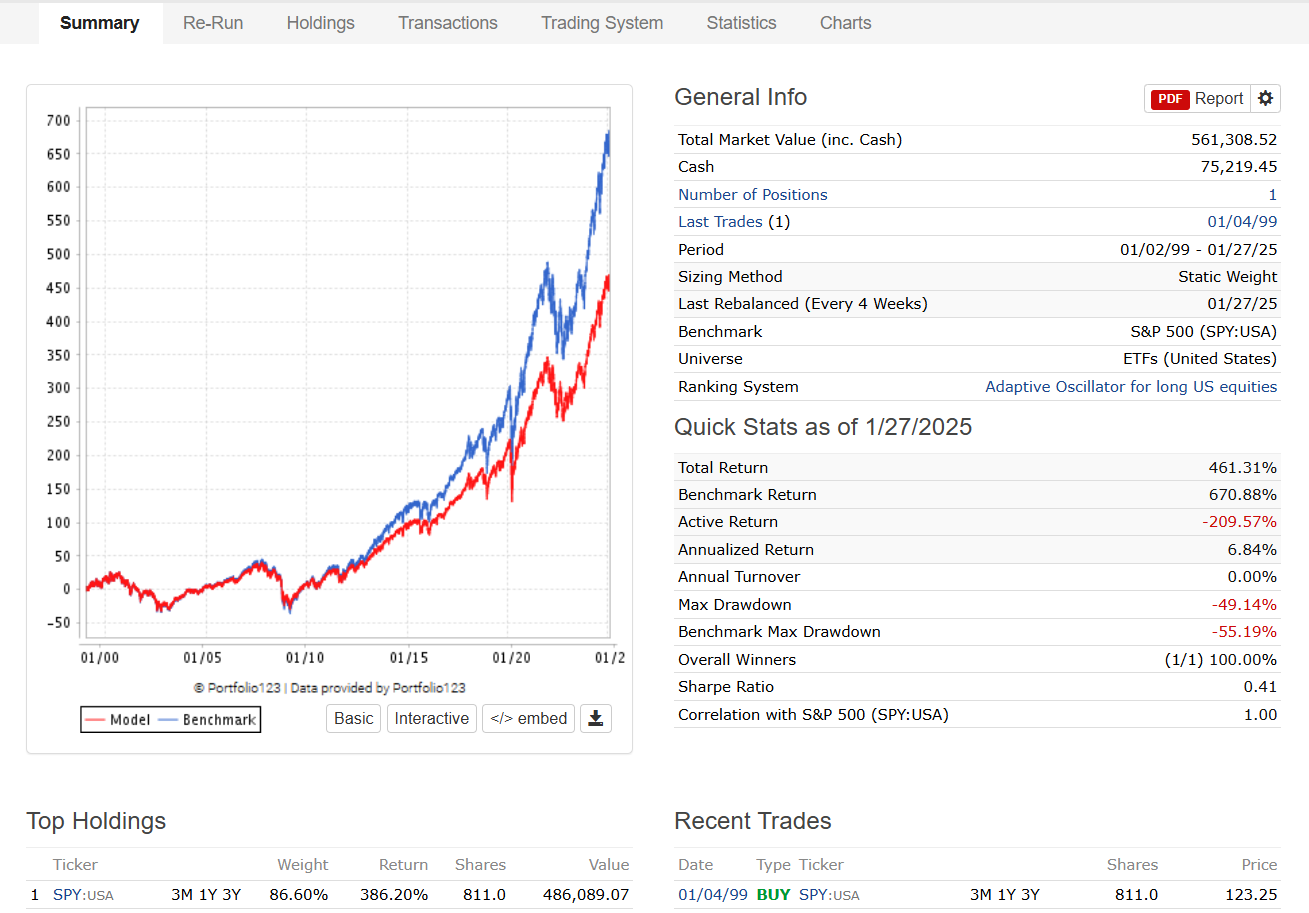

Having started to test some market timing/heding approach, I've (accidentally) noticed that a strategy that simply holds 100% of SPY produces a backtest with results significantly different from the benchmark which is also set to SPY (see the image below) - what could be the reason? Price adjustments for dividends? The numbers don't seem to be aligned...

Hi Romanmom,

I see you are holding 86.6% SPY on the last day. Could it be that you are holding a part of your capital in cash during the years of the simulation?

Best,

Victor

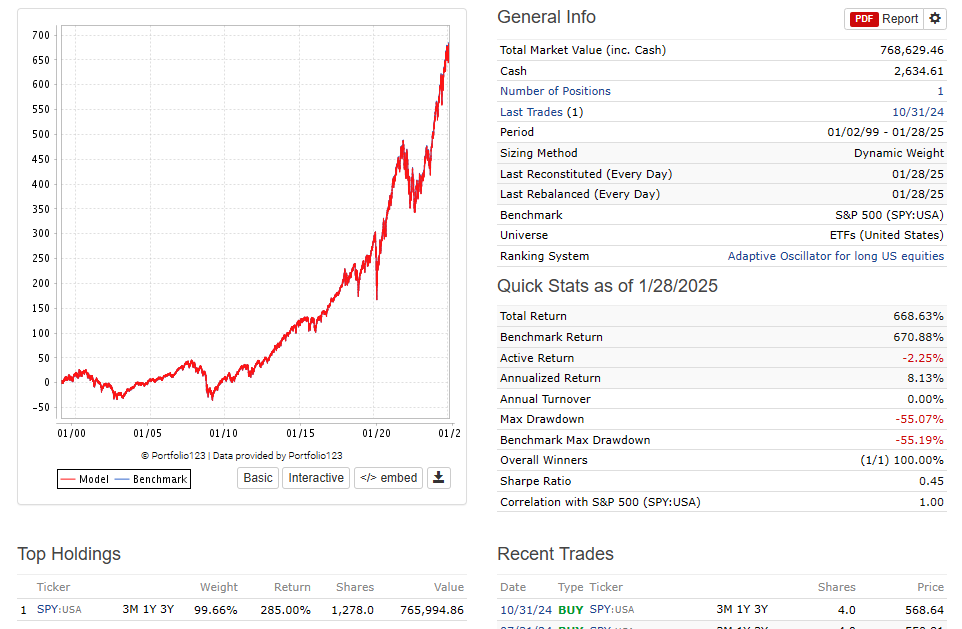

Yes, the difference is that you have your rebalance rules set too loose. I use the 'dynamic weight' feature, set to equal weight where it makes sure the portfolio is tracking very tightly. So every now and then it will add a few shares of SPY. Tracking is very close although off by a tiny amount due to holding small amounts of cash in between rebalance points.

1 Like