Walter, even if the Hi-Lo Index model SPY-Cash has no excess return over buy&hold SPY it is still beneficial when paired with an ETF because one would avoid major drawdowns that way. I found that trigger values from 3.5 to 6% all provided higher returns. So the model is really quite robust. I think slippage of 0.25% is too high for ETFs. I used the minimum that P123 allows for ETFs, 0.1%.

Hi George, everybody,

The time limit problem with my account solved itself and I was able to investigate this timer a bit more. Bottom line is that it is a useful tool but no panacea (nothing is, as we all should know).

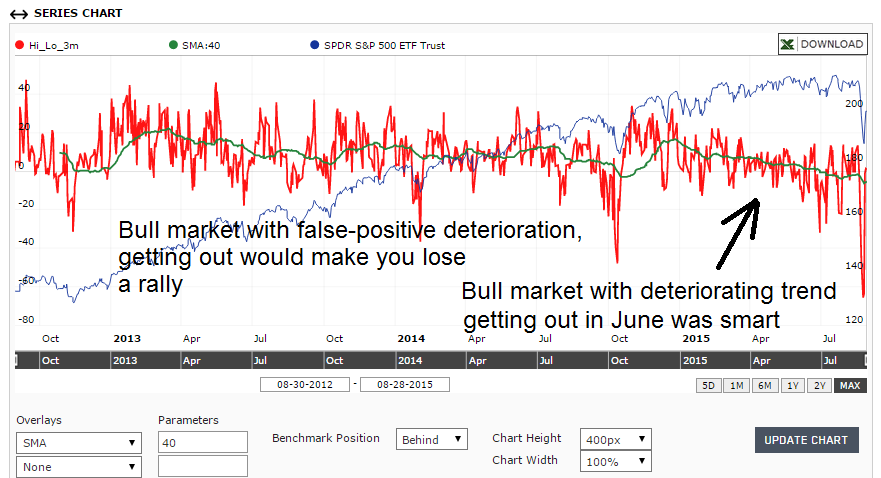

Its useful in the sense that you get to see long trend of sentiment deterioration in the market which usually proceeds sudden breakdowns. You see that especially well if you examine the custom series and use an SMA (or EMA) to filter out its trend. For example in case of a sudden bull market drop like what we experienced in the past 2 weeks, the negative sentiment trend should have been telling to be on the watch. Whether to reduce long positions, increase hedge or any other means it provided a useful signal for traders to consider. But keep in mind that it will often be a false positive signal, getting you out and making you miss a rally. That is why the overall 15 years return for SPY long only screen is merely ~6% annually and you miss many of the rallies.

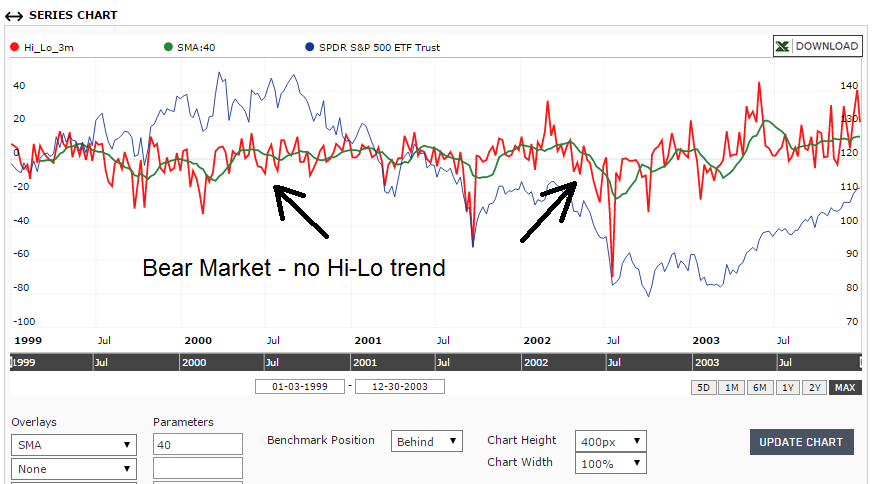

Also important to note that this deterioration signal is far less useful in bear markets where the sentiment is already sour. For example consider the 2000 – 2003 period outlined in my screenshot below. The indicator simply vacillates around zero, it has no trend. So while the 5% threshold does produce some overall positive, there is no magic or special value in that threshold. I don’t think that any experienced trader could look at this chart and at the green SMA40 line and deduce anything useful by whether the green line is above or below any specific threshold. So where does the 5% threshold come from? Like many derived thresholds, it simply happened to produce better result during the entire test case. Call it curve-fitting or call it something else, I don’t believe one can assign too much lasting predictive power to it.

Bottom line: the indicator should be consider as another tool in our chest, a useful one but not more. Don’t build too much into the fact that a threshold value generated a nice overall curve in the past. Next crash may prove to have required different threshold(s) . But if you have several useful indicators to consider whether to be or not in the market – this one can add to the picture. Best thing to do is to look at it manually, not rely blindly on the specific threshold number that happened to do better than others couple of times before.

Please look at my two screenshots below and make your own conclusions.

Just my two cents.

Thanks, Z.

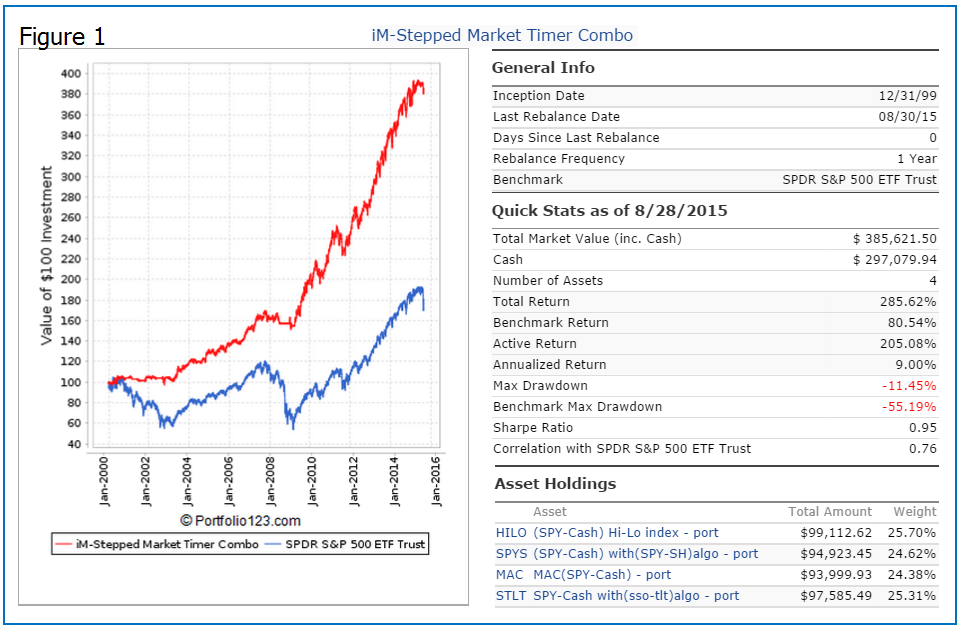

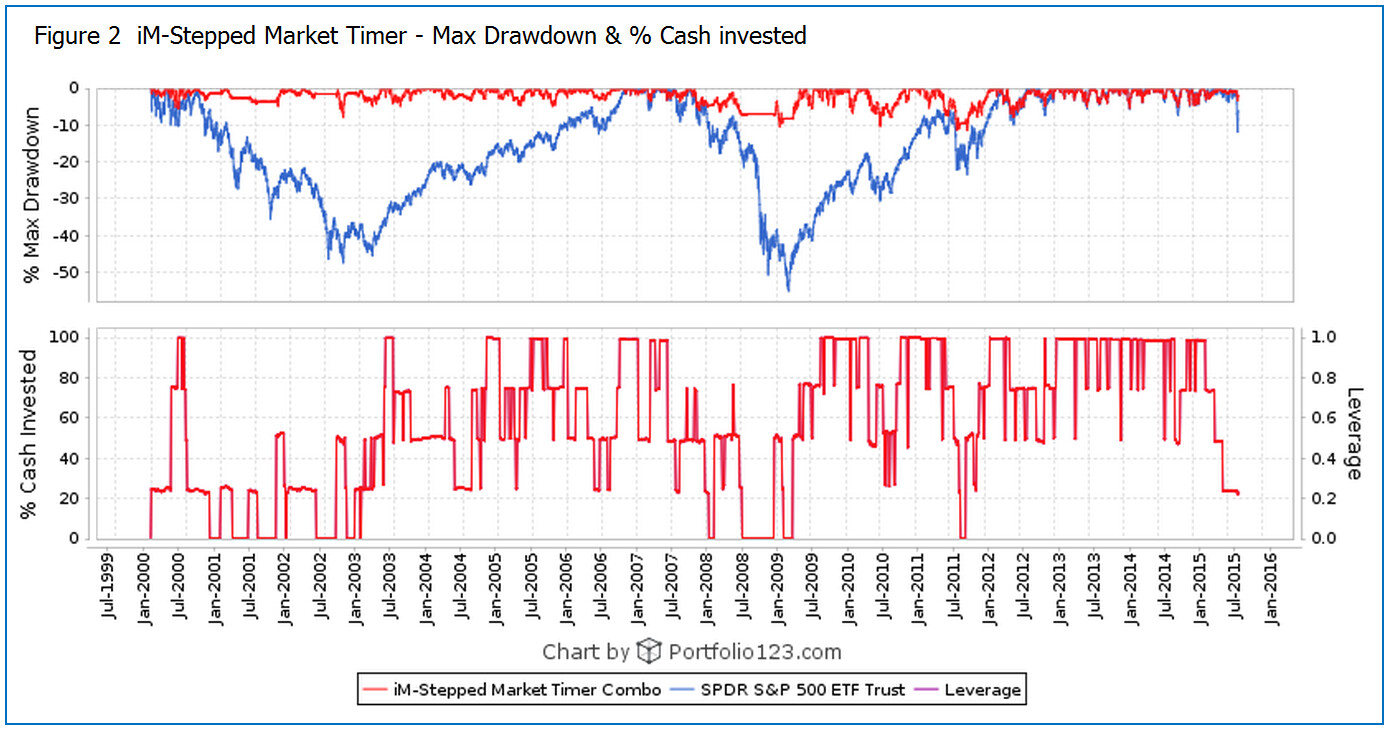

Z., a good summary. i agree with what you said. I use this timer in a combination of timers precisely for the reasons you mention. No timer is perfect on its own, if it was we would all be very rich. One can see the the combo timer is now only 23% invested in the stock market.

Hi Georg, Yes the Max DD under the rolling simulation run looks very good. Thanks for your help.

Here is an interesting backtest using the Hi-Lo Index (Date range: 1/1/2005 to 9/30/2015):

http://alvarezquanttrading.com/2015/11/11/hi-lo-index-as-a-market-timing-indicator/

He wanted to know how well would it work on a S&P500 mean reversion strategy.

All rules are listed for his model.

He shows an annualized return of 13% with a max D/D of -17% and a market exposure of only 52%. Also the average % profit/loss took a big jump up when compared to a SMA200 timing strategy, and the average of the 5 worst drawdowns, dropped dramatically. From 16.30 to 12.20, or about 25%.

I used Bloomberg data from 1990 to replicate this strategy with two variations

-I traded on daily basis, not weekly

-I used the 12-week high and lows instead of 3-month high and lows

And the numbers were quite worse. It did well during the 2008-2009 crisis. It didn´t avoid the 2001 crisis and in the 90s did really bad

Book11.xlsx (494 KB)

And how did it do without the 2 variations? (particularly the weekly / daily one - I would think it is the main difference)

Jerome

How does it look from 1/2/2000 onward?

Your model should look like the SPY-Cash in

https://imarketsignals.com/2015/avoiding-stock-market-crashes-with-the-hi-lo-index-of-the-sp500/