I wanted to empirically test Ray Dalio’s often-quoted claim that portfolios should hold at least 15% gold, rather than just repeat it as conventional wisdom.

Reduce drawdown and tail riskwithout materially sacrificing long-term returns.

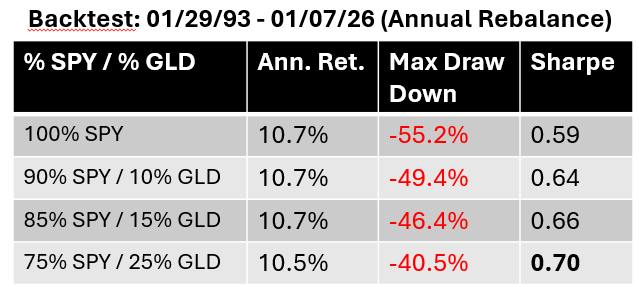

Key Results

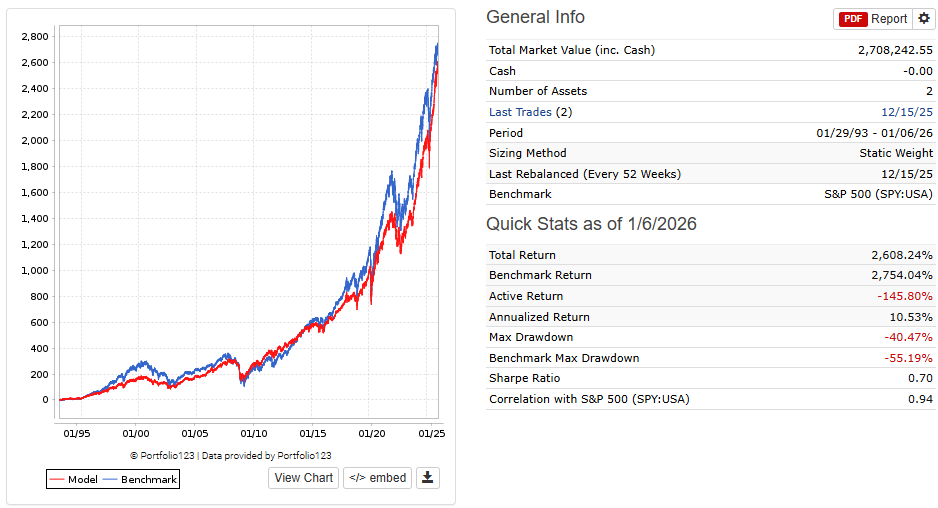

Baseline (SPY only):

Annualized return: ~10.7%

Sharpe: 0.59

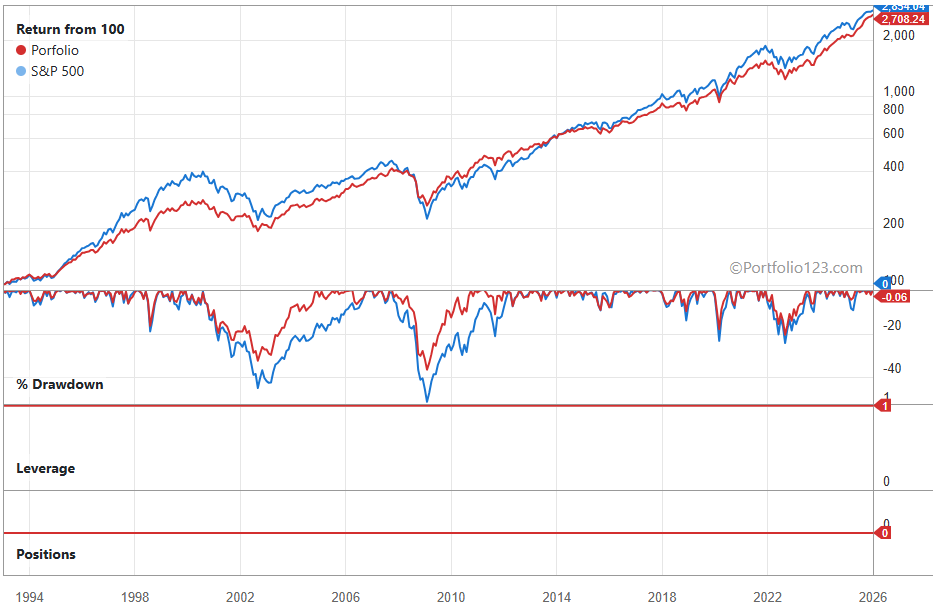

Max drawdown: -55%

Adding gold:

Sharpe increases monotonically as gold weight rises

Max drawdown improves materially once gold ≥ ~15%

CAGR stays remarkably stable even up to 25% gold

Notable points

<10% gold → modest impact only

15–20% gold → meaningful drawdown reduction with no return penalty

25% gold → best Sharpe and largest drawdown improvement (~-40%) with only a small CAGR trade-off

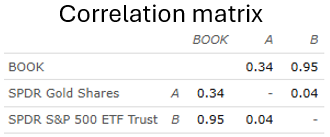

In other words, gold acted as both a diversifier and a return contributor, unlike bonds which typically reduce volatility but drag returns.

My takeaway

Dalio is indeed right: gold needs to be double-digit sized to matter

15% looks like a minimum effective dose

20–25% appears statistically superior if the goal is drawdown and risk-adjusted performance

This does not mean gold will always outperform, but its low correlation + positive long-term return combination is unusually powerful in portfolio construction.

It is funny. 25% gold is my sweet spot for my financial portfolio. For determining allocations at portfolio level I used this free website: https://portfoliocharts.com/. Gold, no miner as different behavior and I see it more like an insurance.

To me, the real lesson isn’t that gold should always be double-digit, but that diversifiers need to be large enough to matter when the regime favors them. We may not know regime shifts in advance, but the real risk isn’t failing to time them perfectly — it’s assuming they don’t happen.

I agree, the Portfolio charts website is a good place to start high level allocation studies. Also, https://www.portfoliovisualizer.com/ provides additional tools to further allocation and performance trades. I hold ~ 15% in GLD.

Around 5-10% in ETF Gold, amonsgst other assets to diversify (bonds ,special situations, biotech,geographic diversification...). Miners are different, Volatility of miners are huge compared with raw gold

I dollar averaged up to ~16% IAU in my core portfolio starting a few years ago, it is now overweight at 25%, after the recent gains, and a partial rebalance. It’s there to stabilize the portfolio returns, and as insurance against dollar debasement.

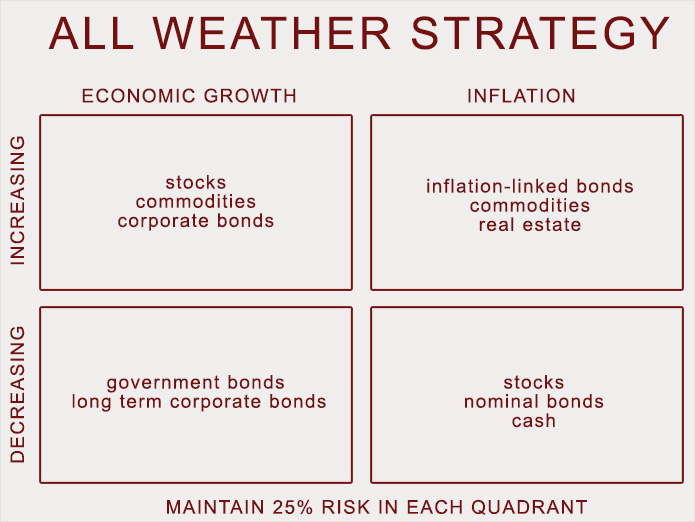

My introduction to Dalio was via his All-Weather (risk-parity) portfolio structure. In that, the general allocation is 30% Stocks (e.g SPY), 40% LT Treasuries, 15% ST Treasuries, 7.5% Gold, and 7.5% Commodities. State Street now offers a fund, which Bridgewater manages, that implements this approach with finer granularity and international exposure. I don't expect returns to be much more than 8%-12%/yr, but the diversifier (geography, currency, investment type) it provides is great for my objectives.

To your question, I started building gold into my portfolio back in 2019 and it's about 10%-12% now.

Yes Dalio typically speaks of the gold % with a (risk free) bond allocation also in mind and not just stocks. Basically, assets that align with different economic change drivers. The bonds need a greater weight given their volatility is generally much lower

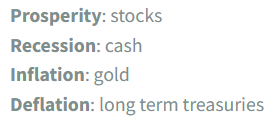

Or Harry Browne’s portfolio which speaks more to me ( Permanent Portfolio – Portfolio Charts ). Even if I am not following it as I ditched bond a few years ago.

You’re probably not alone in ditching bonds a few years ago. Even many well-constructed tactical systems defaulted to bonds as the “risk-off” asset until the regime changed, and a lot of those have since been revised to require momentum or trend confirmation.

Gold, in that context, has often been a better long-term store of real value than cash, particularly across inflationary or currency-stress regimes—but it comes with its own long cycles and periods of frustration.