I have been using weekly returns under "statistics" now for a while to some additional calculations that I use for books. There seems to be some issue with how this is calculated, or it does not reflect the "week". I will use one of my strategies to show, by example, the problem.

Note: this is a simulated strategy, but I have it also live. Please note that this is NOT related to PIT or live vs. simulated differences.

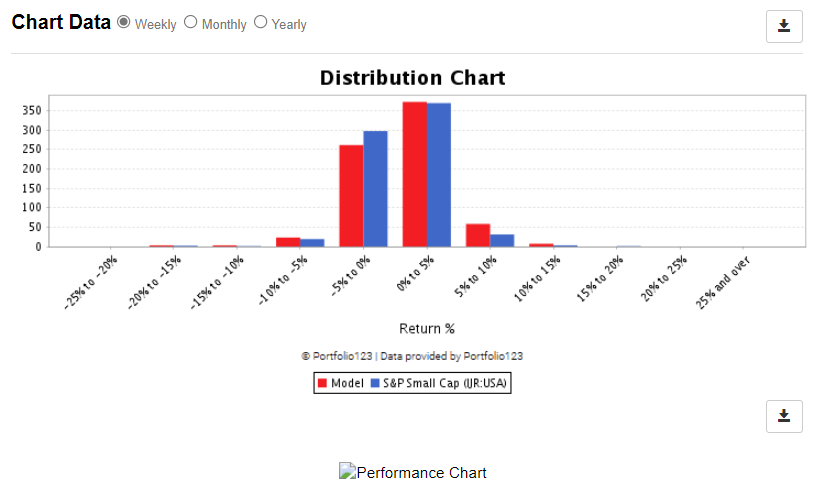

First here is a screenshot of the statistics page which, by default, always shows monthly:

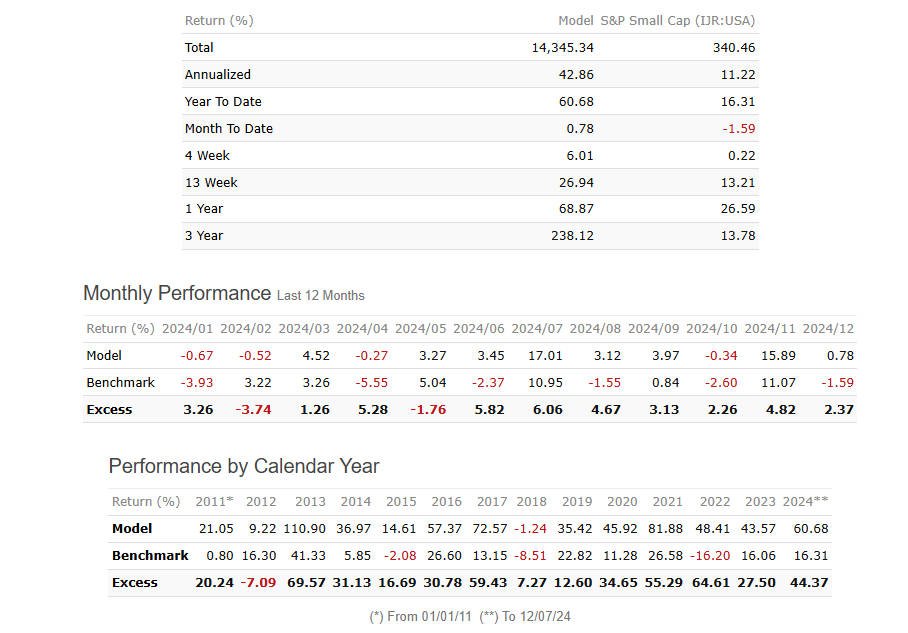

As can be seen by the return for December, the strategy returned 0.78%. Also, because the monthly, weekly boundaries align for this month, the "month to date" also shows 0.78% .

If I go to the strategy overview page and select the performance tab:

Again, 1 week return shows 0.78%. The three reported returns are consistent and is also correct (as per my live port which I track separately as I want daily data).

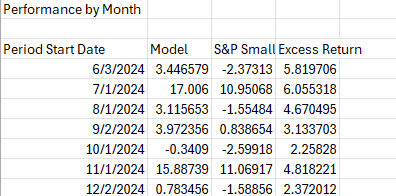

Back to the statistics page. On Chart data section, I have the option of weekly, monthly (default) and Yearly. If I the download button on the chart of "Monthly returns since XX/XX/XXXX", I can get the return per period since the start date. With the monthly option selected, I get:

Note: for the purposes of this email, I have only shown the last few rows.

Again, unsurprisingly, the return for the month commencing 12/2/24 is 0.78346. The monthly returns also all aligns with the monthly performance (last 12 months). So up to this point, everything is correct and consistent.

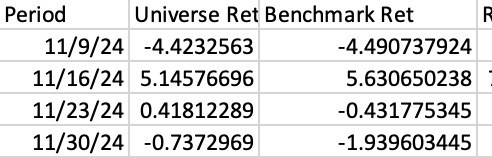

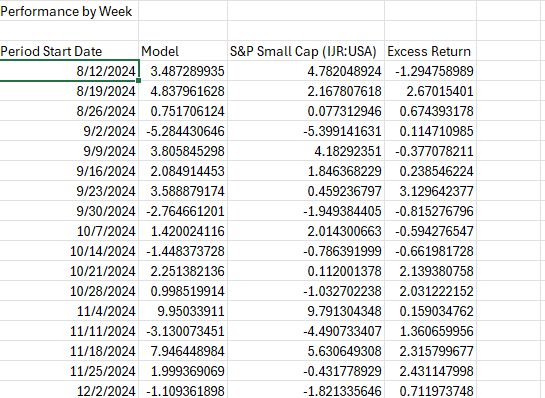

Switching the Chart data to weekly return, and downloading "Weekly returns since XX/XX/XXXX":

Now, things get strange. The weekly return for the week of 12/2/24 shows a loss -1.109361898. I KNOW this is wrong, because as I said I have verified using four different approaches that the return was 0.78%.. But this isn't where is ends. If I use this data to calculate the 4 week return, it is different from the 4 week on the statistics page. The strategy shows a 4 week return of 6.01%. The downloaded weekly data shows a return of 5.4751. The 13 week, 26 week are also wrong/different.

Can someone take a look at this and advise.

Thanks,

Simon