[quote]

pmalis: What i’m curious about is whether I will see a turnaround in small value, or whether they will continue to underperform. What do you all think?

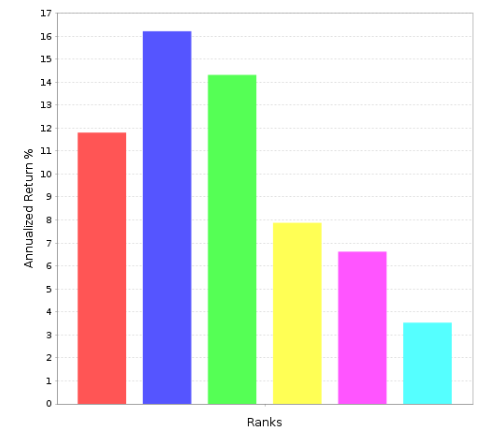

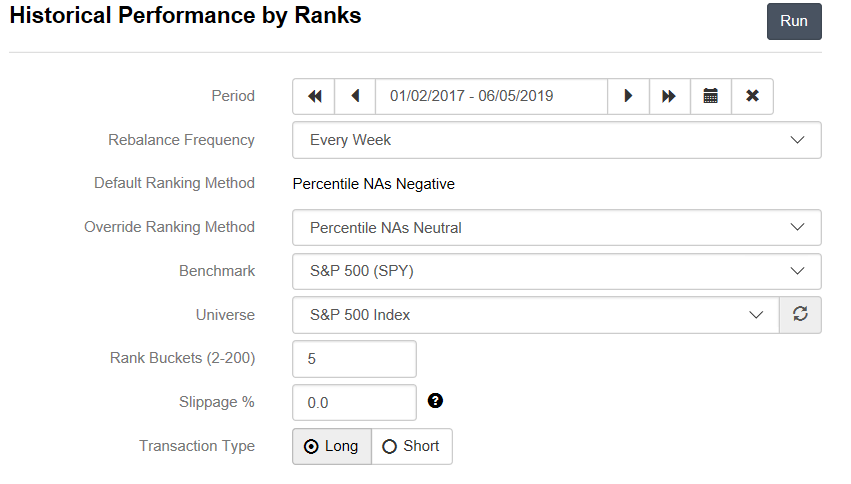

[/quote] If I may, Paul’s original question remains and the underperformance is not limited to smallcaps. The P123 public ranking system “Basic: Value”, using the S&P 500 Index universe, annualized returns, weekly tests, and Percentile NAs Neutral from 1/2/2017 until 6/5/2019 shows results nicely (strongly, strangely?) inverted from the desired. The ranking system’s factors are all price ratios (to earnings, projected earnings, growth, sales, cash flow, and book value). The implication to me is that recently the most expensive stocks have been very strongly favored. I would like to know why, so that I can recognize and understand this kind of “regime change” and perhaps avoid or take advantage of it in the future. Secondarily, I wonder if this inversion is some kind of “irrational exuberance” period that will cause a temporary meltdown as it corrects?

I have not found answers, yet, so I echo Paul’s original concern.

Running Excel seems popular and that suggests that there are analysis functions/features that could be incorporated directly into P123. Besides what’s been shown here, what other kinds of data munging are users doing? Is there a way to offer Excel downloads with the analysis already setup?

Jim, I have nothing against machine learning as long as the (human generated) inputs and instructions to the machine are good. I’m a huge admirer of machine learning when it has been applied to chess. And I think Lopez de Prado is brilliant. People have been trying to use machine learning to solve investment problems for a long time, and if anyone can do it, he’s probably the one, because he really recognizes overfitting. Moreover, too much of what we do in statistics–whether it’s ranking or regression–is linear, and that’s the wrong approach to take with such interrelated and multifaceted data as what we have. I do have a problem with econometrics (as does Lopez de Prado) and my recent comments in this post are examples of that, since the top-bucket-minus-bottom-bucket approach is a basic component of econometrics. K-means clustering is tons of fun, and I could spend days doing it. But you have to use it with the right kind of data, and I’m no longer sure that simple, unadorned industry returns qualifies. My results, which I was proud of for a little while, turned out to be irreproducible if I used different data (Ken French’s rather than P123’s), because so much of the data clumps together, leaving a few outliers. So I’m no longer in favor of using k-means clustering unless the data doesn’t all clump together around a central point. It was a great exercise because it illuminated for me how much clumping actually occurs and where the outliers are. Without it I would have learned far less. But I’m constantly questioning my own results, and I’ve come to the unfortunate conclusion that my clustering approach doesn’t hold water. - Yuval

I am interested in what SP500 would object to. I do not think they want us doing any of this.

Maybe Marc can address this.

Does the SP500 object to downloads of ranks or just raw data?

I also I wonder why there cannot be an internal server that does much of this with just excel on it (no download to us) or Python that accepts an occasional download from another server at P123 but does not download to us.

I do not mean to hijack your thread if this is not on topic.

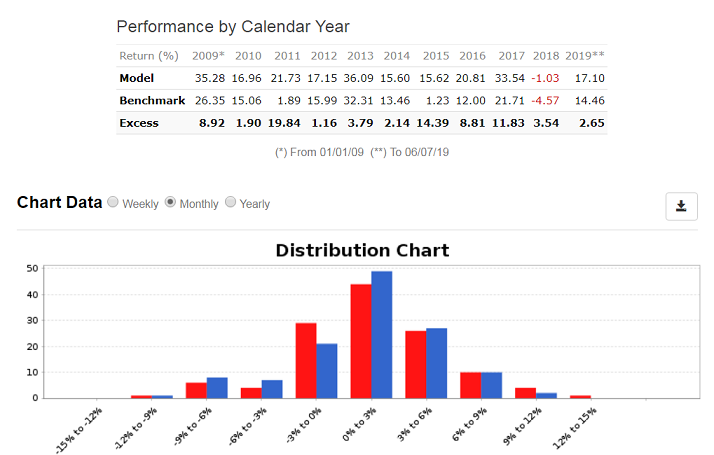

I can’t reproduce your results at all, Bob. Could you please double-check your inputs? Something odd is happening with that performance chart, which doesn’t look the least bit like mine.

[quote]

Yuval: I can’t reproduce your results at all, Bob. Could you please double-check your inputs? Something odd is happening with that performance chart, which doesn’t look the least bit like mine.

[/quote] Here’s my run setup, Yuval. Not shown: All Sectors, Minimum price $3.00, Annualized returns. There is some degradation if NAs Negative is used, but otherwise …?

This is a value factor. But as Yuval has discuss this is also a risk factor.

That is why Piotroski has to have all of the 9 factors to make it work (to reduce the risk). I think people see risk and that is the cause for some of what is going on.

The very top buckets are always depressed for price-to-book even in markets that are not risky.

I am sure there are other or additional reasons that other members will discuss.

Oh, sorry, my mistake. I read 2017 as 2007. Interesting results indeed! And food for thought. It reminds me of what Benjamin Graham wrote about the P/E ratio in Security Analysis, but I don’t have that at hand.

Yeah. Pr2Sales has been a staple of P123 ports for a long time, and was one of the keystone factors in Jim O’Shaughnessy’s What Works on Wall Street, but it’s been an underperformer for about 5 years now and it is seemingly accelerating.

Another option—one that I am included toward—is a decay to zero. I forecast that from 2020 to 2025, the rank-return histograms of price-to-earnings, price-to-sales, and other popular metrics will be essentially flat.

Excess returns come from knowing something that others don’t, having something others don’t, executing better than others, taking risks that others are won’t, or luck. This is an exhaustive list of root causes.

I would be a little hesitant to buy any explanation that has a “this time is different” flavor as it never is. Believing a trend will continue forever is essentially that same thing.

Also, some people pull money out of the market to buy homes, education and retirement.

So who is putting that money into the market for these people? Retail investors that get out at the bottom and essentially leave money they put into the market on the table.

Or so goes some of the theories I have read.

I do not care if you like CNN, Fox, Bloomberg or whatever, they all get paid to make you emotional. It is hyped and one should prepare (in the future) to not get out at the bottom.

We focus on know what stock to buy day-to-day but not getting out at the wrong time may be more important. Maybe we need to keep more cash or whatever helps us do the right thing.

But now, hmmmm. It FEELS different so I’m not so sure.

Common value factors are a lot more accessible than they used to be, but so are growth and quality factors. Why has value in particular been arb’ed out? You would think If anything would have been arb’ed out would be growth factors as people have been relentlessly piling into FANG stocks and QQQ for a decade.

This is why it’s so important to see factors as working together rather than as self-contained ideas.

It can never be said that a low P/E is preferable to a high P/E any more than one could say a low-end Kia is superior to a high-end Mercedes. What you pay is sensible or not relative to what you get. In stocks, the sensibility of a P/E is measured by 1/(R-G) where R is required rate of return (influenced by, among other things, business risk) and the expected future growth rate. For details, see the strategy design course.

Value cannot produce good investment returns if investors are always correct in addressing the relationship between P/E and 1/(R-G). When studies have shown that low P/E has worked over the long term, they should be interpreted to mean that over the long term, the investment community has not been effective in evaluating that relationship. Indeed, various studies have shown that the Street has a tendency to go overboard in assuming the future will resemble the past. Good growth is assumed to persist to a much higher degree than is warranted. Vice versa on the low end. Value investors make their money when reality rears its ugly head and shows investors that they were not really so wise to assume business trends would support the high P/Es they accepted for the high fliers and that they shouldn’t have been so quick to dismiss many of the market’s lesser lights.

So in truth, when you hear or read that value has worked over the long term, you should mentally translated that to read over the long term, investors have not been successful in aligning expectations to the reality that eventually unfolds. This is the condition that’s need to make value work.

What’s odd about the present is that trends (good ones for the most part) have persisted for a very long time. Really long. That means that buoyant expectations that support high P/Es have, expect in some instances here and there, not been disappointed or frustrated. Unless and until that happens, value has no room to work. If human investment community expectations continue pan out (in fact or via stories that are accepted), then value will continue to be starved of the oxygen it needs. If, on the other hand, the world develops such that investors start to lose faith in the high fliers, value will again be the place to be.

Don’t buy into rhetoric about things being arb’ed out. The most important thing . . . Not stopping at WHAT does and doesn’t work but going beyond and understanding and strategizing based on WHY things work or don’t work . . . .is probably at least a generation if not more, from coming close to being arb’ed out.

To Marc’s comment (as I interpret it) about ‘value’ operating in the space between what everyone (ie, the Market) thinks about a stock’s fair value and what a small number (or one person, ie, an analyst or a P123 user) thinks they know about that value; I wonder what the effect that Regulation Fair Disclosure (Reg FD) as well as the ubiquity of company information on the internet has had on closing this gap. Has the gap permanently disappeared (at least for larger companies)?

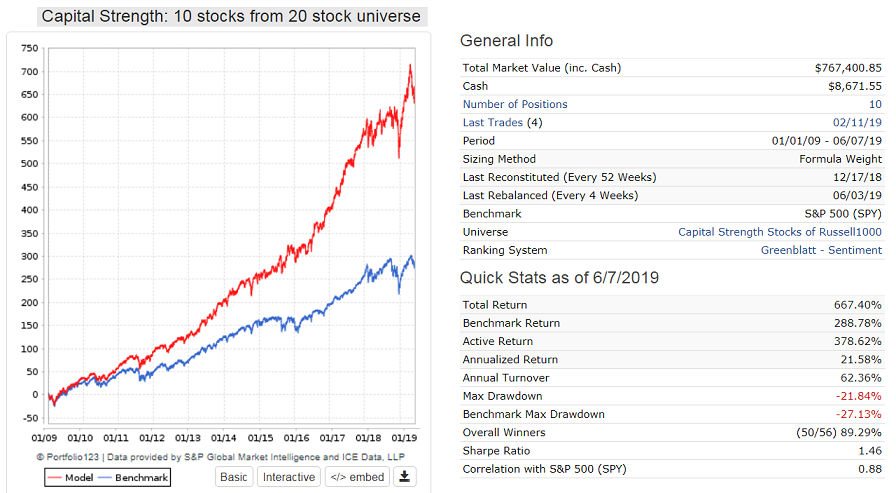

Value seems to have plenty of room to work and lots of oxygen. I am using a Capital Strength Universe. The stocks come from the Russell 1000 Index and must:

have a minimum three-month average daily dollar Trading Volume of $10-million;

have a Cost of Capital less than the Return on Capital;

after meeting criteria 1 and 2, be in the top 500 securities by Market Capitalization;

have at least $1-billion in Cash or $1.1-billion of Short Term Investments;

have a Long Term Debt to Market-Cap ratio less than 30%;

have a Return on Equity greater than 15%;

have a compound annual growth rate of Earnings per Share over the last 3 years greater than 2.5%;

and have a Short Interest Ratio of 9 days or less.

The universe is then reduced to 20 stocks by sorting eligible companies according to the Sales percent change (recent Quarter vs Quarter 1 year ago), and Average Dividend Yield over the last 60 months.

Perhaps this is not the accepted definition of value stocks. But selecting 10 of them and reconstituting every 52 weeks, no buy or sell rules, just 1 as a sell rule, out-performs SPY every year over the upmarket period to 2019 and produced an annualized return of 21.6%. That’s good enough.

Interesting question, and I’m not sure the world is ready to answer it. It’s tempting to suggest that Reg FD has contributed to Mr. Market being a lot smarter than way back when Ben Graham invented him. But even beyond Reg FD, we have the overall information explosion.

But before locking in on a conclusion, I’d want to see how things look when the business cycle gets off the long trend it’s been on. It’s a lot easier for a lot more people to be right when things stay on trend for a prolonged period — people who go overboard extrapolating the past get away with it (and even get rewarded) for a longer period of time.

The more poignant question is more for economists than investors: Why have trends lengthened and are the factors likely to be sustainable? If we knew the answer to that, a lot of other issues about which we wonder would fall into place, at least somewhat.