For those of you who trade nano caps or take more than a day or so to get out of positions, do you trade more aggressively if a stock has had bad earnings or a significant drop in rank?

I ask because even in these cases, I usually just put in a limit order at a price close to the last trade, let it sit for a few days, then update as necessary. But perhaps it would be better to be more aggressive from the start?

I’ve wondered the same. I try to avoid being too aggressive to limit slippage. I’m not sure what the best is though.

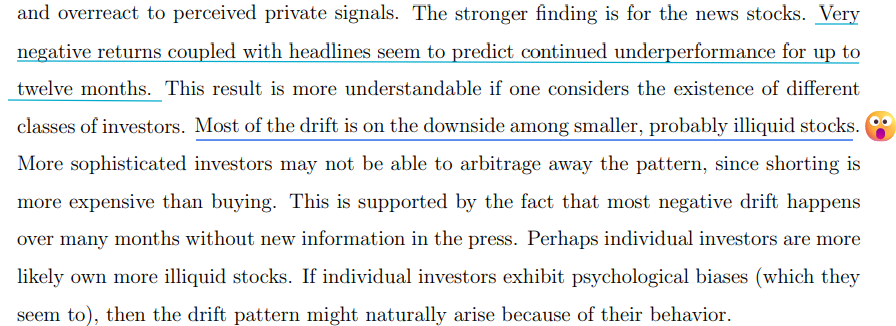

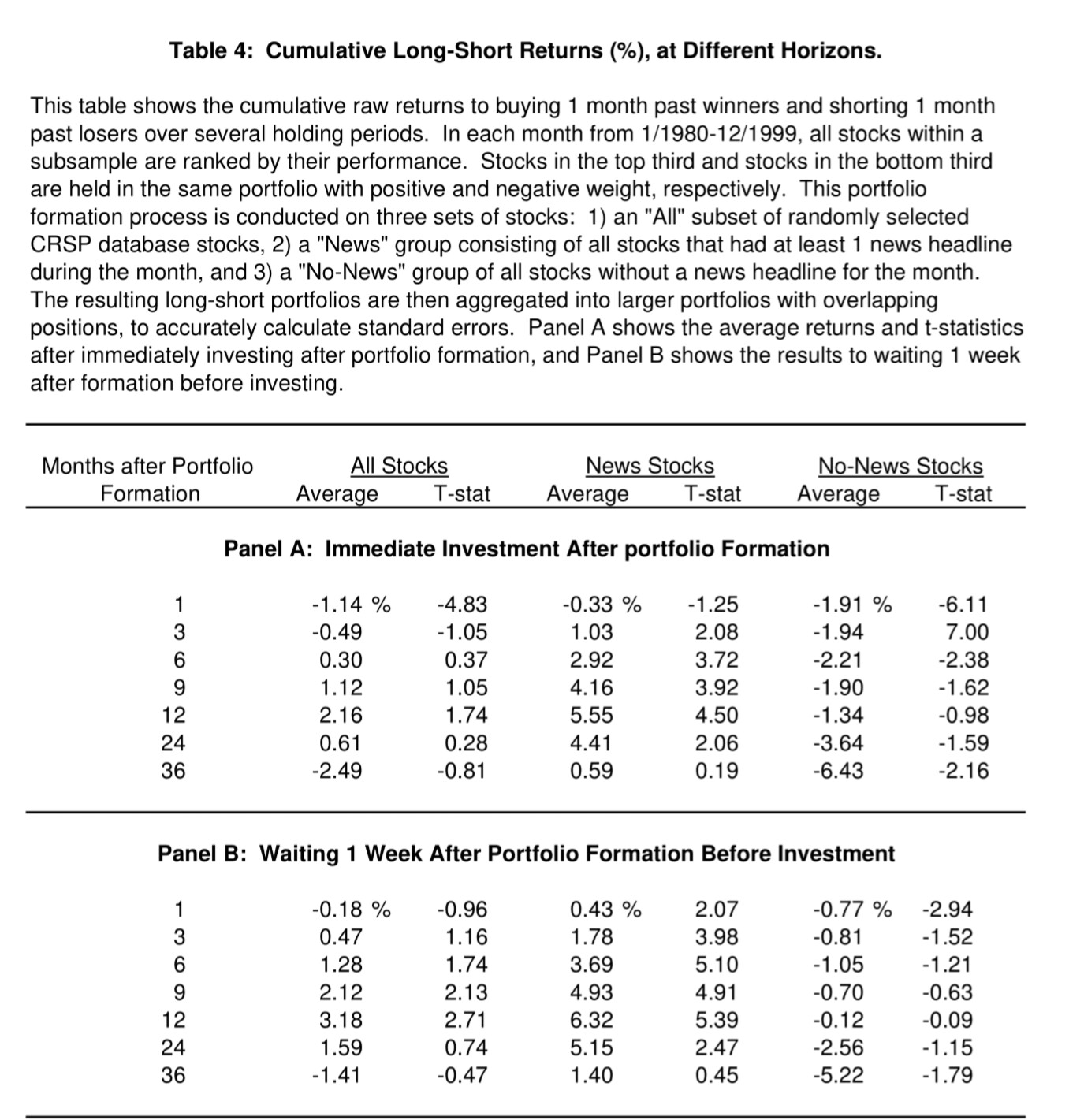

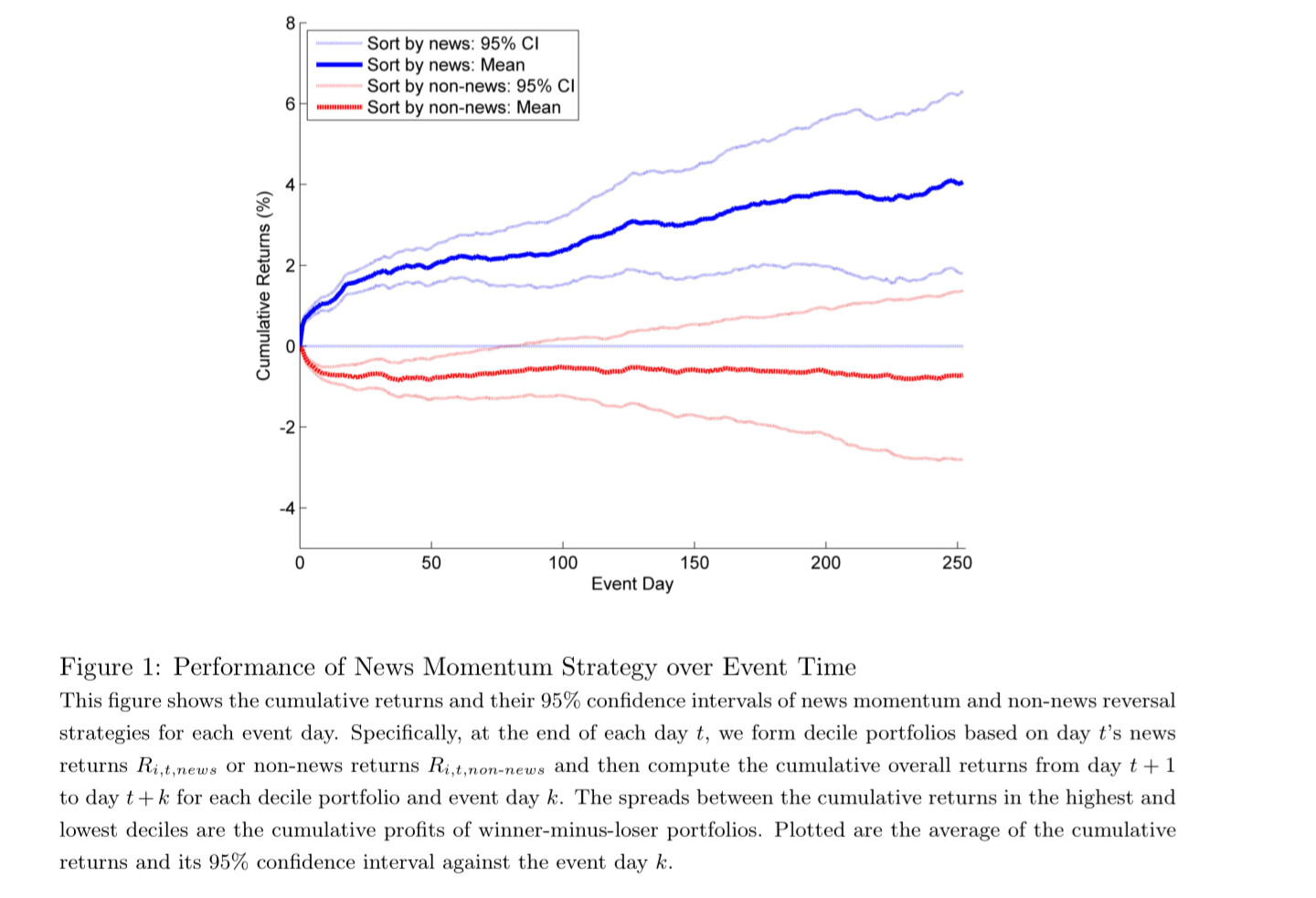

Also because there’s not a lot of liquidity for smaller stocks I’ve seen analyses showing that on average the stock will drop the full amount already by market open or sometime on the first day. Then the average return for the next 30 days is still positive, although a smaller average return than stocks with positive earnings nonetheless. Someone on the forum checked a while back I believe and there has been some studies on post earnings drift.

I say average with everything because the distribution of returns is massive.

A lot of these stats are with small caps and larger though. I wonder sometimes because market information efficiency with nano caps is less likely. Sometimes I do see stocks that continue to drop an additional 20-40% after a bad earnings even after the first day. Other times they gain 20-40% after day 1.

Yeah, it’s a difficult question. I could see it both ways: maybe post-earnings drift applies and the bad earnings stocks continue to lose so it’s better to get out quickly, or maybe the increased slippage you’ll probably experience as you try to bail is such that you’re actually better off taking a little more time.

I have tried Interactive Brokers’s various algos in the past and was never very satisfied (though it has been several years since I last experimented with them). Perhaps I wasn’t setting them up correctly, but they seemed to behave in counterintuitive ways (VWAP would do nothing when liquidity was high and spreads were narrow, then as spreads widened and liquidity evaporated, the algorithm would start to trade wildly). In the end I just went back to limit orders.

Thanks for the academic papers. I’ll try to take a look at them and let you know what I think.

I do add this to my model:

eval(WeeksIntoQ < 2, price / close(7 * WeeksIntoQ + 8), 1)

Which ranks companies higher if they had a recent stock price increase after an earnings release (which probably means increasing earnings), and ranks them lower if decreasing stock price around earnings. It only added .07% annualized return to my model though tbh. I never found a combination that added more than that when taking into account the most recent earnings statement. Perhaps because our models are already taking into account all the financial metrics anyways - if they had a bad statement, their rank probably dropped. If the rank has dropped enough then I sell.