I understand that I can use “book simulation” to test a “sleeve approach,” defined as:

“Sleeve approach refers to the use of a core portfolio, often consisting of a broad-market index fund or exchange-traded fund, combined with several satellite portfolios, each targeting a different investment factor. The core portfolio is often referred to as the base or neutral portfolio, and the satellite portfolios are referred to as factor sleeves.” (Kalesnik & Kose, 2018)

I see that there are very few “books.” in P123. Has anyone made any assessments of the sleeve approach to multifactor investing, or gained any experience, or used this approach themselves?

I see that there are some studies that seem to suggest that this is a good approach:

- “Sleeve Investing: How to Make the Most of Factor-Based Strategies” av ERI Scientific Beta (2019)

- “Sleeving: A New Approach to Factor Investing” av MSCI (2019)

- “Dynamic factor sleeves: Diversify smartly” av Research Affiliates (2017)

- “Smart Beta and Beyond: Maximizing the Benefits of Multi-Factor Investing through Dynamic Factor Allocation” av FTSE Russell (2018)

- “Enhancing factor-based equity allocations with dynamic sleeves” av Vanguard (2019)

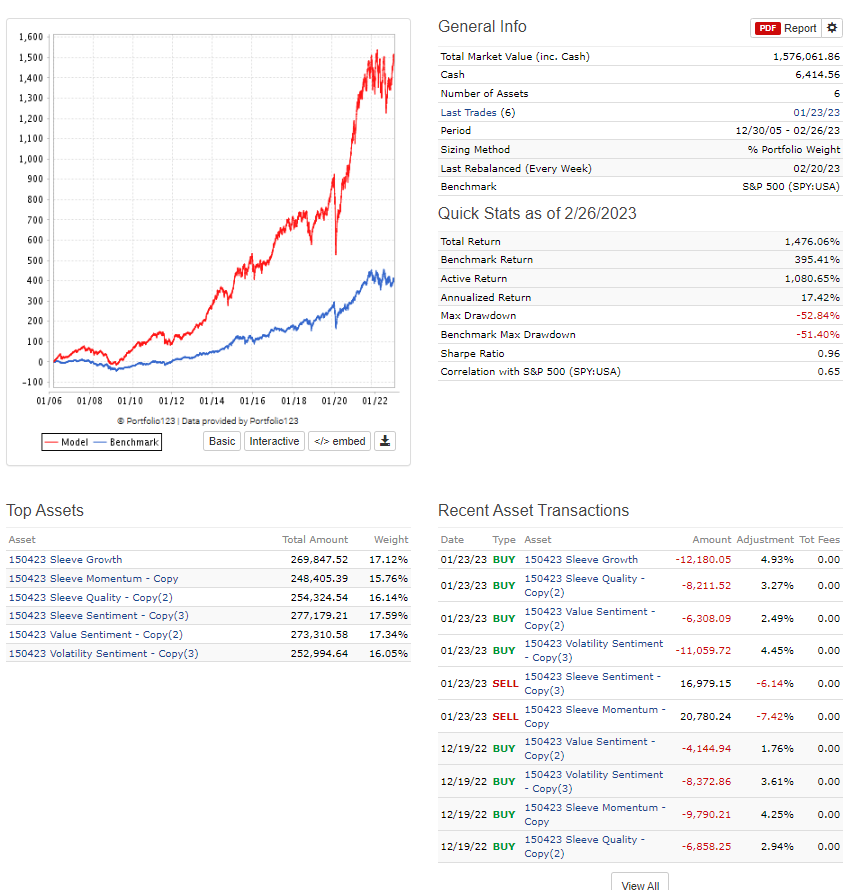

"I tested it out by breaking down one of my EU ranking systems, but removed the size factor, leaving me with 6 factors. I ran simulations on each of these factors, and then balanced them in the ‘book simulation’. Here are the results:

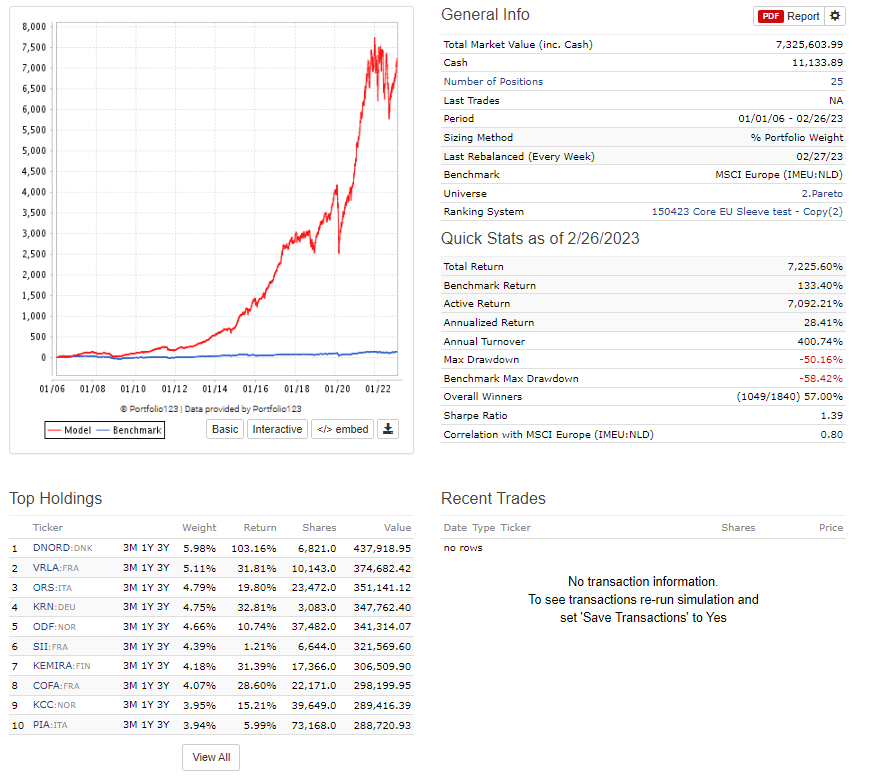

I then ran the combined system with the 6 Equal-weighted factors, and here are the results:"

It may be that I have made some mistakes with my test, but it is clear that the results are very different on the two methods

It was tested on the same universe, same portfolio size, and same period.

I remember reading about several studies that found the “sleeve” approach inferior to combining factors. The reason seems quite apparent to me. Investments, in my opinion and in the opinion of a number of other successful investors, should not be looked at from only one angle, but from a number of them. If you’re using the “sleeve” approach, you’re evaluating each stock you buy from only one angle. If you’re using multifactor ranking, you’re evaluating each stock from a wide variety of different angles. The companies you invest in will therefore be safer and more able to adapt to and survive challenges. The “sleeve” approach strikes me as imprudent. A lot of the companies you’ll be investing in will be outstanding in only one aspect. The only way to beat the market is to invest in really superior companies.

I always think of the analogy of buying house when investing. If I would use that anology in regards to what yuval mentioned, it would go something as follows.

Let’s say you buy 4 houses. For one of them, you only look at how cheap it is compared to the number of squared foot. For the next, you look at the quality of the construction only. For the third you look only at how fast the prices of the houses in that neighboorhood have been rising. For the fourth you only check the quality of the tenant, whether he’s been paying his rent every month and if hes a decent person.

If you would base your investments - for each of them - on only one criteria, you might end up with a house that is cheap compared to the size, but it might not have a roof or it might not have a stable foundation. You might also end up with a house with high class construction, but way overpay for that house or have a terrible tenant in there that might mess up your appartement. The house in the neighbourhood that was getting a lot of interest might be a terrible investment because of bad characteristics of the house itself (‘idiosyncratic’ reasons). Finally, if the tenant is great and the rental agreement is all fine, that could still leave you with a very small appartment in a bad neighbourhood.

So you’re better off checking the house from all sides. Lucky for us, we are investing in stocks and the data is available with a few clicks, so you don’t even have to go anywhere to check the thing you are buying.

It’s nice to see that that form of reasoning is reflected in the results you got. That makes me feel more comforable about my own reasoning too.

Multi-factor ranking will undoubtedly give the best risk-adjusted performance. Focussed trading systems will give the best performance in bull markets, but will also get trounced in bear markets. If you are an expert in a certain niche and willing to take extra risk then a focused trading system can be a rewarding investment approach. But you have to know when to get out.

I think the ‘sleeve approach’ can work but not with common factors. More like a multi-strat approach where each sleeve is focused on one style or theme. If value was one sleeve, you would still need to design a solid and intelligent value strategy that tries to remove value traps and lower risk of crumbling fundamentals and so forth. Make it the best value strategy you can. Same with growth and quality and sentiment and low volatility.

In the end, you’d probably still have a multi-themed factor ranking for each sleeve. But each sleeve would have a massive factor tilt towards one style or another. Just be careful it doesn’t lead to over-optimization.

You have to consider that if everyone is optimizing for the same small and micro caps on this platform with a multi factor model with the same data sets then a few things may happen:

-

Many will arrive at somewhat similar stock rating systems that…

-

Select many of the same stocks which are likely micro or small caps that…

-

Cause the future performance of those holdings to do worse than they may have due to overcrowding.

While a sleeve (or factor heavy per strategy) approach may not produce superior returns on paper or currently compared to multi factor models they can provide an avenue away from crowding into the same stocks as everyone else. They can provide market beating returns as well as long as they are properly designed. But the key is that you need to cover your bases for all market regimes (aka growth, value, quality, etc), avoid factor traps, and avoid ovrroptimzation.

Jeff

“A timed multifactor portfolio

leads to a 20% increase in return relative to its untimed counterpart.”

Has anyone tested a timing approach to factors?

My understanding is that Yuval tried it out, but it didn’t help and only led to increased portfolio turnover, right?

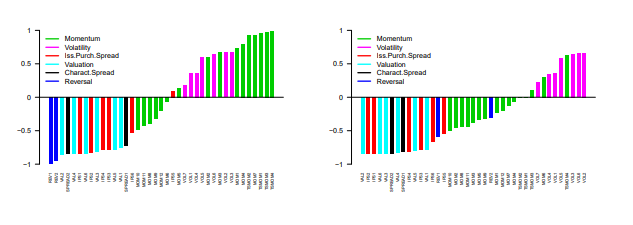

In the study (Posted: 3 Apr 2023), it seems that timing factors based on momentum and volatility produce the best results over time.

Our analysis reveals that factor timing is indeed possible. Predictability is not

concentrated in short subsamples of the data and does not decay in recent time periods. In short, factor risk

premia are robustly predictable. Our evidence reveals that factor timing is greatly beneficial to investors

relative to passive “harvesting” of risk premia

…

The analysis

reveals that versions of momentum and volatility signals are able to provide improvements on a broad

basis. Other signal classes (valuation spreads, characteristic spreads, reversal and issuer-purchaser spread)

provide improvements, but the results vary more strongly depending on whether we study improvements in

raw returns, alphas or Sharpe ratios.

Has anyone tried such an approach?

By the way, from page 44 onwards, there are some good descriptions of the different studies they have covered.

1 Like

Here’s one way to do this. Create a conditional node. The formula could be, for example, Close(0,GetSeries(“IWD”))/Close(210,GetSeries(“IWD”)) > Close(0,GetSeries(“IWF”))/Close(210,GetSeries(“IWF”)). (IWD is Russell 1000 Value and IWF is Russell 1000 Growth.) If that evaluates to true, you use a value formula like earnings yield. If it evaluates to false, you use a growth formula like operating income growth.

The idea behind this is that during periods that value factors just don’t work (e.g. 2019), you’ll be favoring growth factors, and during periods when value factors are resurgent (e.g. now), you’ll be favoring value factors.

I can’t swear by this, but I can suggest it.