Here’s the article on this topic I posted to the blog site:

https://p123blog.com/2018/06/21/my-investment-model-recommends-that-what-the/

Here’s the article on this topic I posted to the blog site:

https://p123blog.com/2018/06/21/my-investment-model-recommends-that-what-the/

I use the defaults; next open, 0.25% slippage.

Marc, I am to lazy to replicate your nano / small cap screen of https://p123blog.com/2018/06/18/understanding...ng-potentially-good-ones/ (the one that works), could you provide a link to it? That would be great, thank you

Andreas

I would like to add more2 cents.

In order to be 100% mechanical, e.g. following your system 100%, something helped me.

Look at your portfolio as something that lives (a living entity that you create) and that is a casino that roles the dice

every day times the amount of stocks you have in that portfolio. on an individual

stock base I will be wrong all the time, even with the winners (because I did not buy at the low

and sell at the high). The same is a casino that you own, you will loose a lot of bets.

But that is not what counts, your overall performance counts.

What I do is also, I post all my stocks (100 because of the casino effect and the lower volatility I get) into tradestation and sort them by winners descending. Usually I got a lot of stocks posting >5 or >10 Percent. I love that, and the Loosers I have at that

day do not bother me anymore, because I know they are offset by the winners.

Good advice.

At the end of the day, it is all probabilities anyway.

Through proper modeling, we are just trying to increase our probability of success while knowing that sometimes it will go the other way.

Here’s the link to the screen.

https://www.portfolio123.com/app/screen/summary/210015?st=0&mt=1

The name of it is

VQS Micro-Nano Cap Stocks from p123spotlight.com

That is the essence of having a portfolio as opposed to a stock.

We all can recite the theory of diversification. But to make it real, one has to get comfortable with the mindset Andreas suggested.

Hi Marc,

There’s something off when I backtest a copy of ‘VQS Micro-Nano Cap Stocks from p123spotlight.com’.

A copy and sim shows an AR of 17.07%. But I noticed that under settings, ranking is enabled but unassigned. When I disable ranking, the AR drops to 7.88%.

Does this screen use a ranking system (under settings)?

Walter

Yes, you need to set ranking as the default P123 sentiment (basic: sentiment). That worked for me.

Rod

Thank you Marc!

Thanks Rod.

On another thread, David used Marc’s P123QVS ranker. That seems to provide identical results to the direct copy of the screen. I don’t know how or why the copy had the ranking system unassigned. I p123 bug, perhaps?

Walter

I have purely mechanical models and purely discretionary picks, and never mix the two.

Once I trust a model, I trust every stock pick from that model. It is always going to follow the rules and pick the type of stock you told it to.

As I recall, someone did a study that showed that newsletter subscribers under perform the newsletter, because they go in and accept/reject the picks on a discretionary basis, basically undoing the newsletter. I think Joel Greenblatt said something similar about his magic formula investing.

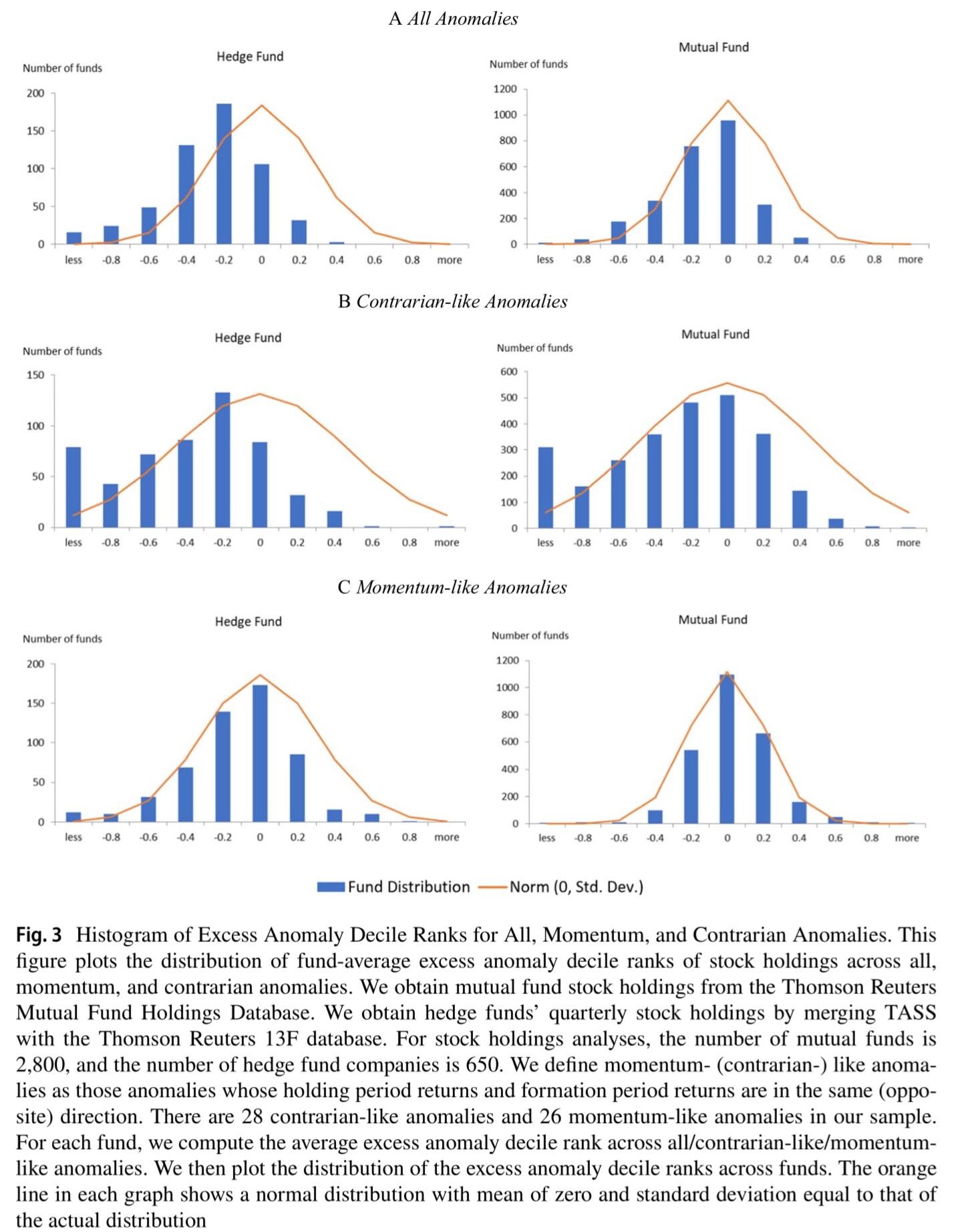

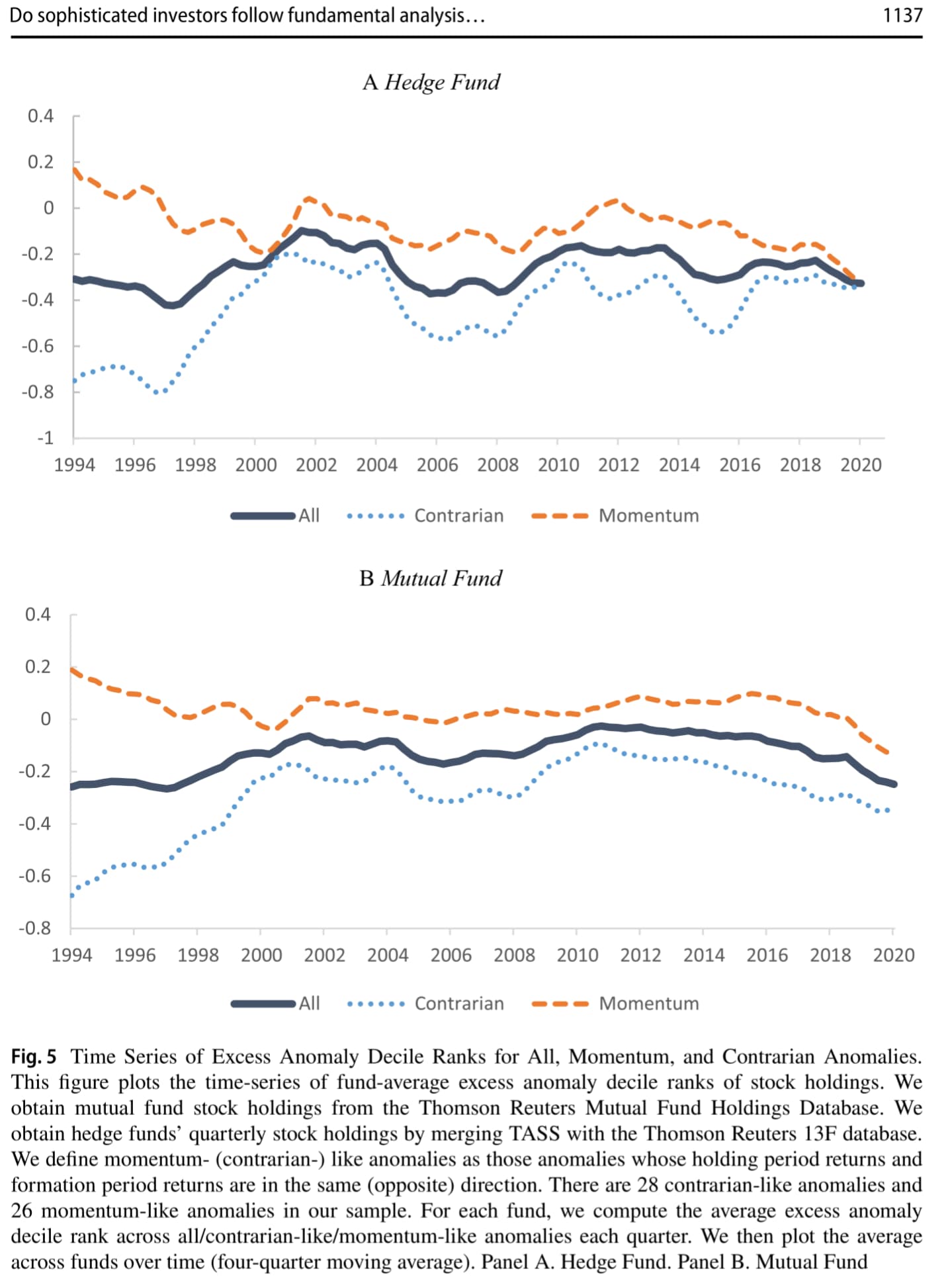

Using fund returns and fund stockholdings, we investigate whether fund managers follow fundamental analysis strategies. We show that hedge fund and mutual fund returns tend to load negatively on the long-short returns of a comprehensive sample of fundamental strategies (i.e., accounting anomalies), suggesting that fund managers are prone to trade in the opposite direction of what fundamental strategies prescribe. The negative loadings are primarily driven by the short-leg of the anomalies, more pronounced for contrarian-like anomalies, and more prevalent among earnings quality, investment, external financing, value, and profitability-based anomalies.

Yuval was correct. Good stocks aren't loved by most hedge funds.

Well unironically, that's exactly why these companies are highly profitable, have higher growth prospects and high shareholder returns.

Pollution is your friend.

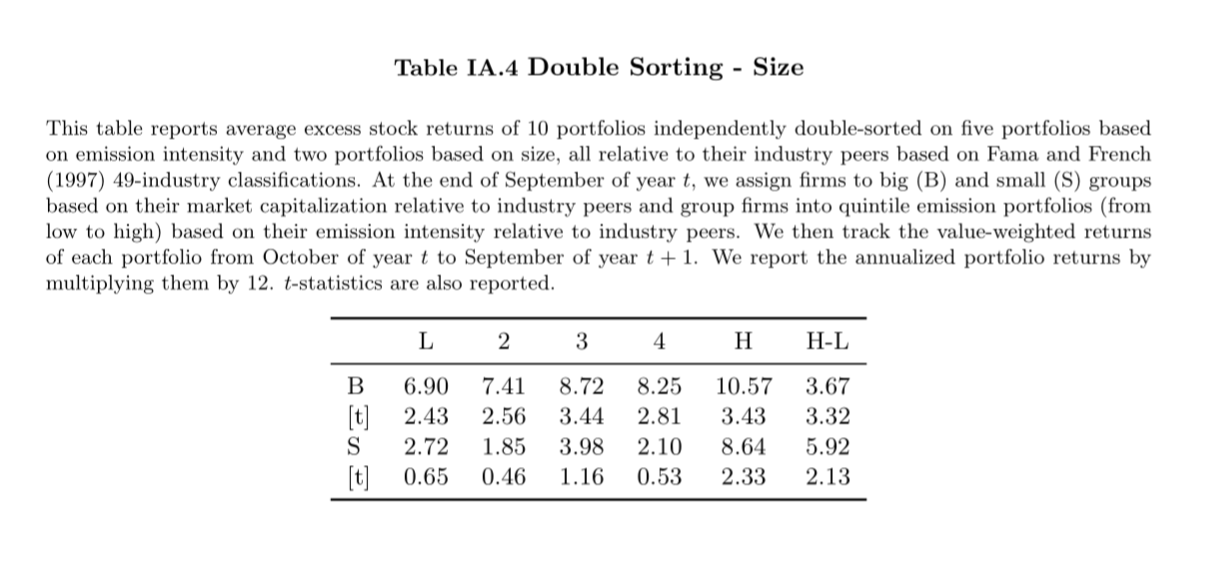

This paper studies the asset pricing implications of industrial pollution. A long-short portfolio constructed from firms with high versus low toxic emission intensity within a given industry generates an average return of 4.42% per annum, which remains significant after controlling for risk factors.

Maybe the real intangible value is the bad things we did along the way

Sin pays.

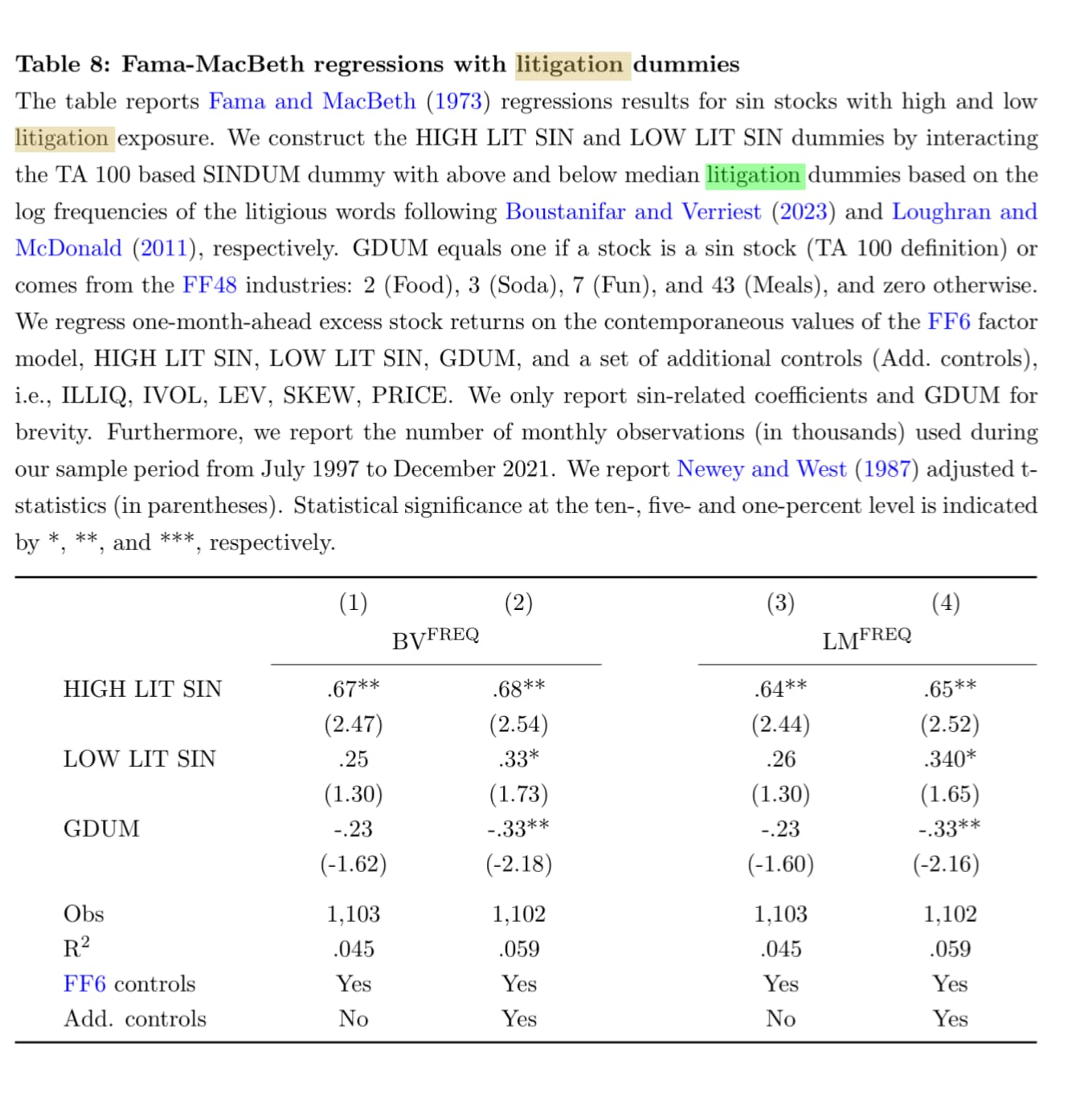

The existing literature identifies sin companies using industry classification codes (IC). We propose an alternative continuous measure of firms’ exposure to sin activities (sinfulness) based on textual analysis (TA). Sinfulness captures nicely both cross-sectional and time-series variation in firms’ exposure to sin activities. TA reveals several important false positive and numerous false negative sin stocks in IC. Neither equal- nor value-weighted portfolios of sin stocks show abnormal returns. However, a sinfulness-weighted portfolio earns an annualized alpha of 5%.

The Secret Ingredient Is Crime.