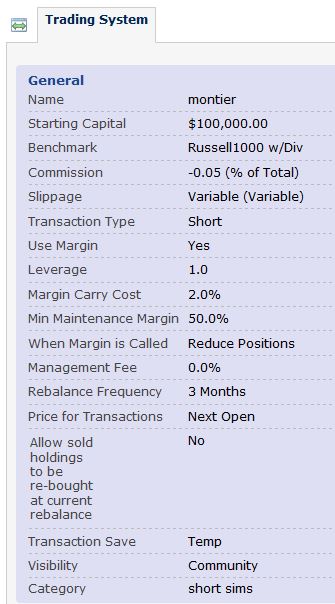

Can I ask for help from the community and P123 staff to check I am doing things correctly when running a short simulation…

(I have just put a similar posting for ranking)

slippage: → should I use negative or positive numbers? If negative, I assume I can’t check “variable slippage”? (but would have to set it to a fixed negative number)

Leverage → 1 for an Interactive Broker RegT Margin account?

Margin Carry Cost → Anyone knows what it could be for Interactive Broker RegT Margin account? (trading USD only)

Commission and slippage should be set to positive numbers. The thread you referenced is likely from prior to P123’s launch of shorting sim’s.

Leverage is something you choose - how much money are you willing to borrow. 1 is a good setting to start (100% of capital).

Margin carry cost has to be looked up stock by stock. Can do this on IB. They have a tool that’s available from the trader’s workstation that shows short borrowing costs. It’s simple and easy to use. For the most liquid stocks on the SP500, it’s typically under 0.5%/yr. For small cap stocks or heavily shorted stocks, it can be 20%/year or more. It’s been going up significantly in past few years. Many of the smallest stocks can’t be shorted at all. However, it’s possible for a highly traded, large cap - to have a borrowing cost over 15% or 20%/yr - if there is a lot more demand to short than shares to short. This is the hardest thing to come close to in P123 for backtest accuracy - there is no real accuracy in the borrowing costs. Some stocks can hit 40-50% AR borrowing costs.

50% is fine to use on min maintenance. During 2008, Merrill changed these on some pretty good sized customers without warning and forced people to close out positions (there were settlements and lawsuits around this) - so some of this depends on the underlying health of the broker.

I have the flu at the moment and am not thinking all that clearly, but hope this helps. I have actually made a slightly more money shorting stocks this year than being long - so that seems to be an interesting underlying market commentary - not sure what it’s saying exactly, but feels like perhaps we are in / moving into a ‘stock pickers’ market from a broad index outperforming market.

Sorry to read you have the flu. I hope you get better soon.

a) This is very helpful and does answer my questions - thank you very much.

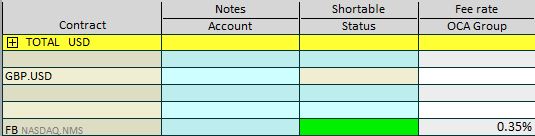

I think I found the field in IB TWS you were refering to. I already had the “short availability status” set-up in TWS. I believe the one you are thinking of is called “fee rate” - Is that correct?

I attach a screenshot of TWS with Facebook as an example (8 Dec 2014 - circa 22h30 GMT)…

b) I will read the 2 docs tomorrow once I have a period of calm.

But, yes - finding a short strategy that can be simulated “reliably” seems more complex than the long side. I intend to limit myself to stocks with a lot of trading volume i.e. SP500 or R1000 to “keep real / implementable in real life”.

Well done on making money on your short strategies this year!

c) Did I miss some threads or there is not a lot on the forum on short strategy discussions? I.e. I only found a couple of threads.

Then I found this - which gives me some possible starting points → Short Selling

Any other sources of inspiration come to mind?

If P123 decides they want to incorporate more realistic carry costs into short sims, here’s an idea:

Not sure how much it costs, but you could pay for an options database that gives you the EOD bid/ask price data for at-the-money options. You can then construct a synthetic short to calculate the implied carry cost. It usually matches up pretty closely to what the real-life carry cost is. It has to, otherwise short sellers would buy synthetic shorts instead of paying the short carry cost. Main downside is there are some stocks that are shortable but have no listed options. Another downside is that with low liquidity stocks, the bid/ask spread on the options could be so wide that the implied short carry cost could be higher than the real one. However, I think the data would probably be reasonably accurate for mid-cap and large-cap stocks.

See pages 3 & 4 for overview of ‘market borrowing costs’ in 2002 - they have (allegedly) gone way up since then (at least those are the anecdotal claims I’ve heard in the popular press, but don’t have the numbers in front of me).

I am definitely paying more than .5% on average to short even with a pretty conservative universe. My guess is it’s between 1-2% blended, even mostly from the R1000 - that’s over trailing 12 months or so. I don’t keep track honestly, although I used to. I rely on a large basket of positions (20-40) to smooth out total costs and set the ‘borrow cost’ much higher in the sim’s (say 2-4% depending on the universe).

And with higher turnover systems, and or really big down markets, you may not be able to short the stocks or sectors you want/need to short precisely at the time you need to short them.

I would not suggest more than (at most) 1% of any port. in any single short. (less in the first year). You can get a huge ‘loss’ (in theory unlimited). My experience is that even really ‘bad companies’ (horrible fundamentals and technicals) can rally 50% to 100% in a day or two at times (which means big losses if you are short them). But, I’ve also had about 5% of my positions make 50-100% in the past 12 weeks. Point is, shorts can be very volatile. Tread lightly to start.