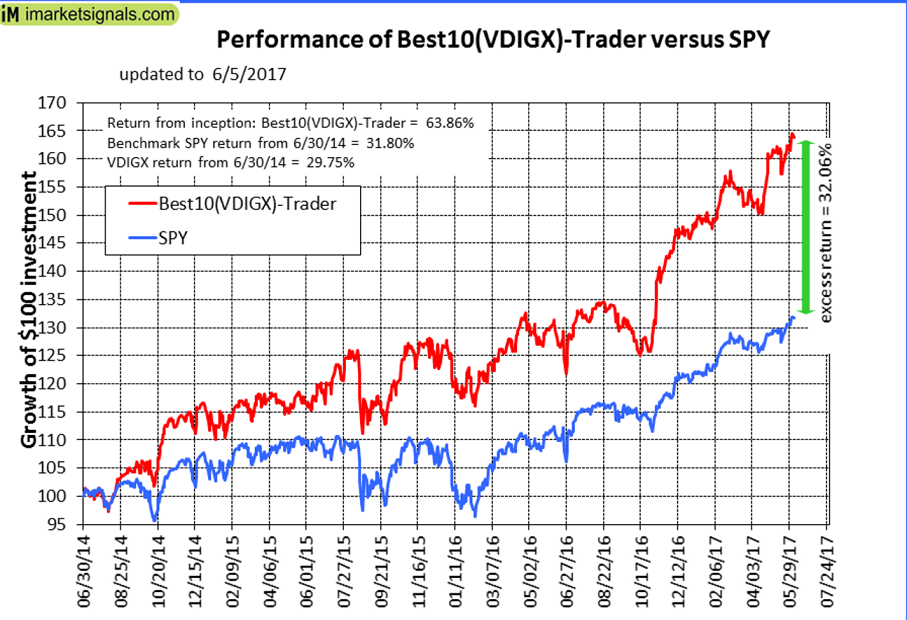

If one makes use of a changing universe from outside P123, one has to run a live portfolio and update the universe periodically. I have similar models using this approach and running for 3 years now. One uses the approx 50 holdings of VDIGX which I feed into the model every 3 months, and then rank them to select the best 10. It has shown double the performance of VDIGX over the last 3 years PIT, but not nearly as good as Walter’s model. I suppose the Value Line selection works better.

Georg, Whether VL is better has yet to be proven, I think. I’m not going to let family/friends invest until I have at least 36 months of out-of-sample date. But the original idea of using an externally derived universe came from your work!

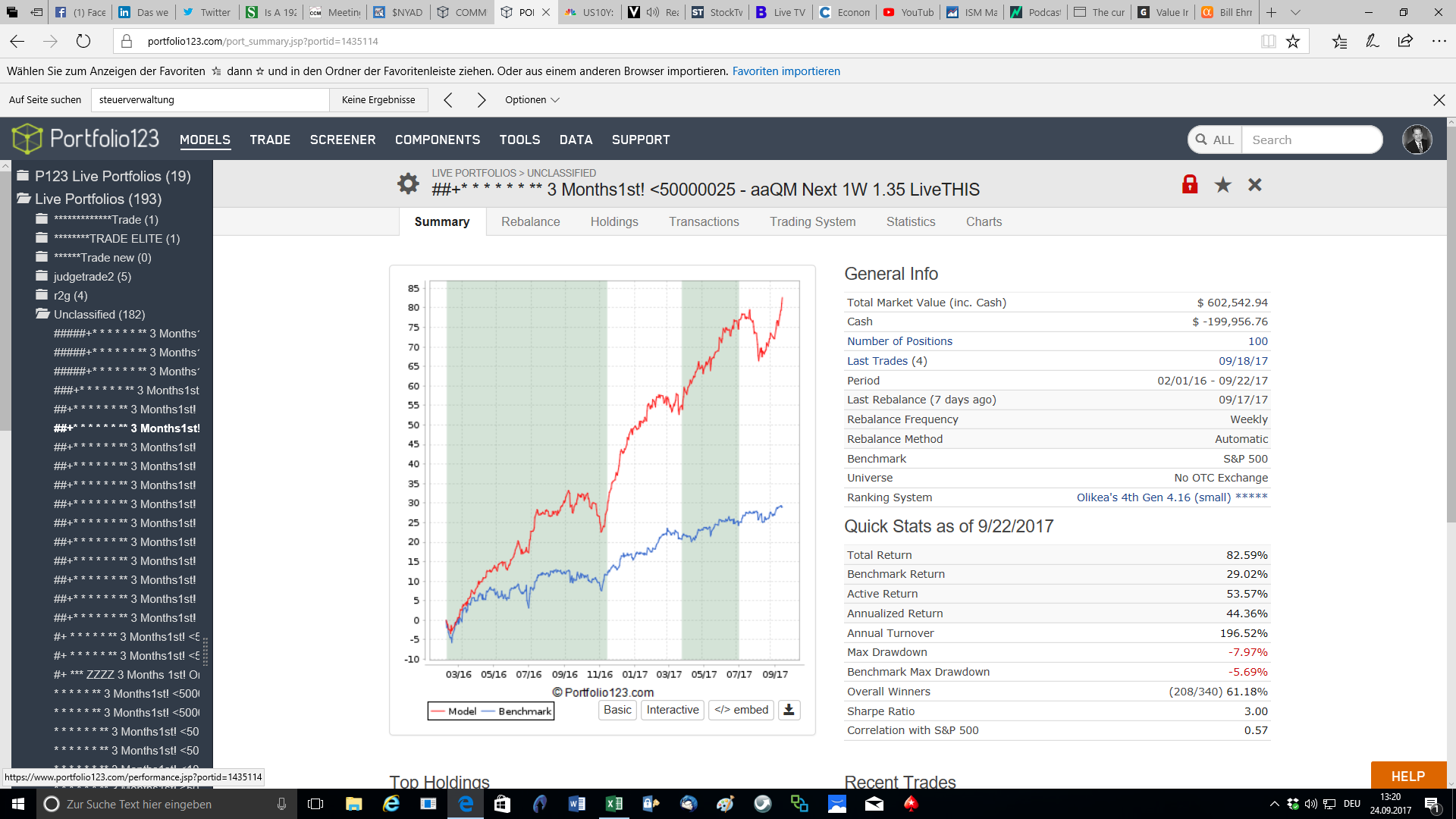

Jim, yes your understanding is correct. I’m updating the active universe with InList in real-time. Every Monday morning I create a new Inlist and manually rebalance. The little secret is that the current port holdings have only one stock in common with the current VL universe. VL holdings are very dynamic.

Best,

Walter

cool

Walter,

Which one of their products do you subscribe to? Feeding a new inlist every week seems like a lot of work to me.

And thank you for the acknowledgement. We, the P123 community should share ideas frequently, like Steve Auger did with his many examples of how to use P123.

Best,

Georg

Georg,

I use VL’s Timeliness rank which is limited to 100 stock selections (max). I’m not sure what the subscription product is called since I access the database online via my local library. I find the the VL product descriptions incomplete and confusing. I don’t why they’re so bad at selling their products.

Best,

Walter

EDIT: It is a bit work to download the stock list each week. Maybe 15 mins max to d/l, make a new Inlist, update the working universe and rebalance the port.

Maybe it’s possible to get Value Line stock list from ETF holding list. http://etfdb.com/etf/FVL/#overview

gs3

You can get the Value Line® 100 Index holdings from the First Trust website.

https://www.ftportfolios.com/Retail/Index/IndexComponents.aspx?IndexID=121

Value Line Index performance is not very impressive, much worse than that of the Russell 3000 Index.

I’ve just started experimenting with the First Trust VL ETF. It rebalances only once per quarter while the VL Timeliness holdings reconstitute every week. Anyway, that experiment has only been running for a few weeks so there’s not much to see.

Walter

While Value Line data was available on Port123 I found that my models using VL data worked best looking at the changes in overall Value Line ranking. Stocks moving from 4 to 3 or 3 to 2. Stocks moving from VL rank of 2 to VL 1 underperformed - at least in my models.

Larry

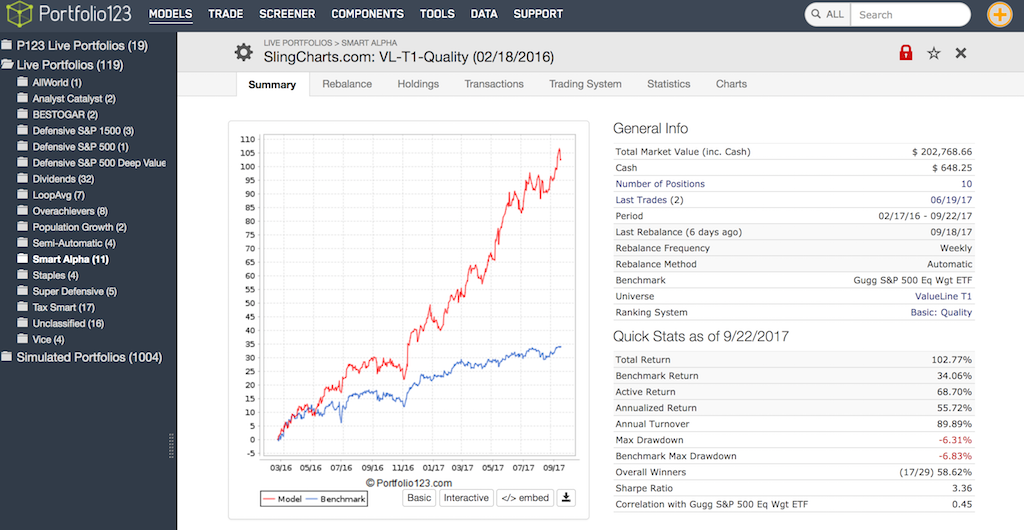

Great job, Andreas! For investors who are willing to keep an open-mind, think and explore the financial world, P123 is a fantastic resource! Here’s an update to my Value Line experiment. It holds 75% large cap and 25% medium cap stocks.

Walter

Nice Walter.

I was struck when reading this article how correlated VL Timeliness ranks were to 26-week past performance. It appears to be a momentum rank as opposed to a value rank.

Thank you, yes indeed, p123 is a game and live changer!

Thanks Parker,

I’ll definitely read the article tonight. I do use a 26W momentum buy rule but it’s applied against Industry price change. Very interesting!

Walter

Miro, thanks for the article link.

Here’s the fact sheet for a large cap mutual fund that invests in VL Timeliness 1 ranked stocks from top-ranked sectors.

https://vlfunds.com/documents/factsheets/VALLX_factsheet.pdf

It matches the S&P 500 over time, but it has crushed it YTD.

Probably due to the recent momentum/size skew. Momentum has been on fire, and large caps have beaten mid & small caps this year.

Their midcap VL1 fund does not have this eyepopping 2017 performance.

I wonder what happens when value comes back in vogue?

Be careful. Article has a pretty small sample size. Six or seven annual holding periods.

yes, agreed. But interesting none the less.

I agree with him a 100%!!!

https://www.cnbc.com/video/2017/10/02/the-full-interview-with-jeff-saut.html

https://www.raymondjames.com/wealth-management/market-commentary-and-insights/investment-strategy

This forum thread was very interesting. It has been a few years, but have you tested, or is it possible to test how likely it is to get fill 1-5% lower (or higher) in the following week after the buy (sell) signal? You say that around 30% are not filled, How do you test this?, and since the variation is 1-5%, do you normally enter a limitorder with “closeprice+ATR”, or something other that calculates the limit to buy (sell) order?