no, I mix them,e.g. I have strats with different ranking system in one book.

And i mix Yuals ranking system with other ranking systems…

For example Yuals ranking system (with my buy and sell rules) is a super bottom runner (e.g. it is extremly strong after big drawdowns), I want that in my book, because other strats (which load more quality) are a bit weaker (they still go up hard)

Strategy books are the way to go:

If you have a new Quad 1-2, I found no way to know before which ranking system does best, so best to mix them.

Also you can add strategies to books with “Seldom” edges with only 5 -10 Stocks (e.g. they do not load stocks all the time, because they can not find any…), for example actuals (which are new).

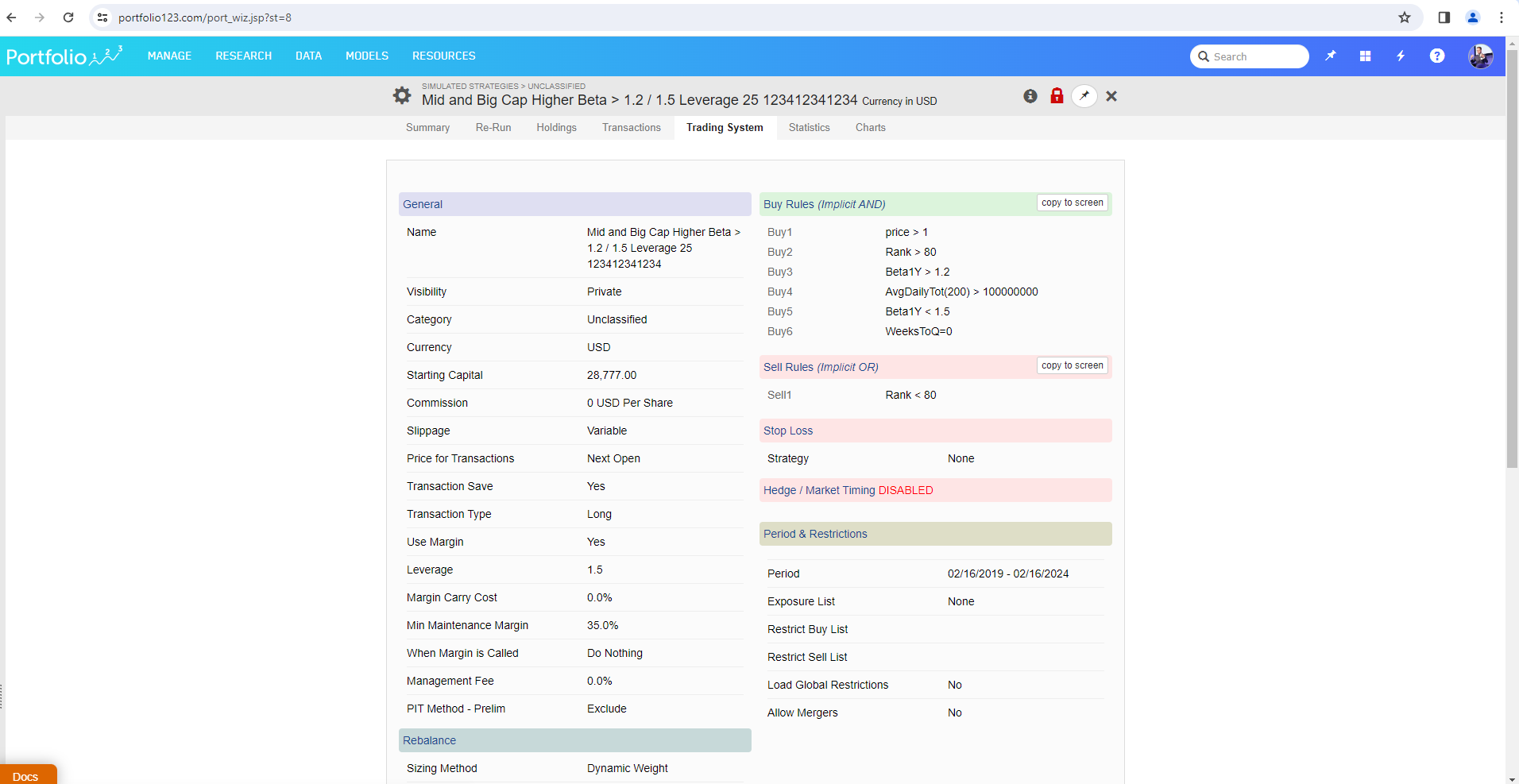

FRank(“ActualGr%PQ(#EPS)”,#all,#DESC, #ExclNA) > 80 or FRank(“EPSExclXorGr%PQ”,#all,#DESC, #ExclNA) > 80

My general assumption: The data from p123 got much better in the last 10 Years, they the earnings estimates got better, now the actuals, also my best guess is that there are less N/As in the data (so broader ranking systems like Yuals are stronger)…

Keep on testing, I find edges every month.

If I hold on to my design rules My system design rules for Portfolio123.com 9 out of 10 Systems reflect the backtest in OOS, so I take the risk also to use systems with not too much OOS.