just want to give my two cents on how I am using (and used) p123 and what system to trade my real money account (with tradestation) and

maybe how I we can scale the system together.

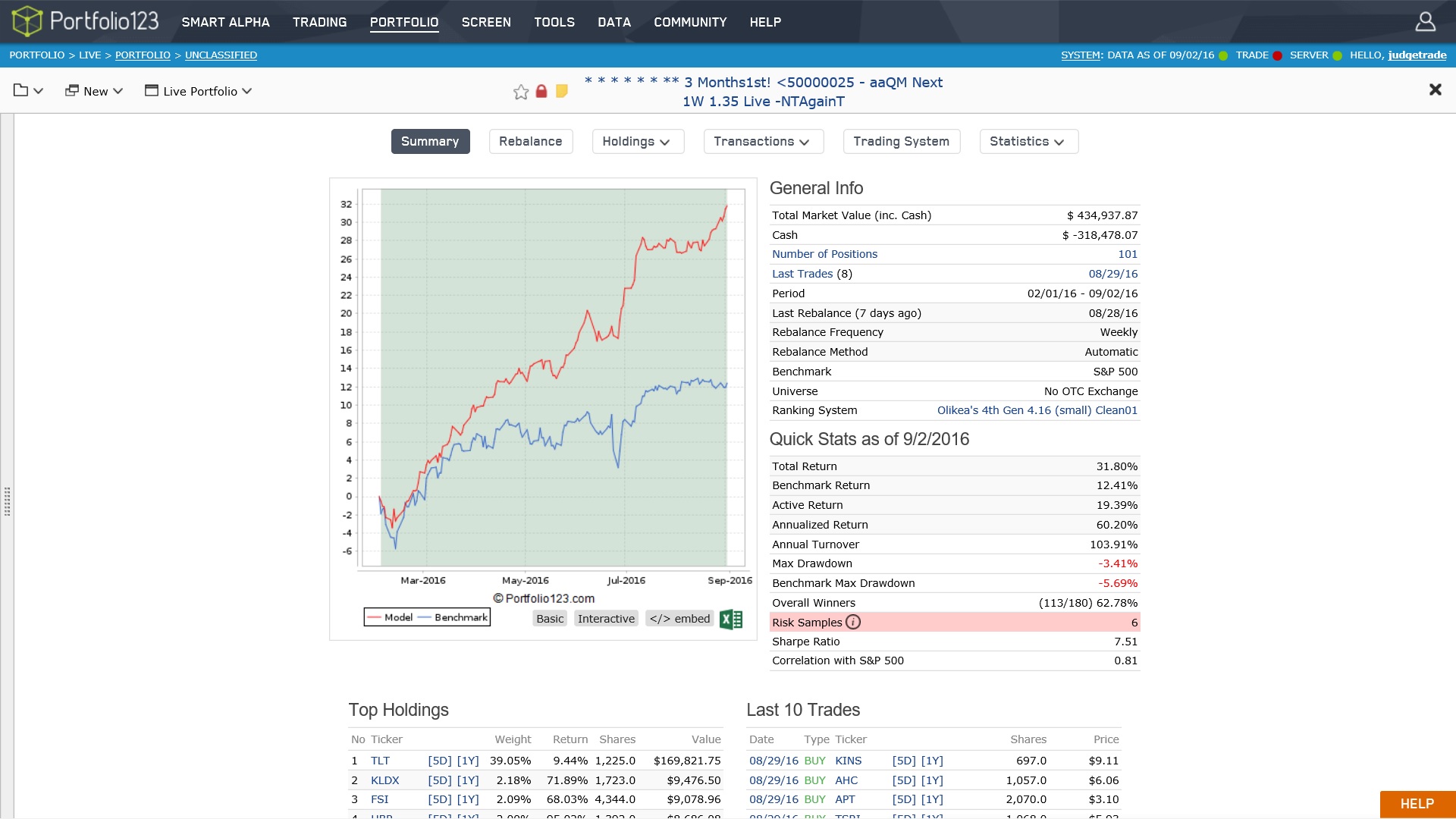

I will update my real time experience from time to time, so far the experience and performance is great, I am

able to implement the transactions of the port very well (e.g. transaction costs assumtions of the system are fine so far).

I will not create a smart alpha out of this (1000 a month is to less relative to portfolio size you could run this with

a very nice performance and I would not be able to control the portfolio size).

If somebody is interested implementing this for Canada (I am not trading there), let me know (will not give away the IP, but happy to provide

weekly signals (I have to get back to p123 staff, if this is possible and if not with my current sub status, what I have

to do, to be able to do this, if a kick back to p123 is needed or a different sub status I am happy to do so.)).

Also if a small cap fund (hedge fund), family office etc. is interested in implementing the strategy, let me know and lets work together, since the strategy can

be run also with much higher liquidity demands and performance deteriorates very slow with higher liquidity demands.

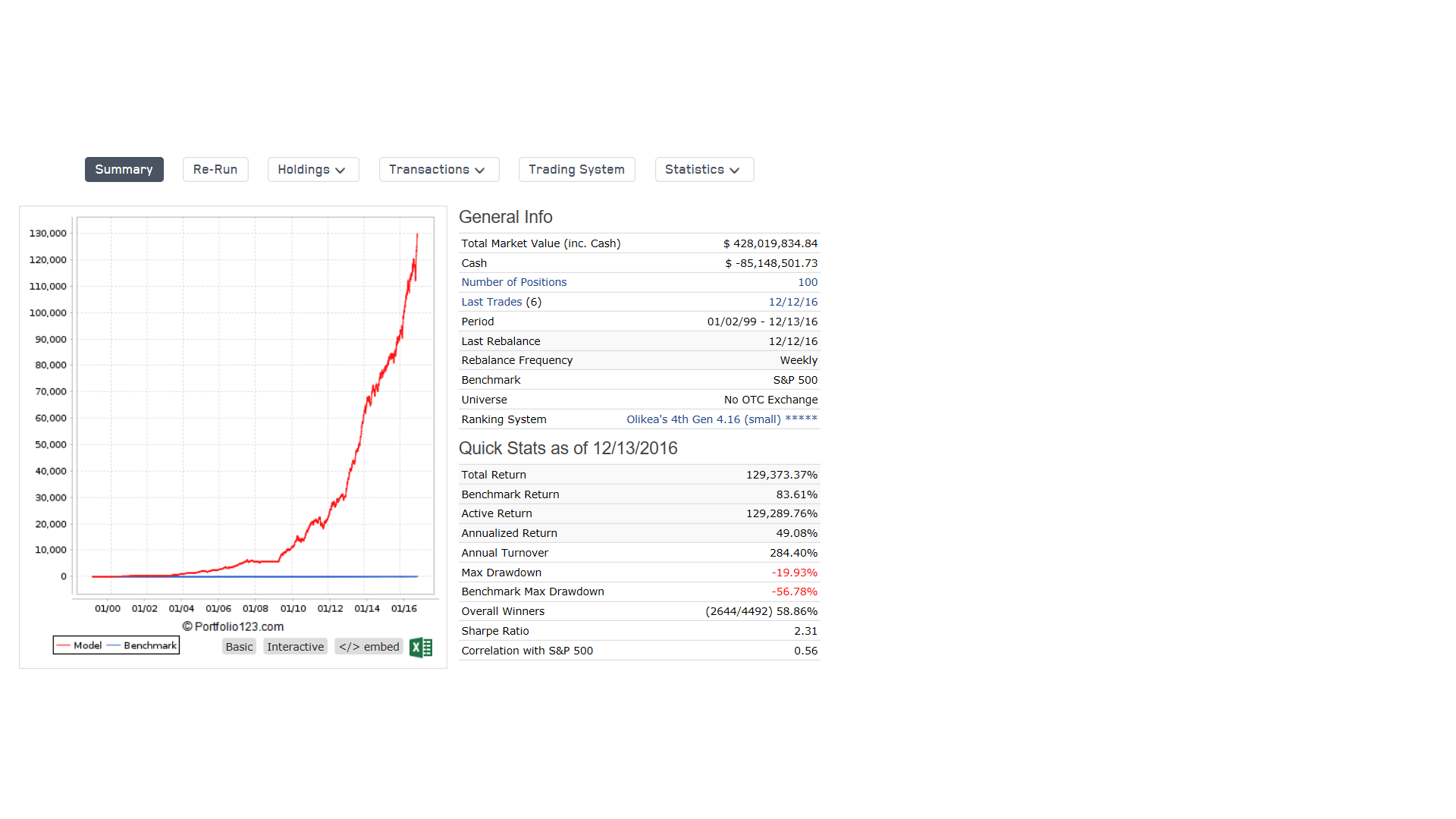

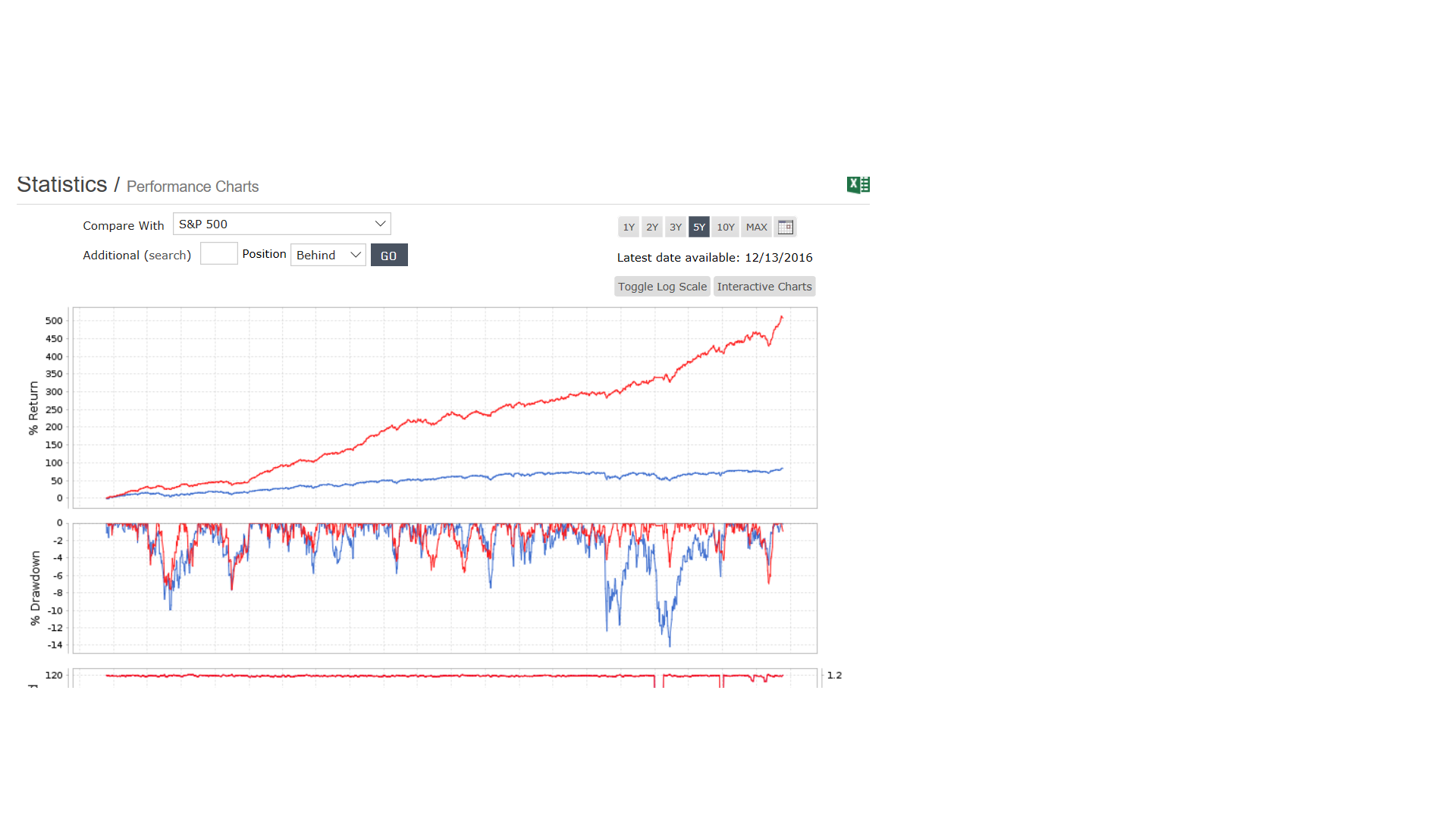

I am sure this strategy can be run (with a 3 Month rebalance and buy and sell algos) with a port size up to 10 Mio. and

be able to generate > 30% performance p.a. with very nice capital curve (e.g. low vola).

This will be especially interesting, if P123 adds more countries, depending on how much this strategy could

scale very well (Country by Country). A shared profit model is intended (e.g. X% of outperformance etc.).

These are very intriguing results. Being in Canada, I looked at the “Canada 50 Stocks” and the top two purchases of AI:CN 245,811 shares and GMP:CN 682,798 shares for Aug 22, 2016 would be nearly impossible to do in a day as these stocks trade with quite low volume. GMP:CN is closely held and while it has had some larger volume days in the past those were “upstairs market” or ‘arranged’ transactions not buy orders that hit the exchange.

May I ask how are you handling liquidity constraints and slippage?

In the US Market (I have no exp. with Canada) this is tradable with o.k. slippage, I trade

with tradestation.

Not with market orders of cause, but with GTC orders 1-5% below (for a buy order) or

above (for sell orders). I adjust every day and get filled, and 30% of the stocks “run away”, so after a week

or two I pay the ask or bid. So yes, there is negative slippage, but there are also stocks

with positive slippage.

Sometimes I move the buy order right away to the bid or the

sell order to the ask, depending on the chart. (What helped me a lot here is Sam Saiden, I think

he is the best technical analyst on the planet, his stuff makes really sense!!!: https://www.youtube.com/results?search_query=sam+seiden+tradestation )

One thing really led me to this system:

I talked to an Private Equity Fund manager: He said, the lower the liquidity, the higher the return.

They calculate 18% annual return for low liquidity investments.

I tested this with p123: a random system that picks low liquidity stocks makes 20% a year (rebalanced

once a year)

But → Psychologically very hard: nobody wants to own micro caps!

But → If you look at all the annomolies (small caps versus big caps, momentum, value, earnings growth etc.), they

are all psychologically hard to trade. No pain, no gain?

Thank you for asking: pretty good!

The picture I post is the actual port I trade of my real portfolio. I gave up the TLT Hedge earlier then in the port, this was a discreationary

descision, give me some time an I will post at the weekend the port with the TLT. See my trade history for my discreationary stuff

here: http://www.stocktwits.com/AndreasHimmelreich

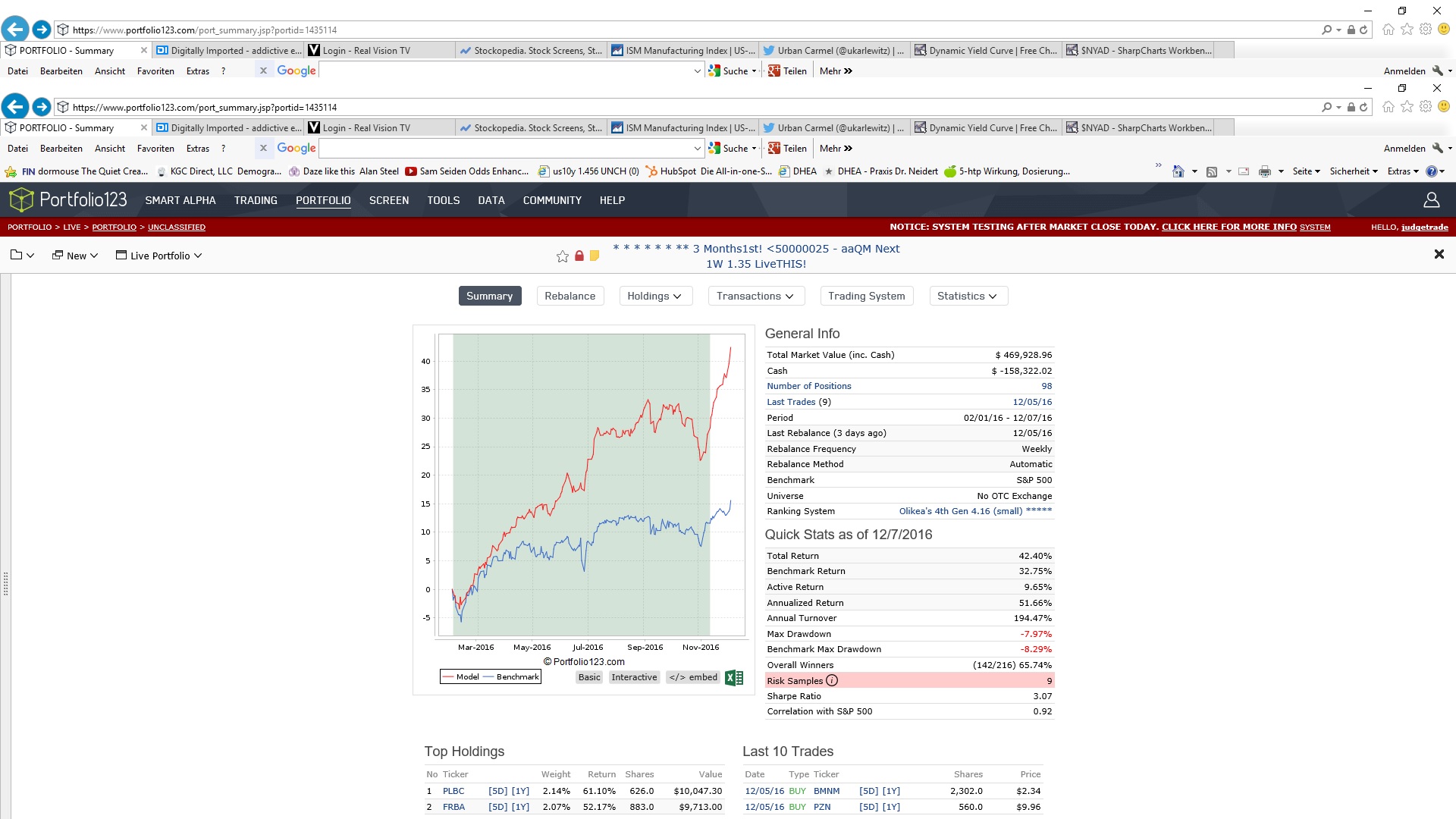

All in all I am up 50%. Though I found two flaws in the empire system:

I did not calculate any interest on the leverage

TLT Hedge only backtestet until 1999, we had a 30 Year bull market in bonds, I can not backtest this really well beforehand.

The warnings from Marc here on p123 got me out of the hedge trade of TLT. (Thank you!!!)

I will update the system (this time with interest for the hedge!) at the weekend and post it here…

got sick at the weekend, will update around Christmas.

I protected my port today with short on VWO (30% of my port), and still got 8% in Bitcoins.

IWM and SPY very, very overextended and I found out that I count my chips every day lately,

good singn for an intermediate top and I want to protect profits without paying tax for this years winnings.

Why VWO: has not participated in the rally, strong dollar kills carry trades and put pressure EMs with

huge dollar denominated debt.

Hi Andreas,

why don’t you just simply buy EUM instead of shorting VWO? Or else short some specific EMs which are particularly exposed to the carry trade?

Thank you Toby!

VWO seemed to have a bit less zing (less beta), also I can be more sure on VWO that it holds its correlation in a real bad event, with derivative based stuff

you can never be sure (in 2008 the credit default swaps to insure the loss of asset backed securites went down or been steady, even

the underlying papers went down). Like to construct my own “Shorts”…