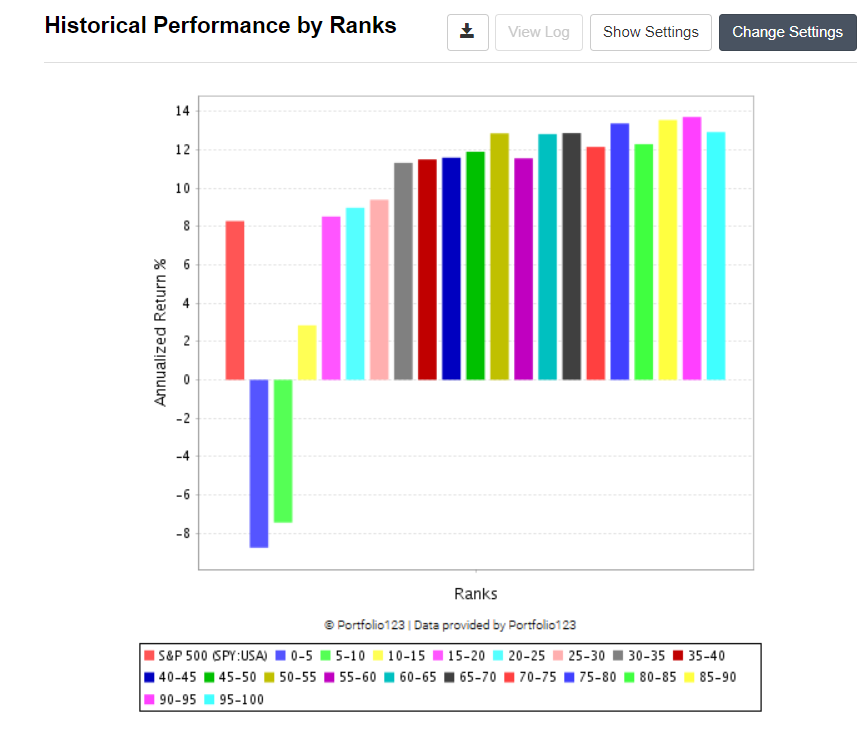

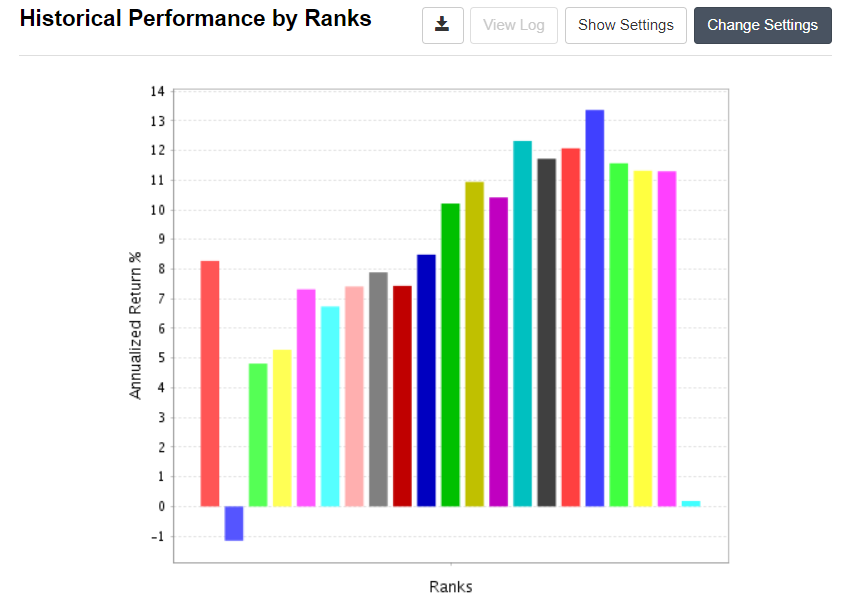

Ranking these factors in buckets - lower is better, on an appropriate universe, seems to obtain pretty consistent results. I obtain similar results for European companies.

The only issue is: I do not have a real explanation for this result, nor can I find any consistent explanation online.

If I had to come up with an explanation, it would be as follows. Other investors do not look at what the equity of the company consists off, and hence give equal weight to other equity based line items as they do to capital surplus, while in fact this is not optimal. But maybe I’m just backwards rationalising a decent working factor here, and maybe this is just a statistical fluke.

Here are few possible reasons: I admit to checking my ideas with ChatGPT. I admit that I would not have thought of" Risk of Takeover" and “Economic Uncertainty” on my own. Poor Capital Allocation (and the others listed) have been mention previously in the Forum (by Marc Gerstein and Yuval for example) and I had made those ideas my own already. Although I would have posted some of these ideas on my own, no doubt ChatGPT said it better. I included the all reasons for completeness and went with the way ChatGPT said it.

Apple is a company that has been accused of holding onto capital and therefore not providing “shareholder value” through dividends or stock repurchases. Maybe their stock could have done even better but that would be pure speculation on my part as I not sure how far you can take this single factor.

I might mention that almost all of the reasons below could be rolled up into Marc’s DDM (dividend discount model) as most companies should be calculating this internally, if my superficial understanding of finance is correct. So you could say that a company is knowledgeable about itself and the DDM calculations are not predicting good growth (causing them to not invest and to hold onto capital) or they have bad management that is not doing the DDM calculations very well–as suggested by the first reason (“POOR” Capital allocation)…

Poor Capital Allocation: If a company has a significant amount of excess capital and no plans to invest it, it might signal poor capital allocation strategies. Successful companies usually have efficient capital allocation plans, investing their surplus capital in areas like new projects, research and development, or acquisitions to fuel growth.

Low Growth Opportunities: Excess capital might also indicate that the company is not finding sufficient growth opportunities in its market. This could be a cause for concern as it might signal saturation in the company’s current market, lack of innovative products or services, or inability to expand into new markets.

Shareholder Value: When a company retains more capital than necessary, it could be a sign that it’s not returning enough value to its shareholders. Companies can return capital to shareholders through dividends or share buybacks, which can increase shareholder value. A large amount of excess capital could indicate that the company is not taking these opportunities.

Inefficient Operations: Some might interpret excess capital as a sign of inefficiency. If a company is consistently producing more cash than it can invest effectively, it might be a sign that it’s not managing its operations efficiently.

Risk of Takeover: Companies with large cash reserves can sometimes become targets for takeovers. Potential acquirers could see the cash reserves as a way to partially fund the acquisition.

Economic Uncertainty: If the economy is uncertain or entering a downturn, companies might retain more capital to weather the storm. However, this would also indicate that tough times are ahead.

I think the way Portfolio123 defines CapitalSurplus is actually different from 'excess capital' that you (or ChatGPT) describes. It is roughly described as the additional paid-in capital in excess of par value that an investor pays when buying shares from a company.

Ah, thank you. But hmm… I wonder if Yuval (who is more knowledgeable on these things) does not think the two are pretty related.

Specifically, I wonder if the forms of capital would be equally available to be used for any investment that might be considered growth opportunities by the company. Especially considering this from the web: “So while both APIC and excess capital refer to forms of capital that a company can use they come from different sources…”

But clearly you are right. ChatGPT sees a difference (as you do) calling what P123 uses:" Additional Paid-In Capital (APIC)." I will spare you the rest of ChatGPT’s response and look forward to what people who are better at finance have to say on the subject.

Looked into this just a bit… looks like retained earnings can cause capital surplus, but so could just selling a large number of shares @ a price significantly above par (which is typically a very low number). Sounds like high capital surplus could be correlated with (among other things) a significant amount of share issuance, having a high price per share, or both.

Companies that have sold a large number of shares for a lot of money but have poor sales are going to have a very large ratio of capital surplus to sales. That’s pretty obviously not a good thing.

Edit: What I said may have been correct but I think I should have a better understanding of “parr value” (and how, exactly, that value is set) before trying to contribute. Finance is not a strong-suit of mine. Yuval, thank you for the reference.

“Par value” has a very clear meaning for bonds and other fixed-income instruments. But for stocks, it’s just the value on the stock certificate. The par value for Amazon stock is $0.01 per share but for Apple it’s $0.00001 per share. For most companies the par value of their shares is pretty close to zero, which means that capital surplus is basically the total selling price of all issued shares (at the time they were issued).