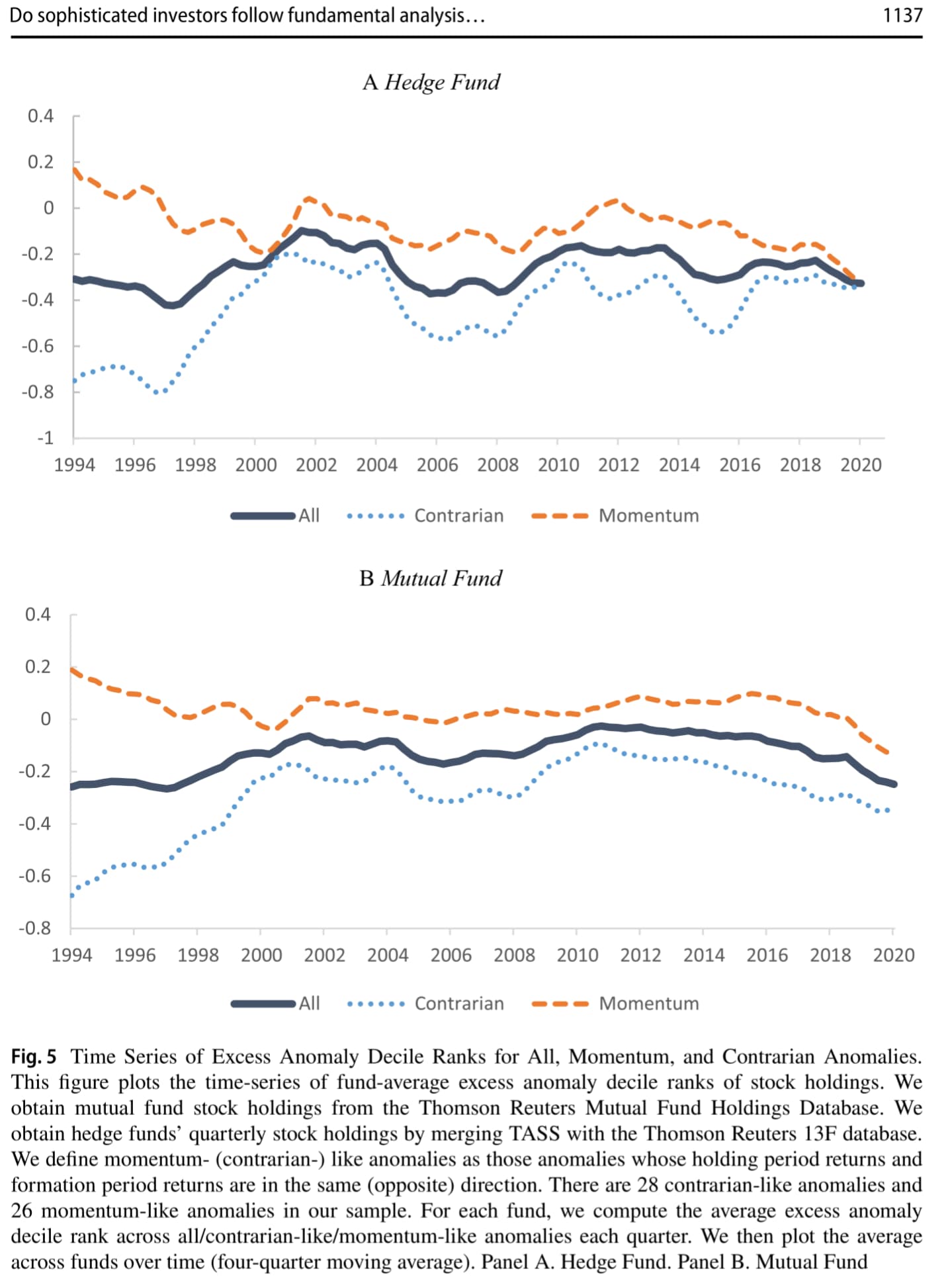

Using fund returns and fund stockholdings, we investigate whether fund managers follow fundamental analysis strategies. We show that hedge fund and mutual fund returns tend to load negatively on the long-short returns of a comprehensive sample of fundamental strategies (i.e., accounting anomalies), suggesting that fund managers are prone to trade in the opposite direction of what fundamental strategies prescribe. The negative loadings are primarily driven by the short-leg of the anomalies, more pronounced for contrarian-like anomalies, and more prevalent among earnings quality, investment, external financing, value, and profitability-based anomalies.

Yuval was correct. Good stocks aren't loved by most hedge funds.