After having used another screening tool for European stocks, where I have done quite, I am new to Portfolio123 and have begun my first screens, backtests and building an actual real money portfolio (unfortunately not yet using all the great functionalities of Portfolio123).

If possible can you please share the backtest results for Max, 10 Years, 5 Years and 1 Year for portfolios you tested and actually implemented? I am curious as to what is considered a good “past performance”, and then if you have confirmed those numbers with real money Portfolios.

(my curiosity also comes from the fact that the other tool I use doesn’t allow for backtests)

I will start things off with a portfolio that I have refined using similar factors as my 3 year old European money Portfolio but with even better past performance:

My real money performance since 11/1/15, when I started using P123’s ranking systems, is 43% annualized. My simulated performance, using 0.4% slippage, for the system I’m currently using, is 112% annualized for max, 95% for 1 year, 108% for 5 years, and 109% for 10 years. It’s long only, no margin.

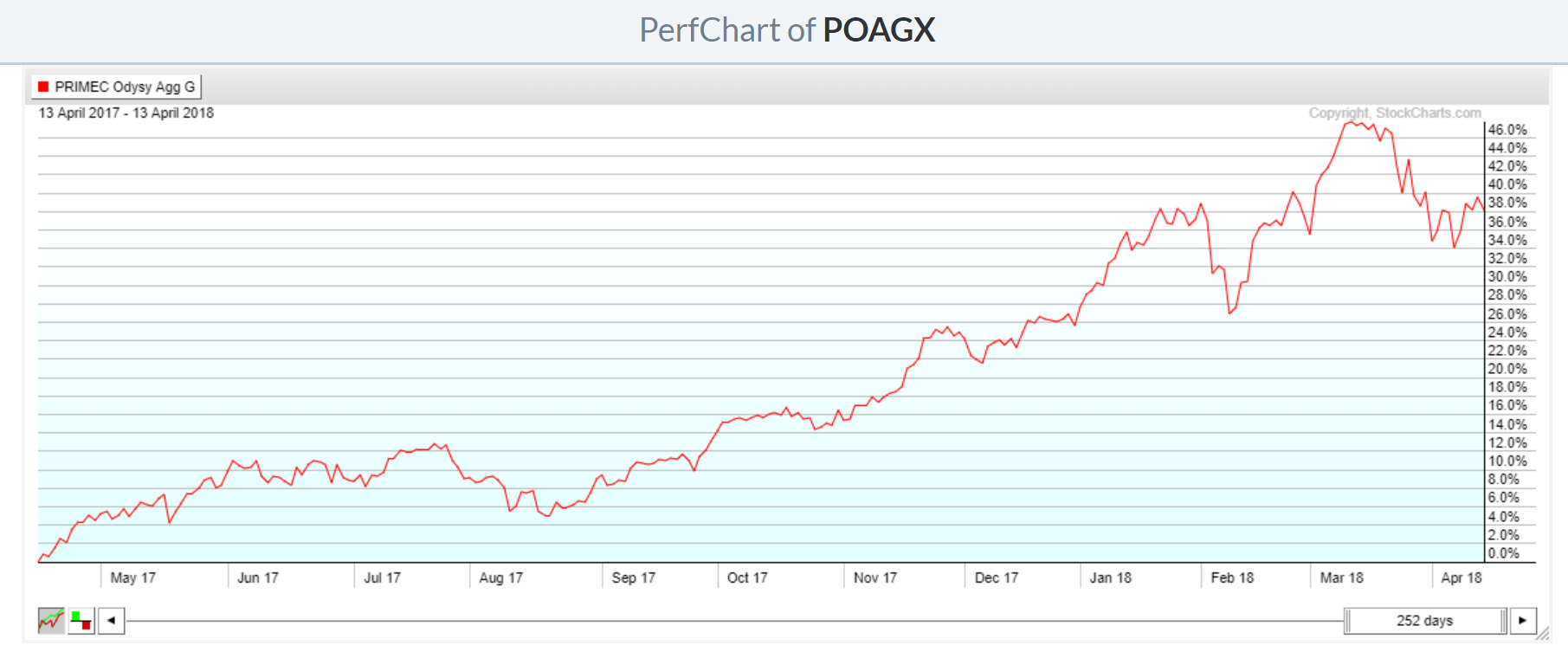

I just started “systematic” investing in February. So far, I am doing a 26% CAGR in the real world, while simulated performance is at 46.6% CAGR.

By comparison, the Russell 3000 is up 3% annually over the period.

The difference between actual and theoretical is due to the execution of illiquids. I don’t get what I want. And I can’t get rid of what I don’t want. I knew this would happen, but wasn’t sure how exactly it would play out.

In response, I’ve started to rebalance daily. All liquids execute Monday; the rest passively execute throughout the week. If I don’t get what I want, I pass. If I can’t get rid of something I don’t want at an advantaged price, then I just push. On the upside, this tends to lower turnover and transactions cost, though I’m not sure how I could simulate this.

The best answer to your question will come from looking at the Designer Models in an objective way. There is a lot of data there. The designers have a financial incentive to create a good model. And you have a sample with a limited amount of selection bias and cherry-picking (not zero selection bias/survivorship bias however).

And you should read “Skin in the Game: Hidden Asymmetries in Daily Life” by Nassim Taleb. Taleb can tell you—in his own words—what the book is about more generally.

But with the Designer Models people have a little skin in the game.

2011 10% Joined www.portfolio123.com and systemized

2012 30% 5 Stock Momentum, Value

2013 20% 100 Stock Book, Momentum, Value, Micro Caps, 3 Month rebalance

2014 15% 100 Stock Book, Momentum, Value, Micro Caps, 3 Month rebalance

2015 0% 5 Stock Momentum, Value (should have stiked to the 100 Stock Book!)

2016 58% Improved old System that I used from 2012-2014, but weekly rebalance

2017 35% Improved old System that I used from 2012-2014, but weekly rebalance

before p123

1996 100% First Year, Bic Cap Momentum Discretionary

1997 46% Momentum Discretionary

1998 147% Momentum Discretionary

1999 53% Momentum Discretionary

2000 55% Momentum Discretionary

March 2001 55% Here I thought I am unbeatable

End of 2001 -41% Was short in March 2001 but went long again

2002 -50% was long!

2003 0% took 50k out to finance a PHD (Trend Following, Momentum)

2004 0% PHD done System created (with another platform) : see https://www.portfolio123.com/app/r2g/summary?id=1290029

2005 0% Break (concentration on main Job)

2006 0% Break (concentration on main Job)

2007 0% Break (concentration on main Job)

2008 -25% should have used my PHD System (it was out of the market!!!)

2009 -25% should have used my PHD System (it was out of the market!!!)

I think you are unbeatable,

around 10 years of negative market experience, you came back with determination to invest money and become successful. Thank you for sharing personnel success. I believe this kind of hardwork and determination required to be successful in the market.

3 to 4 years ago, One of my inspiration to stay with p123 is your designer model’s out sample performance.

my perspective

Keep positive learning/good things and eliminate mistakes going forward is routine work for professional game player/athlete, Believe designing model is no different.

So, I will stay relevant every quarter and every year, as athlete stay fit every day by workout. It is not competition, it is a challenge to stay focused, humbled with discipline just follow the market and stay fit with the knowledge.

I am following best mutual fund performance, if i stay calm and disciplined similar to mutual fund managers, I will keep learning and grow my account every year.

good mornming, very impressive results

is it possible to have updated (jan 2022) data of your system ? just to see if it continue to works as in the past and to have and updated benachmark for me ?

thank you very much and best regards

{kind=link}