Jim,

Earnings estimates for S&P 500 stocks are falling but those for the S&P 1500 are still rising. I suspect that a few mega oil majors are pulling down the average for the 500. What does that mean for the economy? I don’t know. I would guess that the economy is still okay, but I am keeping an eye on it. Theory says that low oil prices are good for the economy. Theory also says that there is no difference between theory and practice, but practice says that there is. My earnings based market timing system that I developed after studying 75 years or so of data and that I use in a couple of my R2Gs is still in the market, but I am watching developments carefully to see if the economy overall is staying healthy.

I use US Government bonds as a hedge as that is currently the worlds safe haven asset and tends to spike with volatility. Between my Bond R2G and another private portfolio I am invested > 40% in US Treasuries.

My best guess for the cause of falling oil prices is that the Chinese economy is hurting much more than the Communist party is letting on. Oil prices don’t usually fall so fast due to more production, but they do tend to fall off a cliff under certain types of recessions. China is now a significant chunk of the world and can affect the world. A Chinese recession may not affect us here in the U.S. because the U.S. are consumers while the Chinese are producers. A Chinese recession may not affect us here in the U.S. because the US are consumers while the Chinese are producers. However, much of the growth in jobs since 2008 in the U.S. has been in the energy sector, and with prices falling some of those jobs may not be maintained.

All,

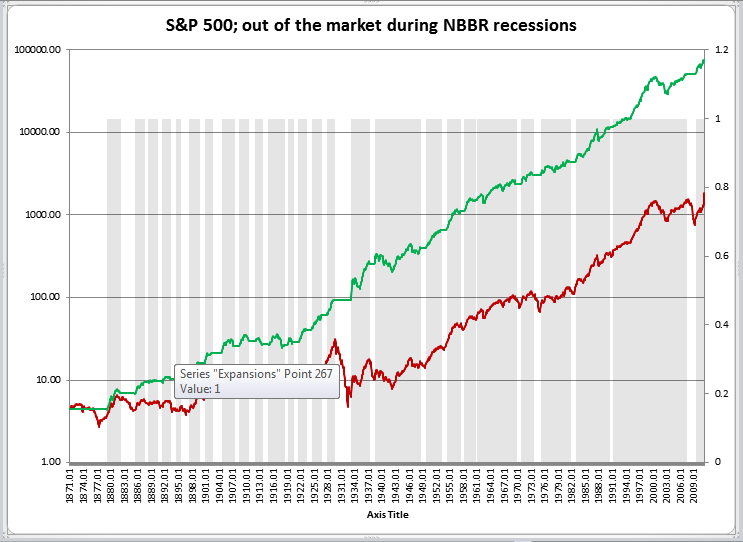

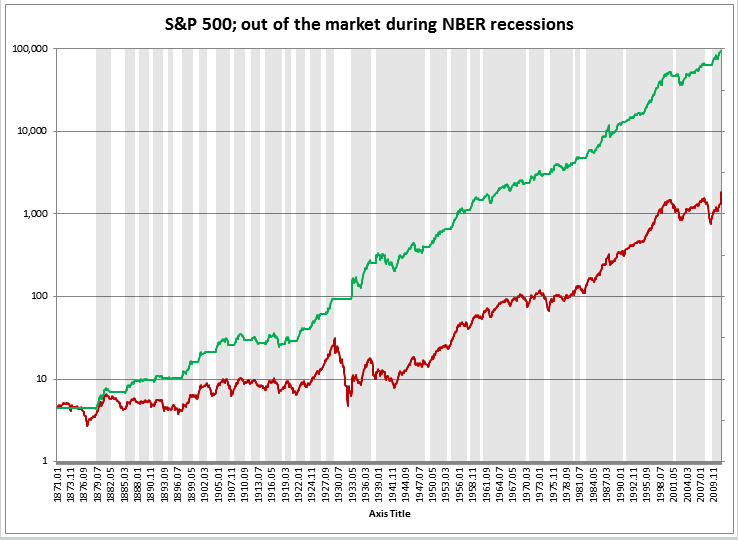

Over the past 75 years or so in the U.S., every time that the economy went into a recession it took the S&P 500 (large caps) down with it by at least 20% (which is the accepted definition of a bear market). Those recessionary bear markets were generally long and grinding. The S&P 500 did go down by 20% without a recession a few times (such as in 1987) but it recovered relatively fast. It stands to reason that any earnings based model should have gotten you out of the bulk of those bear markets, but different models may have started a little earlier and/or ended a little later.

MA timing would also have gotten you out of of the bulk of the recessionary bear markets but would have gotten whipsawed on many of the quick corrections, because by the time a down trend started to form it began to bounce back. It would take a lucky MA based system to get out of those quick corrections in time. My conclusion has been that earnings based timing is better than MA based timing.

Some may argue that there are other things that can bring the market down besides recessions and therefore MA based timing feels more secure for them. If it works for you then fine, earnings based systems have fewer false positives.

I did my testing on large caps. It is possible that earnings estimates based systems don’t work as well in the small cap space. Small caps tend to fall much more often than large caps especially when relative valuations are higher as they are now.

(Disclaimer: I don’t have access to the data right now and this is all from memory).

{kind=link}

{kind=link}

{kind=link}