Over the past few years, I have created several systems that have performed well in backtests and continued to perform well out of sample.

Currently, I am working on a global portfolio where, after reviewing some of Yuval's threads, I have created four ranking systems optimized for four different sub-universes, and then merged them afterward. This gives 289 different criterias. As I understand him, the four different ranking systems should be merged, fully in the final system. However, I would like to test out some different ideas also.

Therefore, I am in the process of creating a web application in Claude, which I would like to share when it is finished. That incorporates some good ideas on how to construct, merge, re-weight, or split up ranking systems to see if it can improve them.

I have come up with some ideas, but I need more from you:

⊞

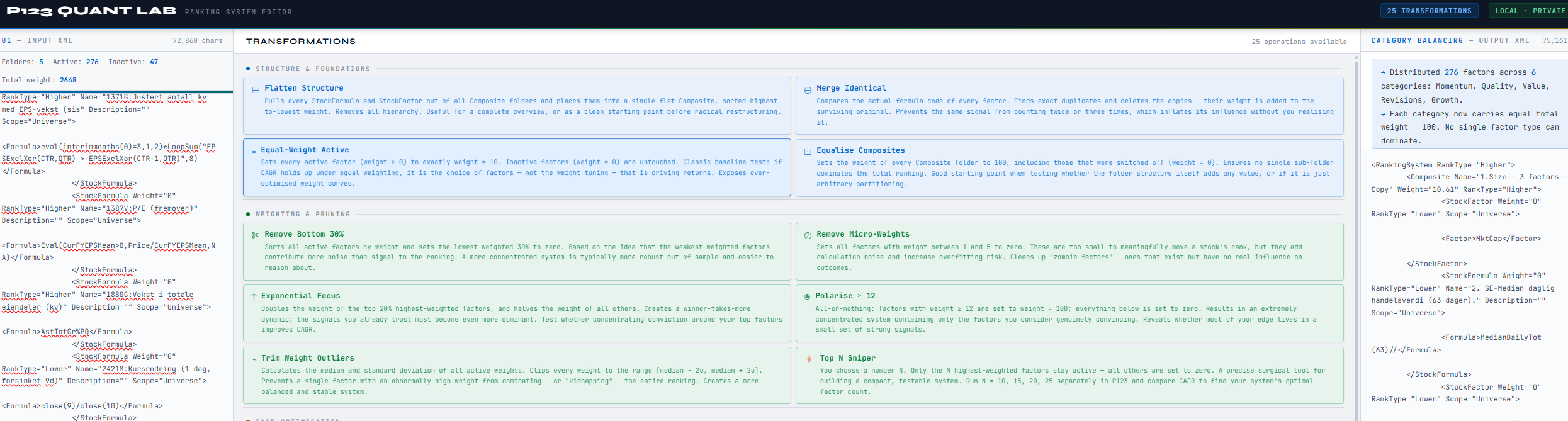

Flatten Structure

Pulls every StockFormula and StockFactor out of all Composite folders and places them into a single flat Composite, sorted highest-to-lowest weight. Removes all hierarchy. Useful for a complete overview, or as a clean starting point before radical restructuring.

⊕

Merge Identical

Compares the actual formula code of every factor. Finds exact duplicates and deletes the copies — their weight is added to the surviving original. Prevents the same signal from counting twice or three times, which inflates its influence without you realising it.

≡

Equal-Weight Active

Sets every active factor (weight > 0) to exactly weight = 10. Inactive factors (weight = 0) are untouched. Classic baseline test: if CAGR holds up under equal weighting, it is the choice of factors — not the weight tuning — that is driving returns. Exposes over-optimised weight curves.

⊡

Equalise Composites

Sets the weight of every Composite folder to 100, including those that were switched off (weight = 0). Ensures no single sub-folder dominates the total ranking. Good starting point when testing whether the folder structure itself adds any value, or if it is just arbitrary partitioning.

Weighting & Pruning

✂

Remove Bottom 30%

Sorts all active factors by weight and sets the lowest-weighted 30% to zero. Based on the idea that the weakest-weighted factors contribute more noise than signal to the ranking. A more concentrated system is typically more robust out-of-sample and easier to reason about.

⊘

Remove Micro-Weights

Sets all factors with weight between 1 and 5 to zero. These are too small to meaningfully move a stock's rank, but they add calculation noise and increase overfitting risk. Cleans up "zombie factors" — ones that exist but have no real influence on outcomes.

↑

Exponential Focus

Doubles the weight of the top 20% highest-weighted factors, and halves the weight of all others. Creates a winner-takes-more dynamic: the signals you already trust most become even more dominant. Test whether concentrating conviction around your top factors improves CAGR.

◉

Polarise ≥ 12

All-or-nothing: factors with weight ≥ 12 are set to weight = 100; everything below is set to zero. Results in an extremely concentrated system containing only the factors you consider genuinely convincing. Reveals whether most of your edge lives in a small set of strong signals.

⌁

Trim Weight Outliers

Calculates the median and standard deviation of all active weights. Clips every weight to the range [median − 2σ, median + 2σ]. Prevents a single factor with an abnormally high weight from dominating — or "kidnapping" — the entire ranking. Creates a more balanced and stable system.

⚡

Top N Sniper

You choose a number N. Only the N highest-weighted factors stay active — all others are set to zero. A precise surgical tool for building a compact, testable system. Run N = 10, 15, 20, 25 separately in P123 and compare CAGR to find your system's optimal factor count.