All,

Personally, I would like to see the backtest results. I am not for hiding information from people or censoring information.

I would like a lot of information about the backtest to be downloadable, in fact!!! I would like to bootstrap the results myself—especially if P123 does not end up doing that. I would run a Bayesian analysis knowing the result is not accurate without the discontinued models.

But people who think newbies might not understand and think that anything will perform as well out-of-sample could be misled are right about that I think.

I mention Yuval’s designer models because they are an example of good models. He has commented on the regression-toward-the-mean for his models. I will let Yuval quantify that or correct me if he does not think there is regression-toward-the-mean for his models.

But regression-toward-the-mean is a force of nature that we can do nothing about as humans (only slight hyperbole here). Actually, if you look at information theory (and entropy) it is not hyperbole at all. There are equations for this.

I do not even have to appeal to overfitting here.

Any professional financial advisor will show you a Monte Carlo simulation at least once (maybe so she does not get sued for false promises but I am not sure).

As a somewhat southern hick I want to say: “I do not have a dog in this fight.” I will not debate this much. But I do think bootstrapping is a great tool and is as good or better than Monte Carlo simulations. Better than Monte Carlo because of the assumption of normality for Monte Carlo simulations if nothing else.

I would consider adding a bootstrapped confidence interval if you continue to show backtests. Again, this (or Monte Carlo simulations) are established professional tools.

And a disclaimer along the lines: “Due to regression-toward-the-mean the designer model is expected to perform below historical returns and toward the lower confidence interval.”

This is, actually, a provable mathematical fact. Full stop. And there is no need to imply that the designer is overfitting in any way.

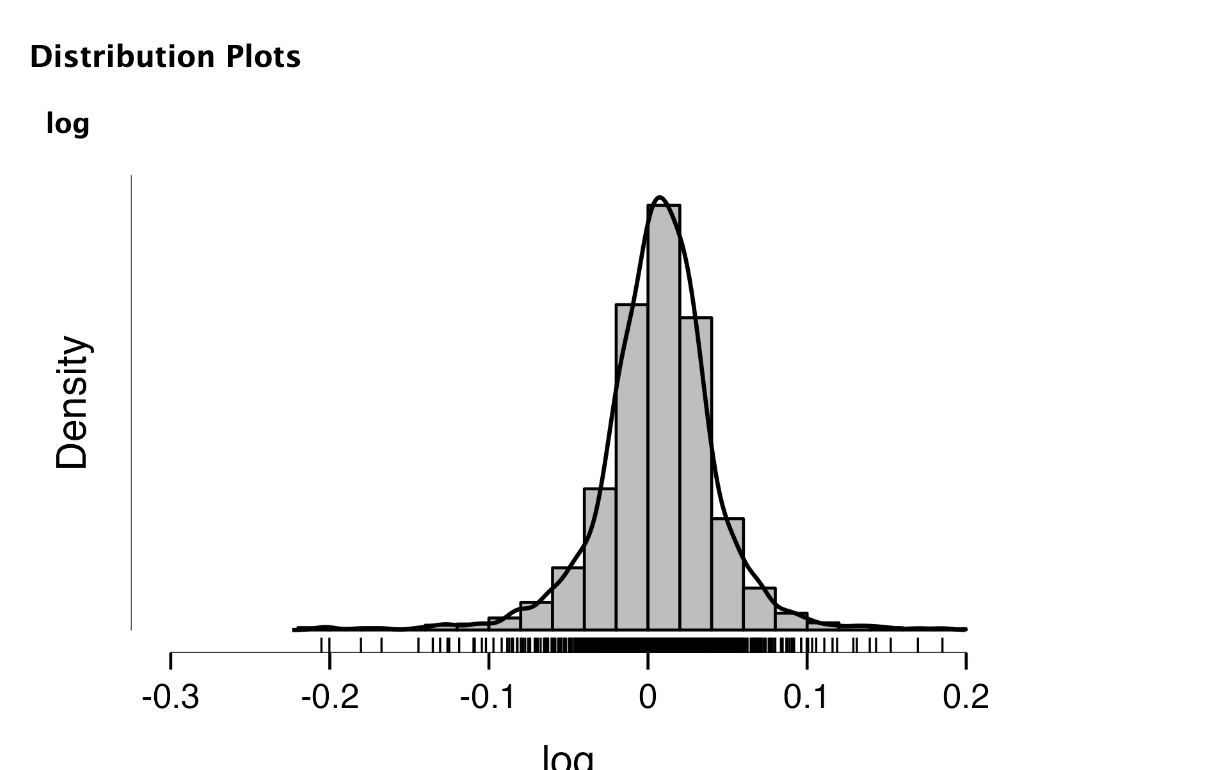

Using my sim/port as an example, I have redone the above a little using log returns (and is a little better but not perfect yet). If it were a designer model the backtest would show about 42% annualized return.

The lower bound of the 99% confidence interval is 22% annualized return.

Put simply, I think it would be wrong to suggest to a buyer that it would perform better than 22% annualized return. If it does do better then sue me.

But any implication that it might perform as well as the backtest would be just short of a lie most of the time. I guess anything is possible but that is not likely.

BTW, as per Walter’s request for a distribution. Fat tails, I think (something favoring bootstrapping over Monte Carlo):

Jim