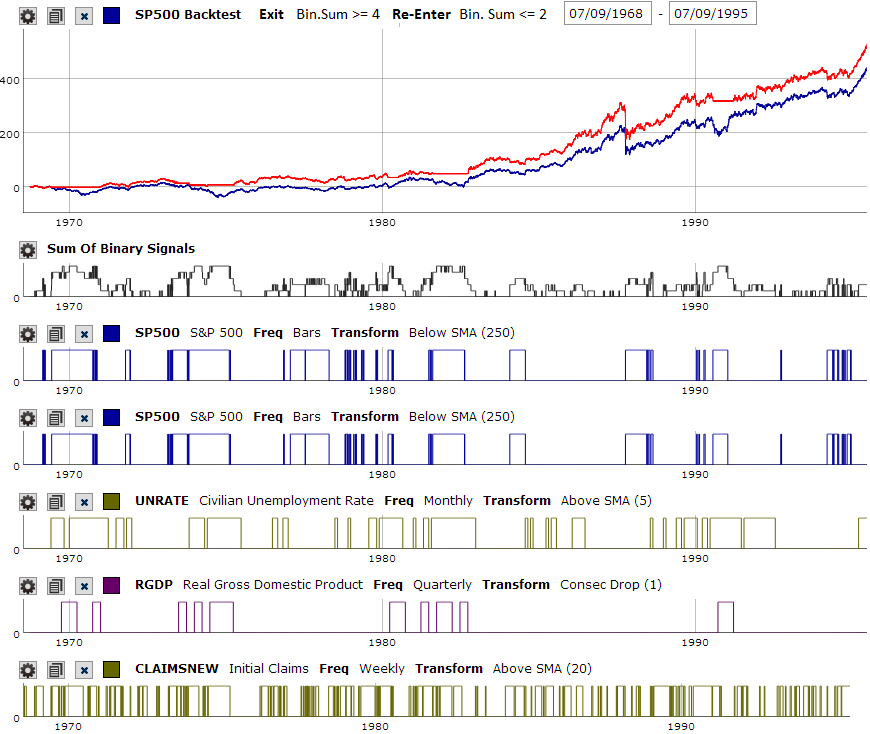

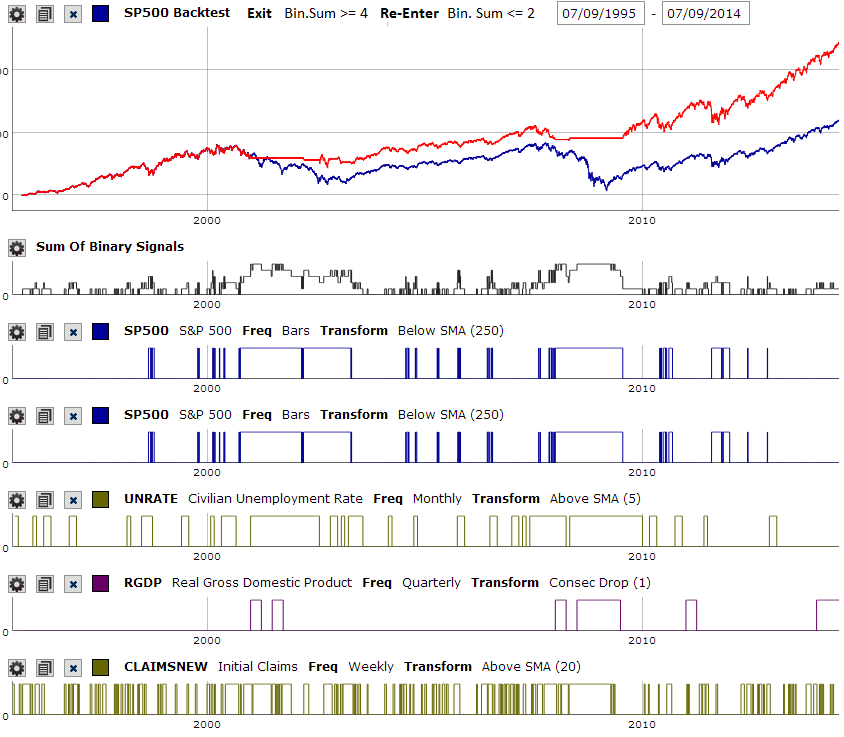

As mentioned in this post the upcoming MarketScore graphical tool will include a backtest feature. I put together a MarketScore with the following binary signals that are considered bearish:

Wght Condition

2 SP500 below 250 average

1 Unemployment rate above 5 month average

1 GDP below previous quarter

1 Initial Claims above 20 week average

I put a double weight to the SP500 technicals so the highest possible value of the MarketScore is 5, the lowest is 0. I then backtested the above score as follows:

Exit the market if the Binary Sum >= 4

Re-Enter the market if the Binary Sum <= 2

Below please find images of the backtest. One was from 7/9/1968 - 7/9/1995, the other from 7/9/1995 - 7/9/2014. Looks like it did pretty well in most bear markets except the 1987 crash, avoided a lot of draw-downs and handily outperformed.

We plan to release this by end of the week including the ability to save your system. The ability to use MarketScore within sims/ports/screens/etc will be next.

NOTE: I double weighted the SP500 technicals by adding two binary charts

I did the same thing with RGDP. But I had to wonder if it was PIT (seldom does anyone come on the TV and say we entered a recession today). It says specifically that it is not point in time.

I have had good results with tests that are point in time and there are many. Indeed, it looks like you results would have been as good without RGDP.

Wow, good stuff! I assume that you would envision including this in simulations and ports, as a separate layer for market timing? Could be useful to then reallocate to bonds instead of cash.

There’s a backtet button now but it’s not using point in time. The backtest results are therefore no good. We should have point in time backtest by end of the week.

We’ve also uncovered many other issues with ALFRED data that we are correcting:

some series were filled in sometimes in 2000, but go back to 1950. For those we are artificially lagging the point in time data by the average lag of past reports

quarterly/monthly series periods in FRED come in with a date at the beginning of the period. For ex Q1 of 2014 has a period date of 1/1/2014. We are correcting those to be 4/1/2104

Also

we’re adding EMA to the transformations

we need documentation

Keep in mind the graphical interface to market score is just a playpen. You will be able to create a market score that can be referenced from rules. This market score will be able to do everything the graphical tool can do, but also have access to any TA functions that we have.