The Trump CRUMBLES in disaster Q&A post is getting long. So I thought it maybe a good idea to start a new post with another Brian Tyler Cohen (9min video) just posted online today.

It is pretty good, (the best part is how President Trump misled investors about tariffs during his campaign now on record),pls take a look if you have time.

The market has been on a bull run since mid-April, following Trump's temporary lifting of the massive "Liberation Day" tariffs. The 90-day pause is set to expire in early July, and it remains to be seen what will happen at that time because Trump's promise of "90 deals in 90 days" has fallen flat on its face. China and other countries are calling Trump's bluff and are finding alternative markets to replace US sales while playing hardball with US trade negotiators.

It appears that, for now at least, investors are piling into the "TACO" trade. By now, everyone has probably heard of that acronym, which stands for "Trump Always Chickens Out," meaning that Trump's tough-guy threats and proclamations ultimately disappear when the public outcry becomes too much. Trump's approach is a classic, "ready, fire, aim," which causes endless and unnecessary harm to both finances and people's lives.

If the past is prologue, Trump will have to find a way to save face on the tariffs, which will likely result in significantly increased volatility as the 90-day deadline approaches. At that time, it will be challenging for investors to separate fact from fiction issued by the administration. However, in the meantime, it's full steam ahead.

Interestingly, there was a robust Zweig Breadth Thrust on April 24, and this measure of Advancing-to-Declining shares has a 100% track record of identifying the start of profitable bull runs in both the 6-month and 12-month time horizons.

I agree that the "90 deals in 90 days" promise probably won't happen since it is already mid-June and there is only one single non- legal binding agreement with UK. All the pending agreements with Japan, Korea, India that was suppose to be "near closing" never materalize.

In addition, there is the uncertainty from the Supreme Court ruling whether Congress should keep the power of the purse (tariffs). I think that market volatility may increase as we head to the end of the month into next month.

Personally, I'm enjoying these Trump performances that obsess news viewers because impulsive investors are currently causing factor returns to remain at a steady high.

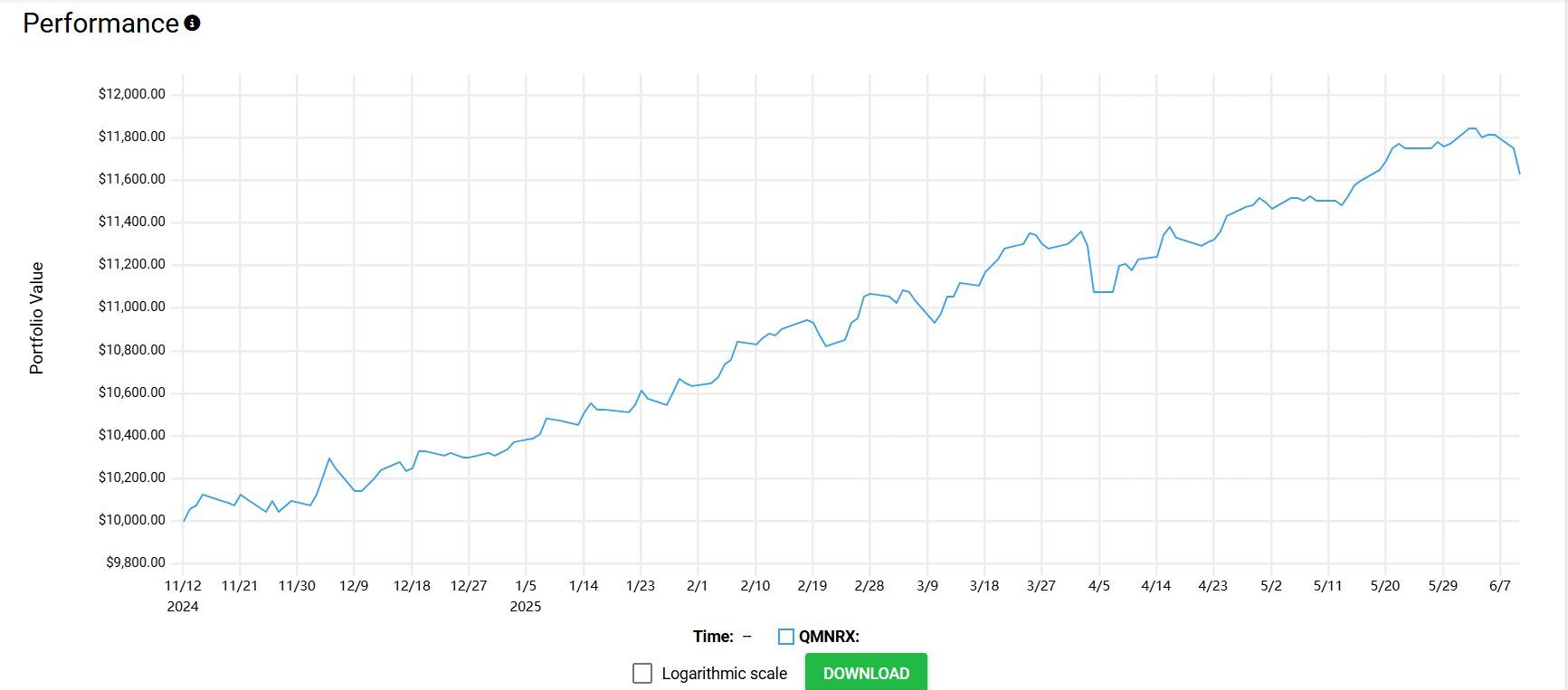

For example, AQR's market-neutral fund has maintained a straight-line upward posture since Trump was elected.

If you believe volatility will pick up in the near future, you can go long VIX futures or buy options on VIX futures. If you don't have the appropriate trading access, you can also buy the appropriate ETFs or options on them.

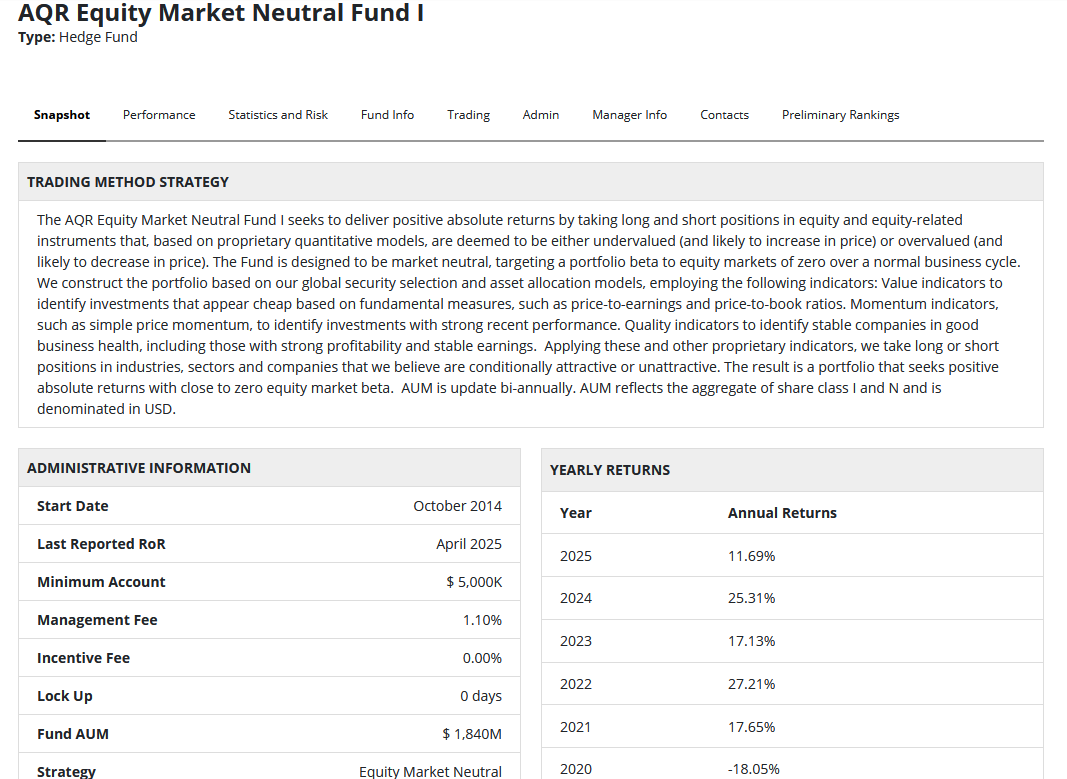

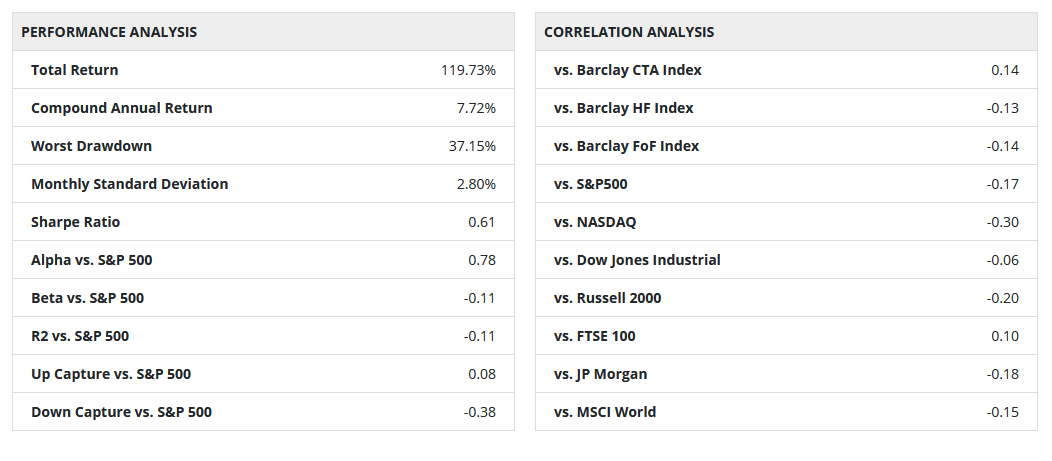

AQR Equity Market Neutral Fund has a poor history of being true market neutral. It has a max drawdown of over 30% since inception in 2014.

(and lost 18% in 2020)

A larger max DD does not contradict market neutrality. Market neutral means that beta is about equal to 0. Your screenshot indicates that beta is about -0.11, so its overshooting that. In 2018-2020 (especially 2020) where common factors underperform, a loss is reasonable for a market netural fund.

A common hedge fund marketing pitch leads to the misconception that market neutrality means good returns whenever. But market neutrality only means that its returns are not dependent on stock beta and would be good if you can get positive alpha over the long term.

In addition, while the madness of 2020 caused considerable pain in the short term for those who adopted the right strategy, in the long term, 2020 rekindled the enthusiasm of retail investors to donate in the casino, which, combined with the return of value spreads, has greatly aided factor returns since then. The current Trump-induced insanity has helped this further.

Thanks for all the attachements, I have skimmed throught them and not going to read all of that (some are not related to market neutral strategy).

However, I don't think even professional portfolio managers can tolerate and invest in a market neutral strategy with a 37% MDD (without getting fired or terminated).

To add to your post, here is something that is more straight- forward and maybe relevant to all.

Market Neutral Fund is a type of mutual/hedge fund that seeks to deliver consistent returns regardless of the direction of the market. The fund aims to achieve a net-zero exposure to the broader market by taking long and short positions in different securities.

Here's a more detailed explanation:

Market Neutral Strategy:

This strategy seeks to profit from mispricings or inefficiencies in the market by taking long and short positions in securities that are expected to converge in price.

Hedging:

By combining these positions, the fund aims to hedge against market risk. The goal is to minimize the impact of market swings on the fund's overall performance.

Alpha Generation:

Market-neutral funds strive to generate "alpha," which is the excess return earned beyond what a typical market index fund would achieve. This is achieved through the fund's investment expertise in identifying mispricings.

This is indeed one of the reasons why people who can stick to the right simple factors after 2020 can be very well rewarded. Almost all clients, owners, investors, allocators, and managers can't stand this perfectly reasonable DD.

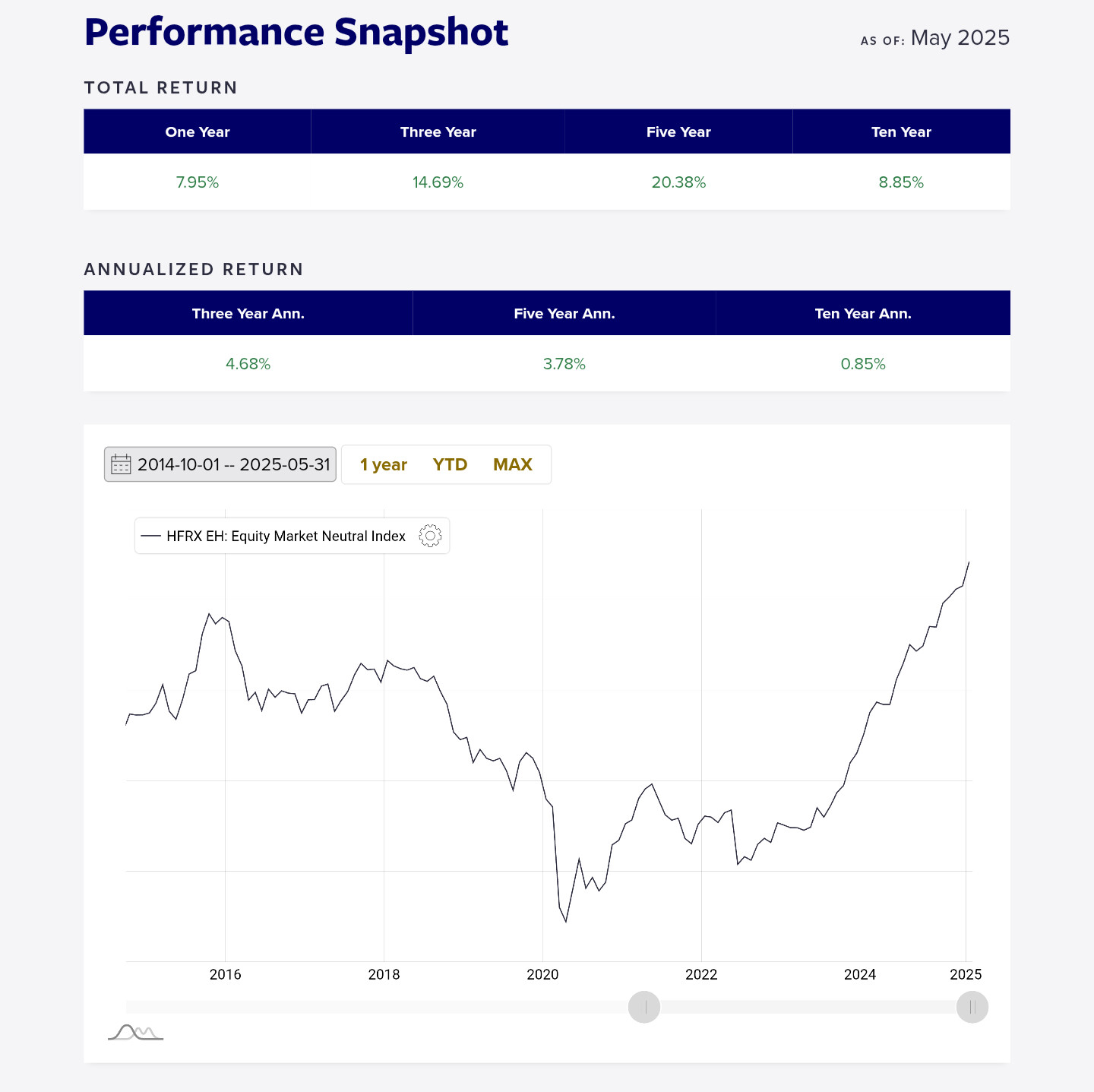

This is also one of the reasons why the Market Neutral Hedge Fund Index does have a lower DD, but it only has a Sharpe ratio of -0.27 and has positive beta and negative coskewness.

Note that this still occurs in the presence of various biases such as backfill bias (especially in the early years, although relatively small in the HFRX index). Your response gives me a better understanding of why this would happen.

It's a commonly-used clever marketing language. Its substantive meaning is to achieve a low correlation return, but to make people think it's a positive return in almost any situation. This is despite the fact that a sharpe ratio of 0.6 or more is already considered a very consistent return.

This is a misleading statement that gives the false impression that alpha is excess return, even though the two are the same thing only if beta is 1.

This is very relevant to your proposed critique point (max DD), and just isn't a direct explanation of the definition of a market-neutral strategy.

Thanks for the in-depth comments for the definiton on Market Neutral Funds provided by Google AI.

The bottom line is why invest in AQR Market Neutral Hedge Fund since there are multistrategy funds, like Millennium, Veriton, Hudson Bay with better returns (above 12% AR), higher sharpe (above 2) and lower Max DD (less than 10% since inception)?

It's sad to know that you actually have to ask the AI even such basic questions, and don't even know what's wrong with the answer SMFH

However, this is precisely the reason behind the current prevailing opinion that AI's productivity-enhancing effects are limited to those with specialised knowledge, and that its illusions are misleading to those who lack such knowledge LOL