Although I am defending small value, (or at least my version of it), I am not yet pounding the table in favor of small value right now. I do know that it will bounce back one day. I just don’t know exactly when.

My best guess is that small value will bounce the highest off the bottom of this bear market. I don’t know if the outperformance will continue after that after the first nine months to three years. But the longer LG outperforms, the more SV will excel when it gets it’s turn in the sun again.

Here is my simple explanation on the subject. It is based on a presentation by John Templeton to a group of us in the early 1990s. Someone asked him what was his strategy. He said it is very simple, the way I got rich was to wait for a recession and then buy every stock under $1 a share. Repeat! When he was most active he said recessions came routinely every four and a half years. I modified his strategy a bit and have used it ever since with amazing success. (Interestingly, this matches some of the conclusions from that article on crisis investing.)

That brings us to the present times. Why have small caps stocks underperformed for a long time? Reason #1) We rarely have recessions anymore! The Fed has tried its best to eliminate them. Reason #2 (a natural outcome of #1): Now, during even the slightest economic softness, the Fed’s policy of zero interest rates and mass stimulation has created zombie (mostly small cap) companies. So, in past recessions, if you had a cheap small company you knew that it was at least a decent company–for it was surviving the recession! (Recessions were a natural cleansing of bad companies–the forest fire analogy.) Now, there are a lot of crappy companies that should have gone bankrupt long ago.

Still, in my opinion, this current recession offers small cap opportunities–but I have modified my base-case strategy (because of reason #2).

I have been thinking a lot about what is being debated in this post. My historical beliefs align with what Chaim and Chipper are saying. However, I now believe that the market has structurally changed. I am an Economics major and years ago we learnt about economies of scale and diminishing returns which basically talks about how a company like Ford can become more efficient as they grow larger and spread the fixed costs over increased sales up until a point when the firm becomes too large to manage and they start to realize diminishing returns as the firm expands and has to continually invest more capital to grow the business. Compare that to nowadays with Fang stocks that are fundamentally different. The largest corporations today all benefit from network effects. The marginal cost of Microsoft selling another office 365 product is basically zero. Same for Facebook every new customer they gain is basically at a zero incremental cost. Now add a few more million customers online every year and you start to realize how the global behemoths are kicking the small caps asses. The small cap innovators of today have to pay Google if they want to advertise or give Amazon a cut of their profits if they want to grow their business. Its a totally different cost structure that I never learned about in University. While I do think small caps will have their day I don’t think it is today or tomorrow.

Some of the Nifty Fifty were similar. For example, what’s the incremental cost to Coca Cola of selling more syrup? Very low. So, Coca Cola was a FAANG type stock back in the day. It was selling at a very high PE. It eventually grew into that PE, but not before it’s price crashed. If history will rhyme, I wouldn’t be surprised if these huge companies hold up the longest throughout this crash, but eventually crash along with everything else. Then, coming out of the bottom, I expect small value to lead for at least the first 9 months to 3 years. After that we shall see.

David,

Thanks for the article. I have alluded to the problem quite a bit back when people were still thinking that this was a normal market correction and hoping for a V shaped recovery. BTW, most small stocks that were profitable before the shutdown will recover. They are not doing as good as the FAANG stocks but are in much better than the corner barber. OTOH, many small stocks which were not profitable during the good times will be forced to close their doors. Others, especially those which will be shutdown for more than a few months (e.g. travel, entertainment, restaurant, oil) will have a much more difficult time recovering. Cyclical stocks may also be affected more than the typical recession.

At this point, investors have again forgotten the hard earned lessons from the 1920's, 1960's, 1980's Japan, and 1990's; price ultimately matters. Stocks will revert to track earnings. So everyone "knows" that there is no point in owning small value stocks. Proof? The past ten years. FAANG and tech stocks are the place to be. The current attitude is: What is discounted cash flow? Is that something like the failed modern portfolio theory? Hasn't the recent past dis-proven DCF?

And:

2021 Update: Small cap value (top 300 cheapest Russell 2000 stocks as ranked by “Core: Value”) has been up by 151% vs 56% for the Nasdaq 100 (large growth proxy) since that was written. At this point small value is still cheaper than large growth but not by as much. Price has rocketed up and what would have taken years during regular markets took a year (perhaps because of all the stimulus money).

Valuations matter. What’s cheap now? Many international stocks. While we don’t have data for individual international stocks (except Canada), I would love to be able to backtest international ETFs based on Market Cap/GDP and other value measures.

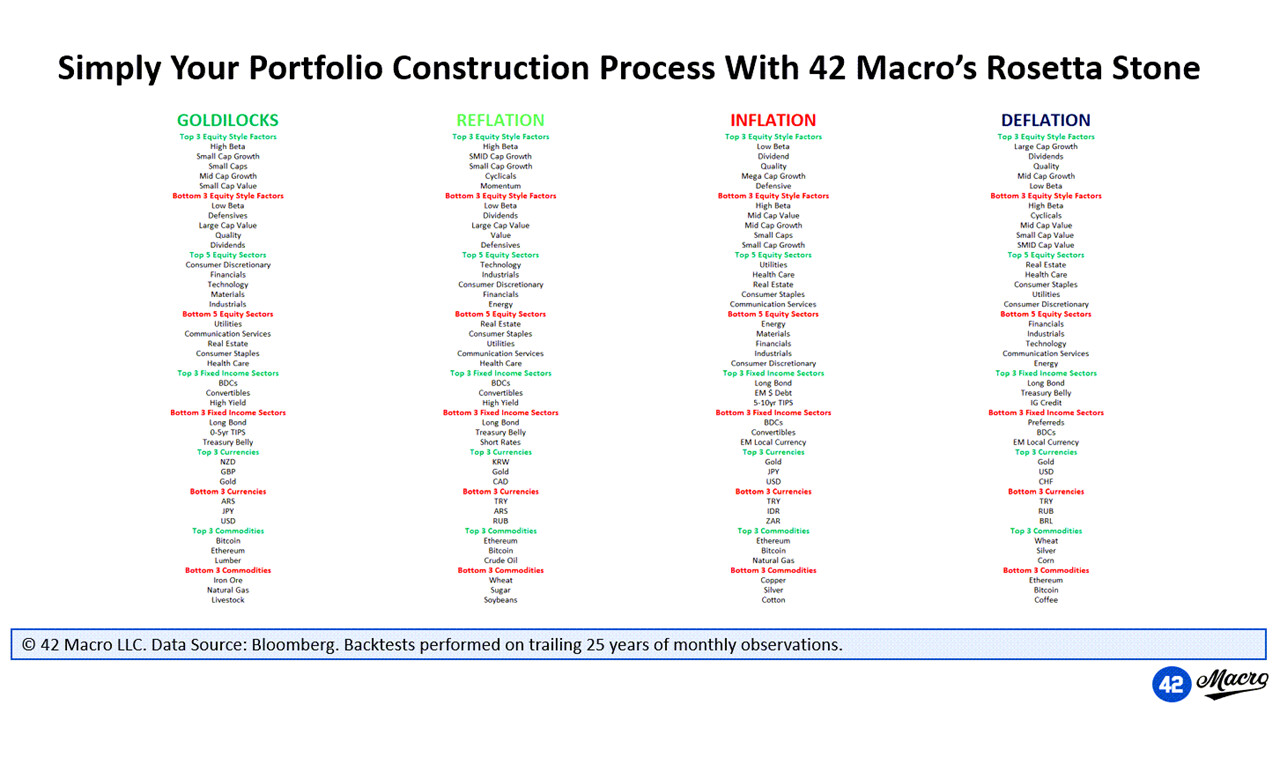

Regime 1 Goldilocks: ROC GDP up, ROC Inflation Down

Regime 2 Reflation: both up

Regime 3 Inflation: only ROC Inflation up

Regime 4 Deflation: both down.

Random Thoughts:

The only comparison that makes sense is to compare a big cap with a small cap with kind of the same fundamentals, factors (growth momentum, industry momentum, value etc.)

Small caps and value stocks as a group have underperformed b.c. they had worse factors then Google and Co.

There is just too much junk in the russel 2000 to be able to keep up. (Reason behind that, huge scalability and network effects of google and co, which are basically monopolies).

Also:

The small cap effect is not really an effect, it is driven mostly by low volumne (e.g. small cap stocks with relative high volumne is the worst place to be long)

I am buying small caps with low volumne b.c. one can find small caps with great fundamentals / factors that are not buyable for the huge institutions (because of size) and playing a structual competetive advantage of a portfolio sub 1-3 Mill. That is a structural edge that can not go away as long as I can find stocks with low volume that have great factors.

So I do not care about the russel 2000 b.c. I do not buy a typical russel 2000 Stock: my stocks have less volume then a russel 2000 stock and better fundamentals / factors…

So I designed a book of strats that perform well in regime 1-3 and try to time regime 4.

Factors I use: Momentum, Low volatility, Industry Momentum, Value, Quality, low volume + everything through a lense of Rate of Change (e.g. improving ranks!) especially when it comes to earning estimates.

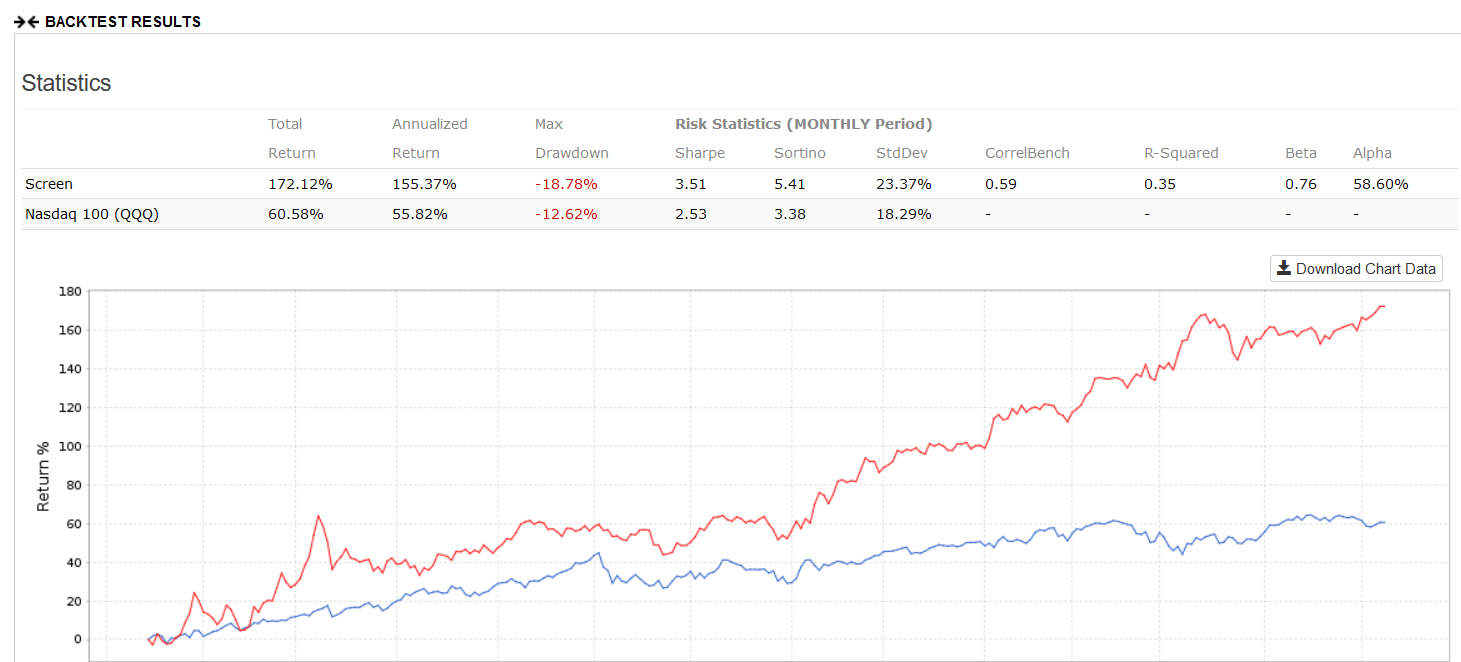

When this thread was started, a lot of people were ready to abandon small value in favor of large growth. But guess what? Valuation matters. Here is the chart.

Although not purely a value play, the ETF “RWJ” has produced a similar overall return over the same time frame (about 170%). A lot simpler to invest in. I have had some money in it for about 6 months now.

This is not my strength so just a quick question: At least in retrospect, doesn’t Marc give a good reason as to why growth stocks have been underperforming with the Dividend Discount Model (DDM)? Growth underperforming and value doing better?

Even if one believes Tesla’s story on growth haven’t those future (expected) revenues been discounted more in the recent environment of inflation and rising interest rates?

Obviously, any expansion or corrections from Marc (or anyone else who truly understand this) welcome.

Changes in inflation affect different types of companies differently. Warren Buffett wrote about this years ago (late 1970’s early 1980’s?). Commodity companies (and other value stocks) don’t necessarily benefit if costs go up as fast as revenues, while strong moat companies (a category which overlaps large growth) simply raise prices with inflation an continue making a high ROI.

However, people overestimate the correlation between earnings growth and stock prices while they underestimate the correlation between valuation and stock prices. You can see this very clearly when backtesting growth vs value.

Over the long term people often overestimate the discounted cash flow of growth companies vs the discounted cash flow of value companies. This is a bias that we take advantage of. An exception was the period from when the dot com bubble burst (in 2000) through 2013 when people actually underestimated future earnings growth of big tech in particular and large growth in general. It’s human nature for generals to favor strategies that worked in the last war.

I think this is absolutely right. I was even going to post about this. But I would have probably said something about regression-toward-the-mean (for earnings) which would have gone off into the statistical weeds, as I often do. Plus, I think people confuse mean-reversion and regression-toward-the-mean. I doubt that people are interested in the distinction (which is important if one is going to look at it that way).

“Over the long term people often overestimate the discounted cash flow of growth companies…” sums it up quite nicely, I think.

Maybe this is a subject for a different thread, but I’m wondering how you deal with this when looking at discounted cash flows since you have to plug in some sort of growth estimate for every company that you do discounted cash flow analysis of.

Here’s my conundrum. I believe that DCF analysis is probably the best way to arrive at a company’s intrinsic value. DCF analysis depends a good deal on what growth number you plug in. Every study I’ve done shows that growth and performance have a hill-shaped relationship: middling growth performs better than high or low growth. This means that DCF analysis will often arrive at results that are inferior to comparative value measures that don’t take growth into account (especially p/e and unlevered free cash flow to enterprise value). I can’t really conceive of a DCF analysis technique that will result in a high-growth company being assigned a lower intrinsic value than a comparable middling-growth company, but that’s what I believe is called for. Either that or one could assign all companies the same growth numbers . . .

And to get back to your quote, is there really a difference between the discounted cash flow of growth and value companies since DCF takes both growth and value into account (unlike, say, P/E)?

I do not have to tell you that I am not the best source on this. I look forward to Chaim, Marc and others commenting on this.

But FWIW. I find the usual DDM formula confusing or even misleading in this context.

My simple-math mind is not fond of: P = D(0)/(r-g).

You already know that P is the price of the stock, D(0) is the dividend for the first year, r = constant cost of equity capital and g = constant growth rate into perpetuity.

So first, I like some of the discounted cash flow models better but sticking with the DDM the expanded version is MUCH MORE INTUITIVE FOR ME. Just me personally, probably.

So like this, I intuitively understand why growth is discounted more under certain market conditions:

P = D(0)/(1+r) + D(1)/(1+r)^2 + D(2)/(1+r)^3 …… D(n)/(1+r)^n

This is intuitive to me. No matter how you arrive at r, when it is increased the value of future dividends will be decreased EXPONENTIALLY. My simple-math mind gets this.

Gets it without really caring how growth is calculated. I do not have to even worry about r so much—I just have to think it is probably increasing.

Many people understand this better than I do. And this is just a preference for me, personally.

Again, just FWIW. But if r is increasing (for whatever reason) future dividends mean less and I can see it this way on an intuitive level.

Although value investors believe that price tracks intrinsic value…eventually…and that intrinsic value is DCF, I don’t recall a single value investor who uses true DCF successfully.

That’s because estimating DCF is too imprecise.

Rather, successful value investors use either (a) statistical techniques (ex: buying a basket of low PE or other value yardstick), or (b) try to estimate earnings over the next few years using past results, growth, and ROI of retained earnings, and slap an estimated PE on it in year three (this worked well for me and worked even better for others such as the Oceanstone mutual fund) or (c) look at the really long term expected ROE combined with todays PE multiple, a technique used by Warren Buffett.

You found that average past earnings growth is correlated with better future returns than extreme growth (or shrinkage). But how does past earnings growth correlate with future earnings growth? That is a different question. Did you ever study this?

I notice you use DCF and not DDM. There are 2 obviously good things about this in my mind.

First, usually when they use DCF they only try to go out about 5 years on their estimates of growth and make no claim to be able to estimate growth “into perpetuity.” Still 5 years is a heavy lift but literally infinitely better than the DDM assumptions.

Second, they usually separate out the cash flow calculations for each of the 5 years (no constants for growth). Certainly, I have problems when making any estimate of continuous growth. In fact, there is no such thing as constant continuous growth.

Will Tesla have continuous growth that can be put into one constant? Not a chance!!!

Once the cash flows (or dividends) are separated out, then the formula may be accurate: depending on the accuracy of one’s estimates over the next few years (for DCF). But I think I am guaranteed to be wrong if I am assuming continuous growth and trying to find a constant for this.

So using the expanded DDM or discounted cash flow formulas really is better I think. It’s not just more intuitive.

I don’t see a point in using DDM, unless it’s a stock in liquidation and the value is in the dividends. Nor do I know too many analysts who use DDM successfully. DCF is what Warren Buffett considers the true intrinsic value of a stock.

I did, three years ago. I wrote then, “I found that measurements of past earnings growth were relatively useless for predicting future earnings growth. In fact, there tends to be a reversion to the mean. The stocks whose earnings per share have grown the most over the last twelve months are less likely to exhibit strong growth over the next twelve months than a random selection. But there was one exception: operating income growth, as measured by the most recent quarter. And indeed, if you look at Seeking Alpha’s articles on individual stocks, they very often use precisely this comparison.”

Just a side-point that may tie what you and Chaim have said together. Chaim said this I think:

And your link suggest that EBIT may be useful. I did not read your link in detail and I probably missed a few things. Or could be simply incorrect in what I think I read.

But DCF, unlike DDF, uses terminal value in its calculations, I think. As near as I can tell, there are multiple ways to calculate terminal value. But some will use EBITDA/EV for this or perhaps EBIT/EV at times.

If I had a question (to which I do not have a clear answer) it would be: are you finding EBIT useful because it is related to earnings growth, terminal value or both?

I do not think the two are mutually exclusive as earnings growth will affect the terminal value. But I think the terminal value using EBIT or EBITDA could be the most direct link to a formal calculation of a company’s “intrinsic value” (or the price price target) and why you find it holds up well in your analysis. People like Marc and Chaim may also be looking at this in their calculations. And buying when you do (driving up the price when you all agree).

And again, while my to-do list has me buying some textbooks on DCF (and reading them) I have not gotten too far on this. I defer to you, Chaim, Marc and others on most of the details of the best practices in calculating DCF.