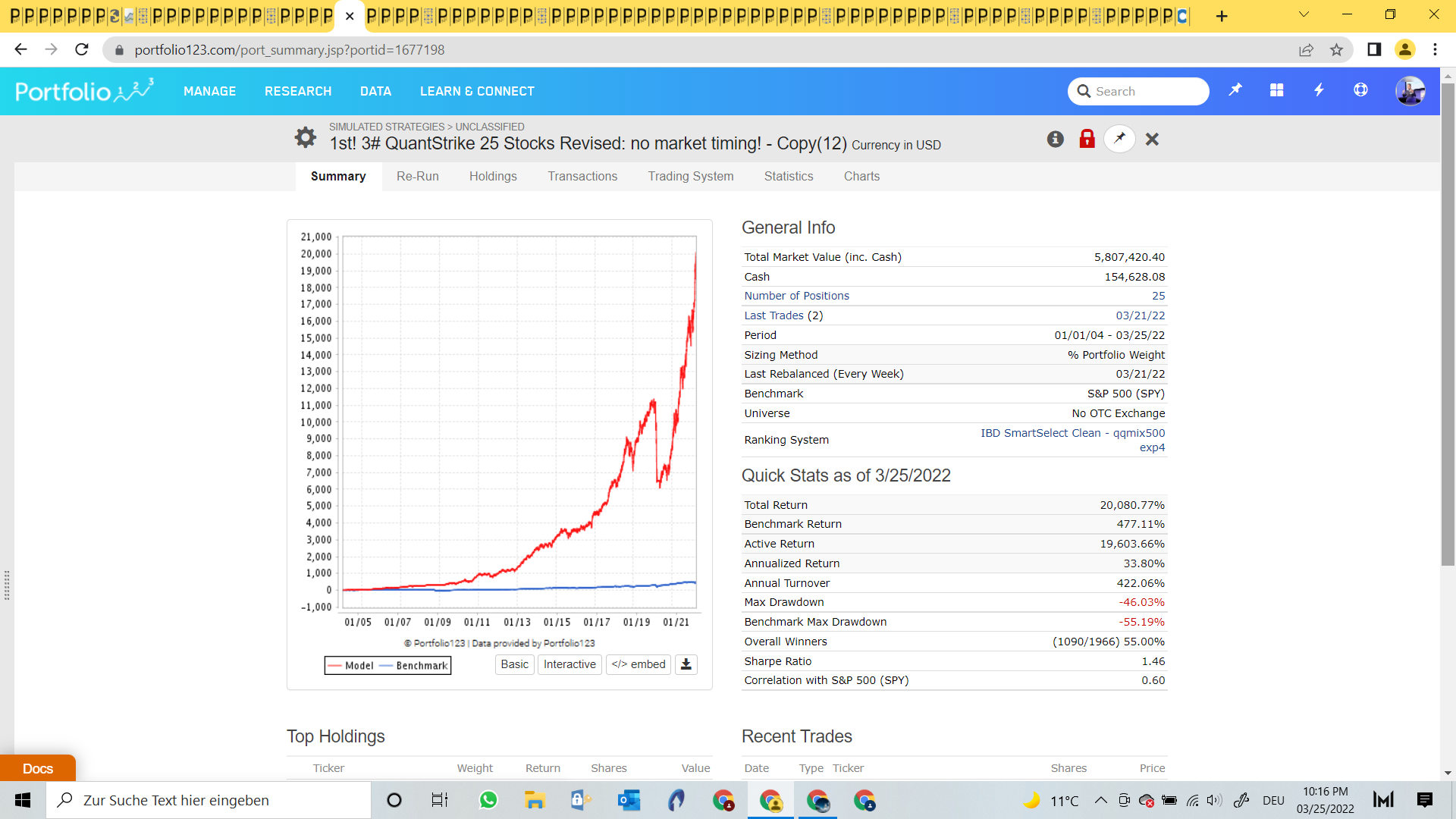

Here the performance difference of my designer model (the last backtest I made within the old site could replicate the perormance, now that performance is gone!)

25 Stock model!!!

(I revised it and got rid of the market timing once, performance hit happens no matter if with or without the timing!!!)

Almost a 8% hit. Very robust model, no EPS Revisions in it, almost always fully loaded (e.g. has 25 Stocks).

So this performance hit has nothing to do with me trading systems which have less than 10 Stocks.

I will inform my sub on the model (800 Bucks per month by the way), that until further notice the model should not be traded!