The paper from Matthias X. Hanauer proposed SUSIR metric.

Conceptually, the formula calculates how far the current short interest has deviated from its 12-month average (the numerator) and then scales this deviation by its historical stability (the denominator). A large deviation from a historically very stable level of short interest results in a large SUSIR value, signaling a significant "surprise." Simply: the zscore of most recent value vs. previous PIT values.

SUSIR = (SIRatio - LoopAvg(FHist("SIRatio", CTR), 12, 1, 4)) / LoopStdDev(FHist("SIRatio", CTR), 12, 1, 4)

Alternatively: FHistZScore(SIRatio, 26, 2)

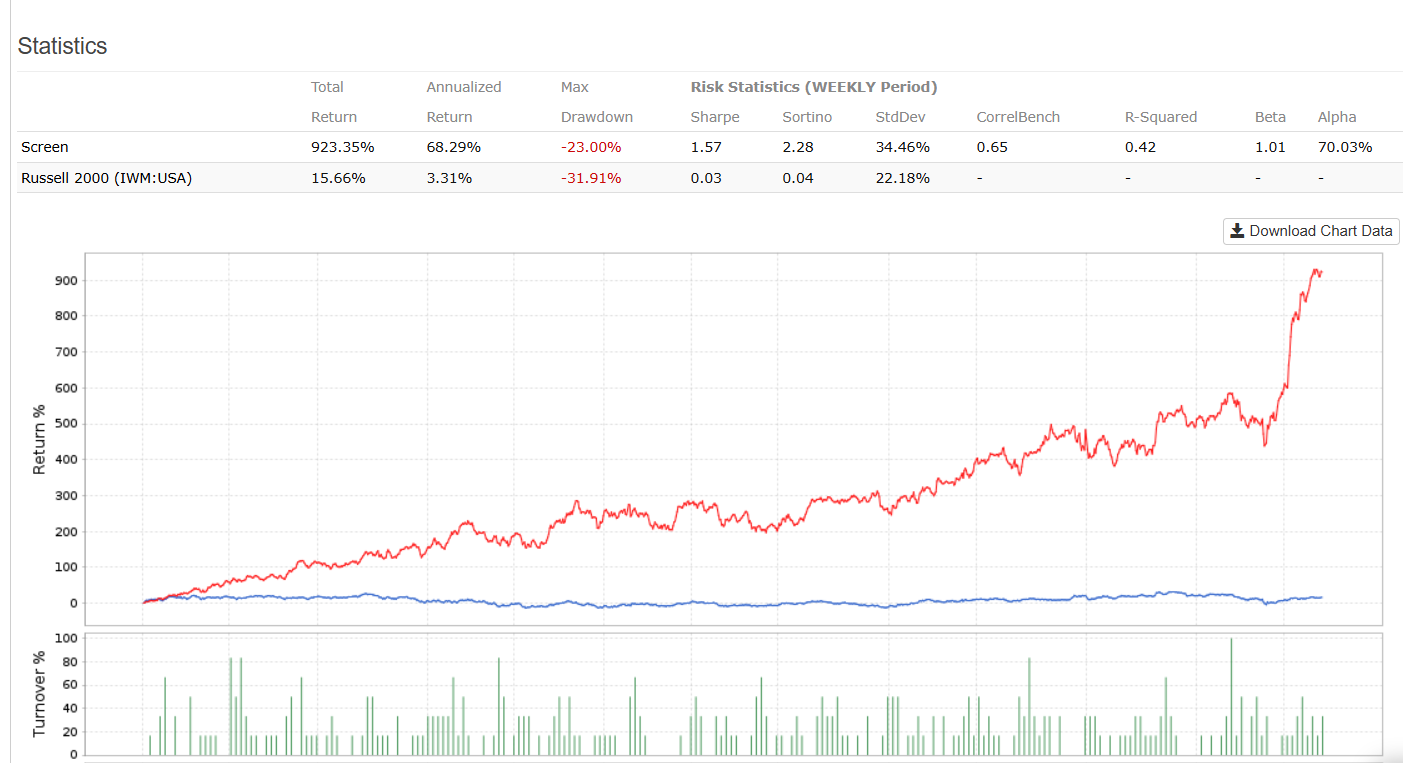

The performance seems to be encouraging:

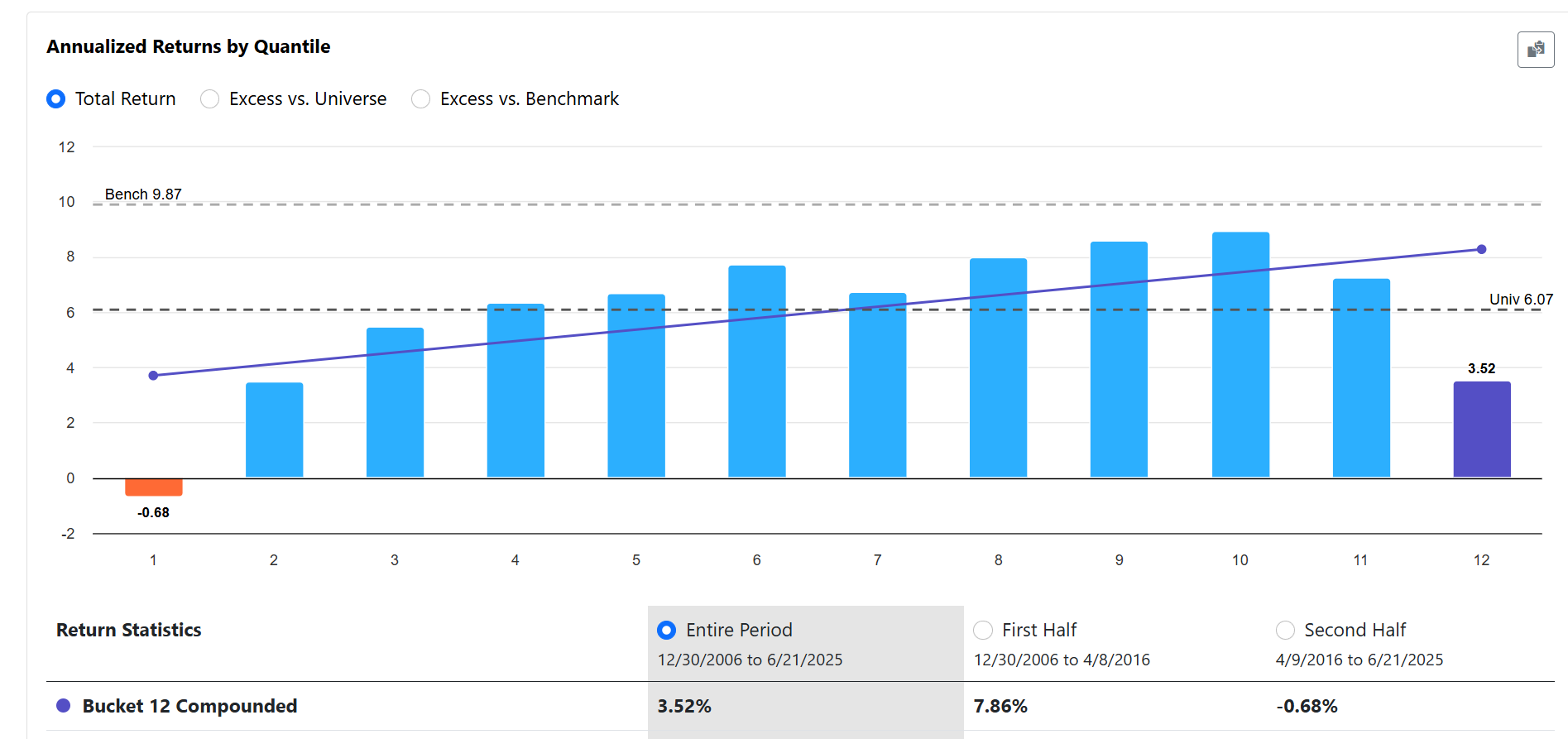

SUSIR, lower is better, Easy to Trade US

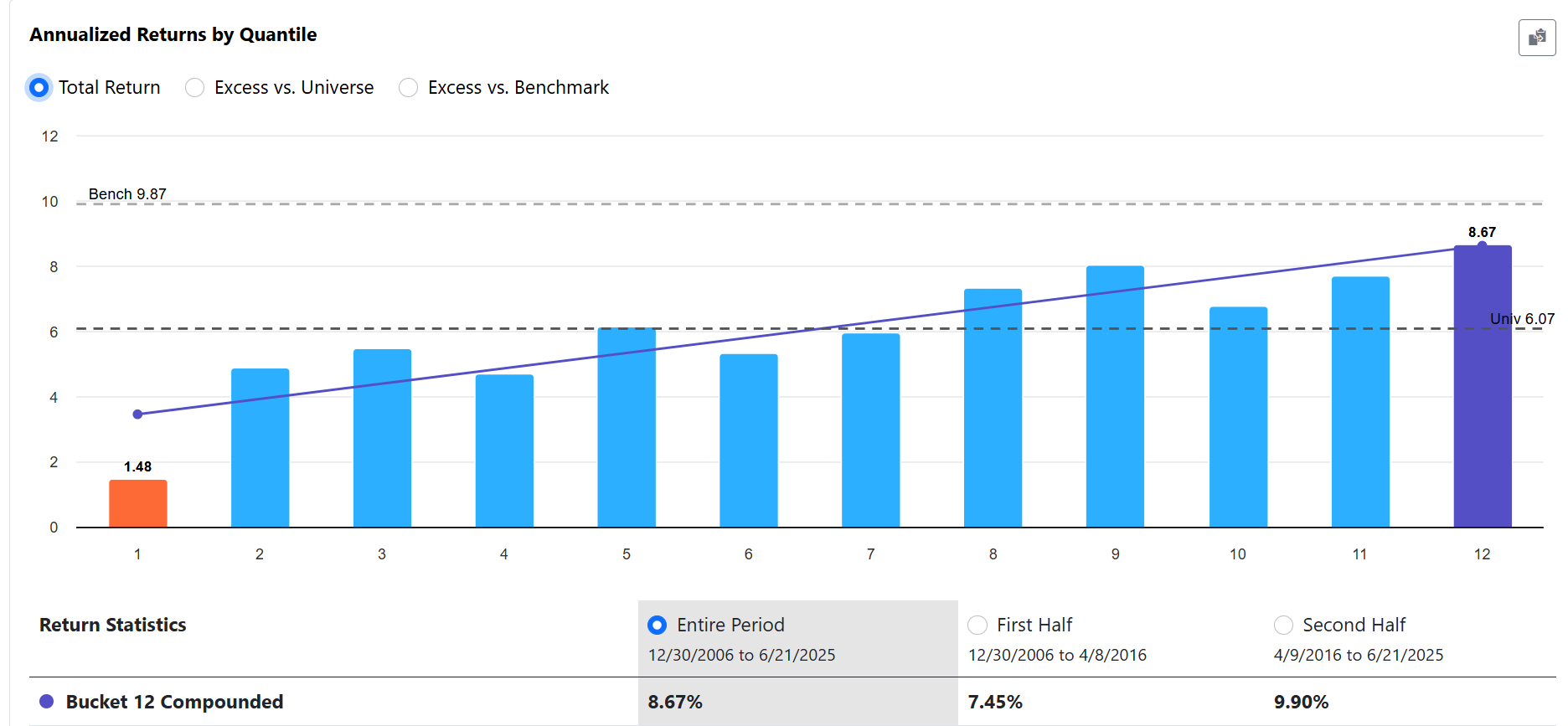

SiRatio, lower is better, Easy to Trade US

Surprise in Short Interest by Matthias X. Hanauer, Pavel Lesnevski, Esad Smajlbegovic :: SSRN

edit: Due to formatting issues, the formula is not displayed correctly. Please edit it by adding a backtick before FHist and after CTR) to make it work.