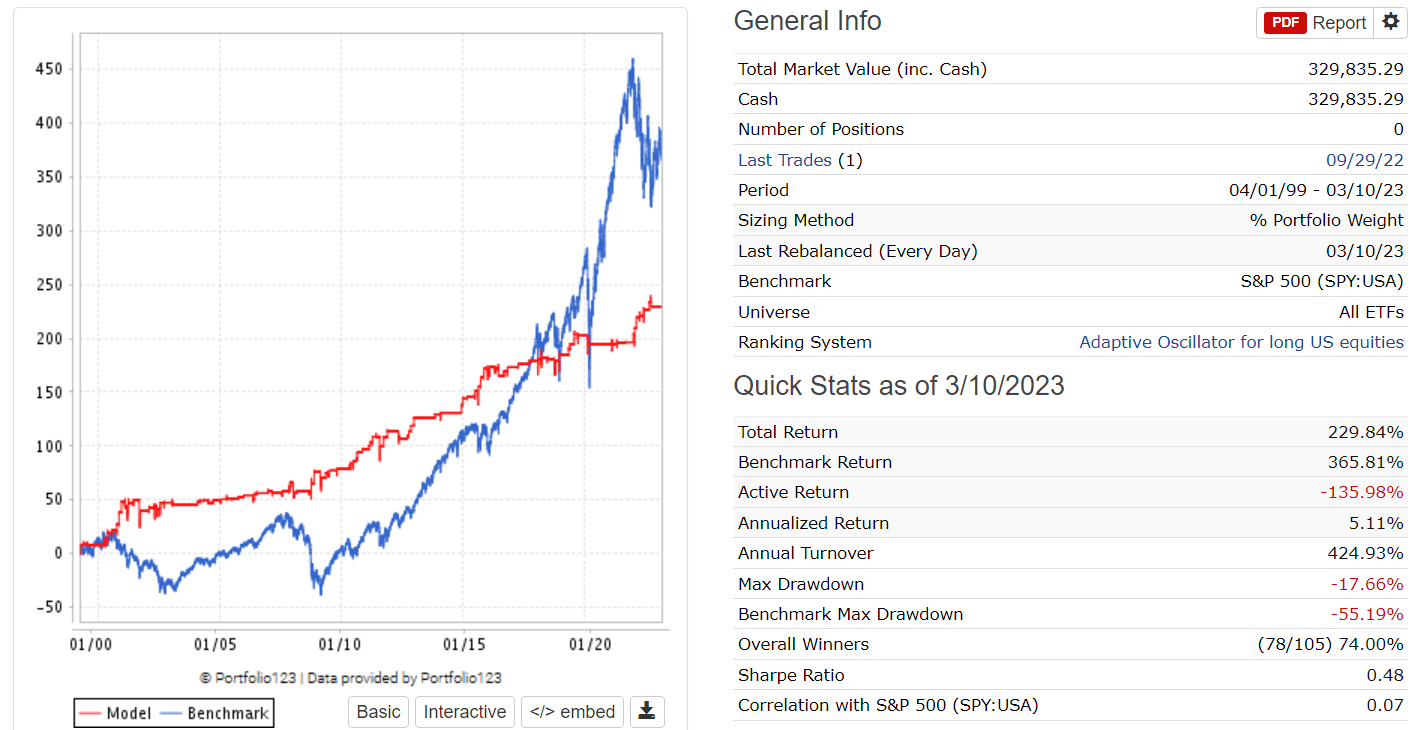

I’m looking to replicate the results from this article. It’s shows a simple system that buys QQQ when RSI(3) < 10. However, it filters out trades where the close of the previous day is in the upper half of the candlestick. The author shows significant improvement from the filter, but I am not seeing any benefit to adding this buy rule.

Do you guys see anything wrong with the Setvar rule?

How do I see the output of the Setvar rule after running the sim? It just shows up when using showvar in a screen.

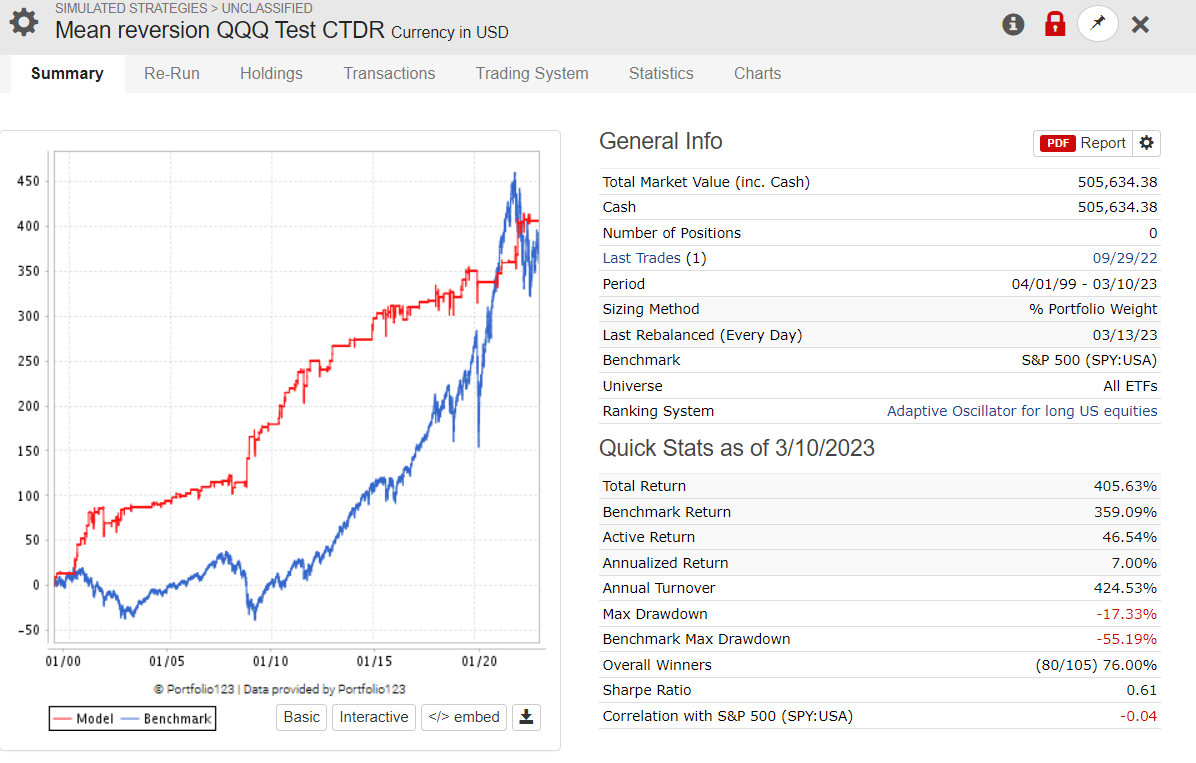

Thanks for the responses Changing the transaction price to next open matches my intended system of placing the trades before the open. I’m still not getting much benefit from the second buy rule requiring that the previous close must have been in the lower half of the candle. Here’s the corrected equity curve with the open price. Not bad and it looks good if in IEF when not holding QQQ. Also, the system was only active 8% of the time leaving capital free for bonds or other trades 92% of the time.

Yes, I switched the exit rule to my preferred RSI(2) > 70, but RSI(3) > 50 gives very similar results.

I still cannot find the output of the SetVar function which is important for troubleshooting…