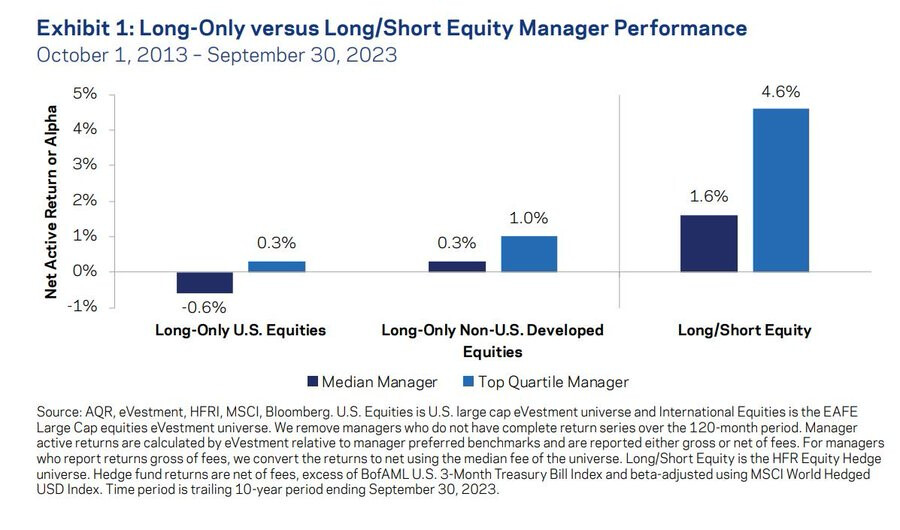

As seen in this research below, the median long-short equity strategy generates alpha while the median long-only does not.

Long/Short equity generates 1.6% alpha (excess return) for the median manager and 4.6% alpha (excess return) for the top quartile manager. The alpha (excess return) for the Top 10% should be even higher.

Isn’t this a bit silly? If the market return is the aggregate of all investors and a large number of those are equity managers, then obviously the aggregate alpha is going to be zero. And a long/short equity strategy will have a very low beta and therefore a high alpha, even if it lags the market. Measuring long/short success by alpha makes no sense because it’s impossible to construct a long/short market return. Here’s an example of a long-short strategy:

Notice that the model’s return severely lags that of the S&P 500, but it has an alpha of 2.38% because its beta is so low.

I don’t have the whole research paper but according to this screenshot which is part of the research that was sent to me by a friend, it does mentioned net active return (excess return - I assume above benchmark) which is what most hedge fund manager are chasing (as well as low beta and correlation to the market).

Furthermore, the screenshot above shows the result of the median and top quartile performance of a group of hedge fund managers. The performance (alpha/beta) of an individual long/short model can varies a lot and depends on how successful the long/short strategy go against the prevailing market condtions.

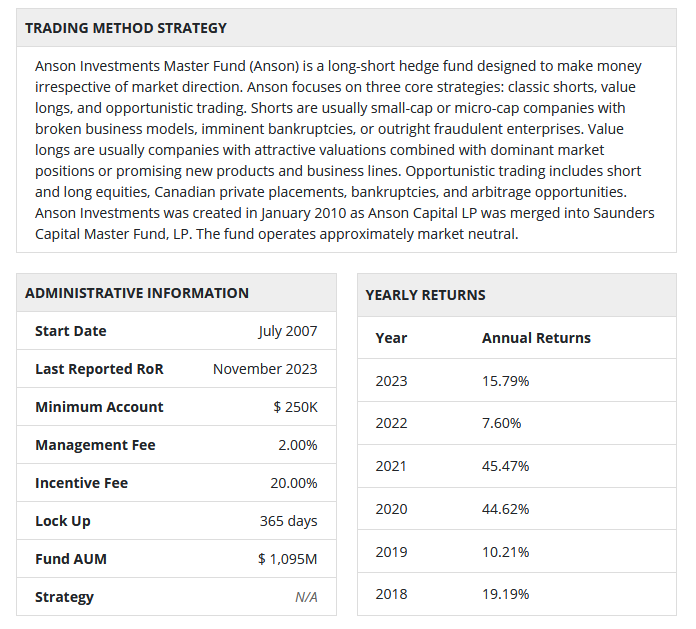

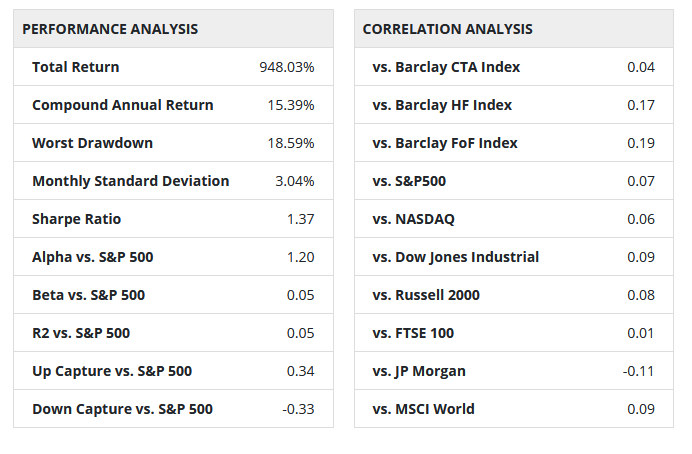

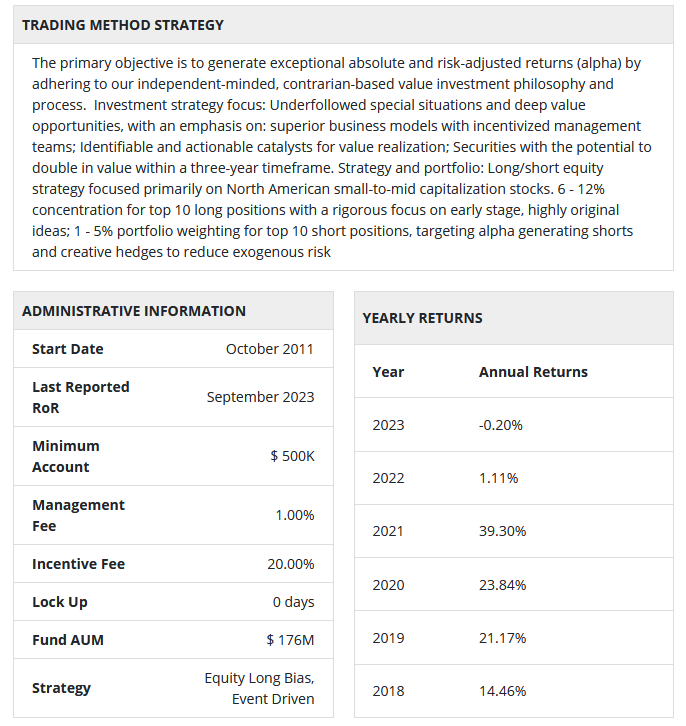

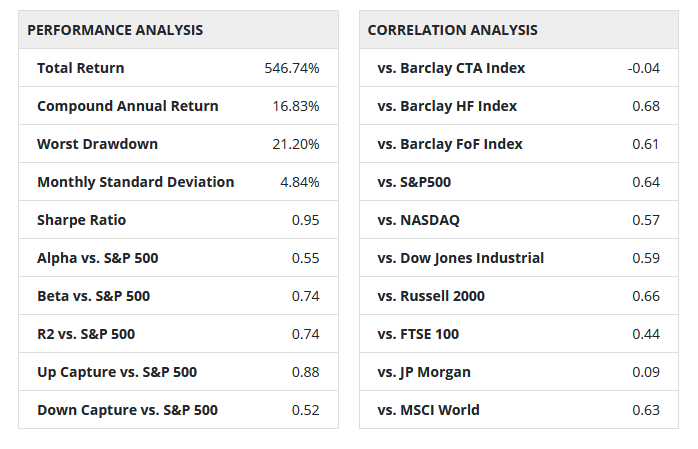

Here is the latest performance (that I have posted earlier) for two of the best performing long/short hedge fund in the past 5 years according to the top 50 performing hedge fund report.

Note that Anson Investment has an alpha of 1.2 vs S&P 500 and beta vs S&P 500 of 0.05 while Voss Capital Value has an alpha vs S&P 500 of 0.55 and a beta of 0.74 vs S&P 500.

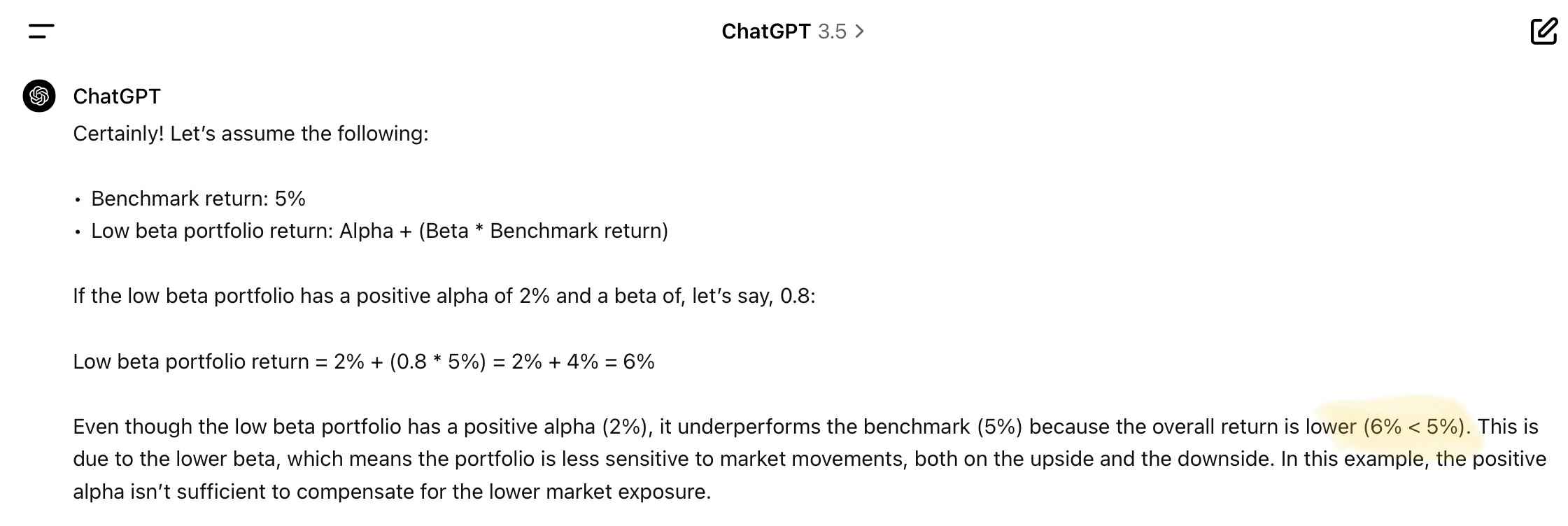

A user asked me how alpha can be positive and still underperform the benchmark. I explained, “The return of a portfolio is its beta times the market return plus its alpha. So if the beta is well below 1, then alpha can be very positive even if the portfolio return is less than the market return. For example, if the market return is 10% and the beta is 0.5, a portfolio return of 8% would have an alpha of 3%. Long-short strategies, if properly managed, almost always have much lower betas than long-only strategies.” That’s why I think using alpha to compare long-only and long-short strategies is sophistry. Long-short will almost always win. On the other hand, if “excess return” is the measure, that’s very different from alpha, and it’s not clear from your posts which is being used.

This from ChatGPT 4.0: “For calculating alpha, it’s beneficial for the benchmark to have a reasonable degree of correlation to the portfolio to ensure the comparison is meaningful. A good correlation might typically be in the range of 0.5 or higher, indicating a moderate to strong relationship. However, the specific number can vary depending on the investment strategy and the nature of the portfolio.”

Some of this may have been what Yuval is trying to say in different words. But at least in the extreme, I do not find that for market-neutral portfolios the alpha has anything to do with anything.