All,

Thank you for your comments. Much to consider. Thanks especially to “Joe” and others like him who show that it can be done, despite the difficulty,

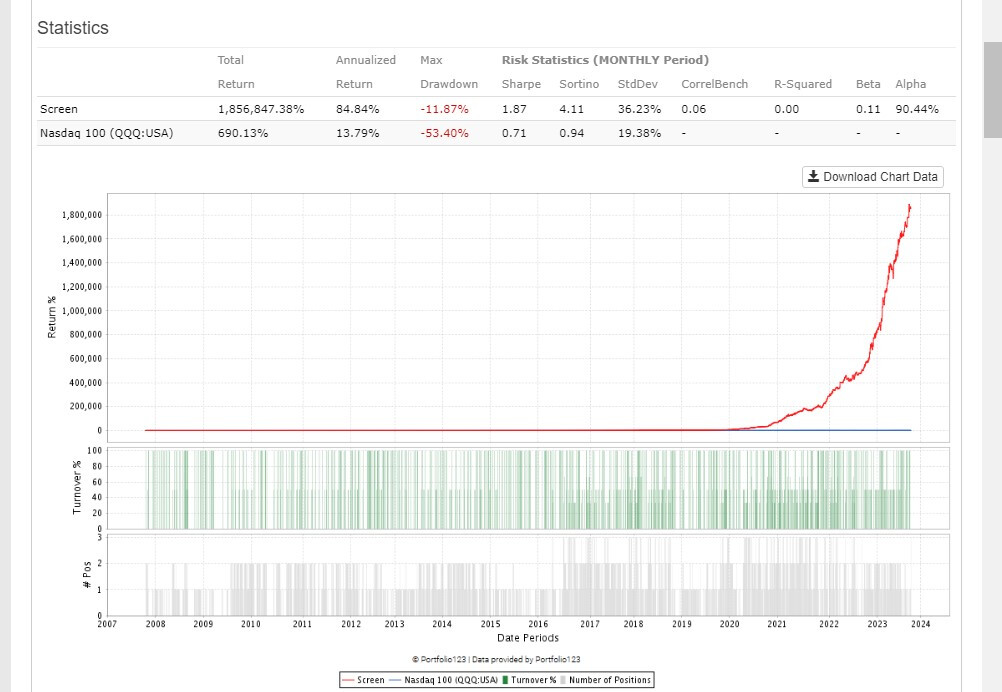

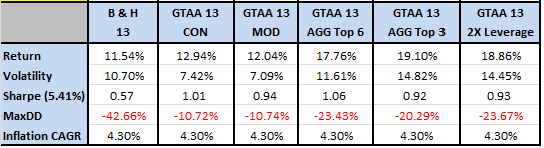

As for Meb Faber’s GTAA 13 Aggressive 3 and 6 versions, I don’t think of them as market timing. After all, the universe of 13 investable assets are ETFs representing different classes, some US based, some foreign based, some representing stocks, others commodities, etc. (See “A Quantitative Approach to Tactical Asset Allocation”, SSRN-id962461, https://mebfaber.com/wp-content/uploads/2016/05/SSRN-id962461.pdf ). For some of the strategies outlined, they are buy-and-hope and rebalance. Others, though, such as the Aggressive 3 and Aggressive 6, attempts to select the best performing 3 (6) ETFs using a momentum only strategy, namely as ranked by the average of 1, 3, 6, and 12 month momentums (p. 50). Here is a snippet of “Figure 20: Buy & Hold vs. Various GTAA Allocations, 1973-2012”, p. 52:

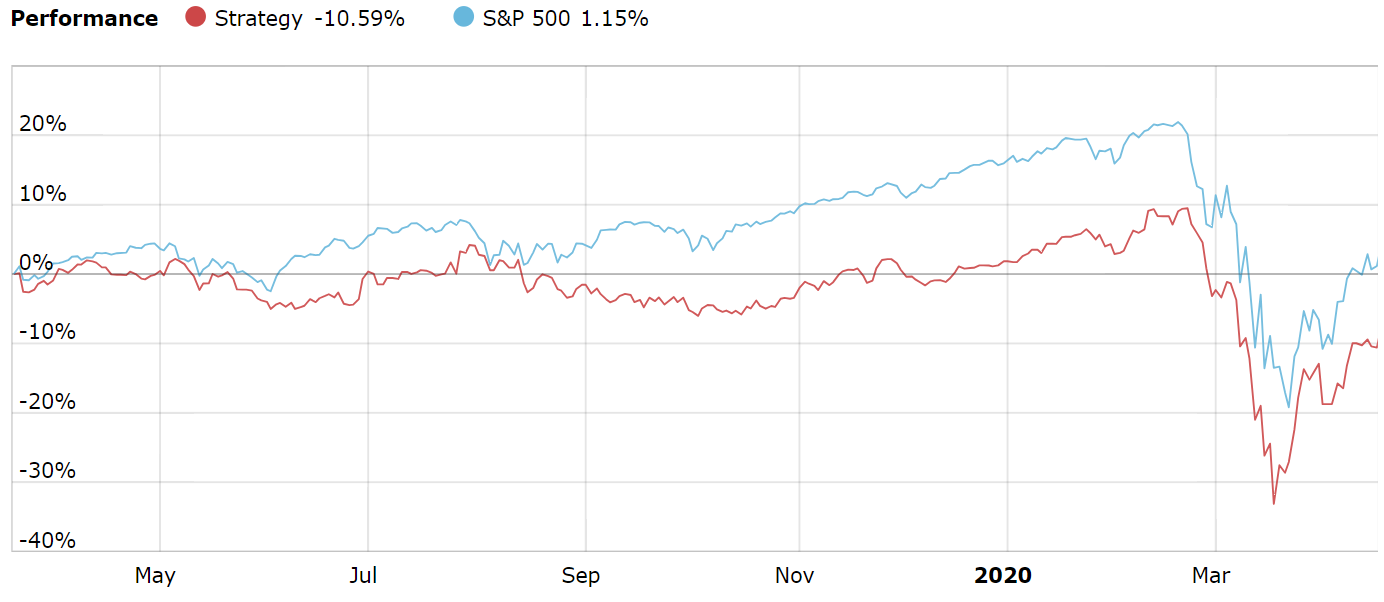

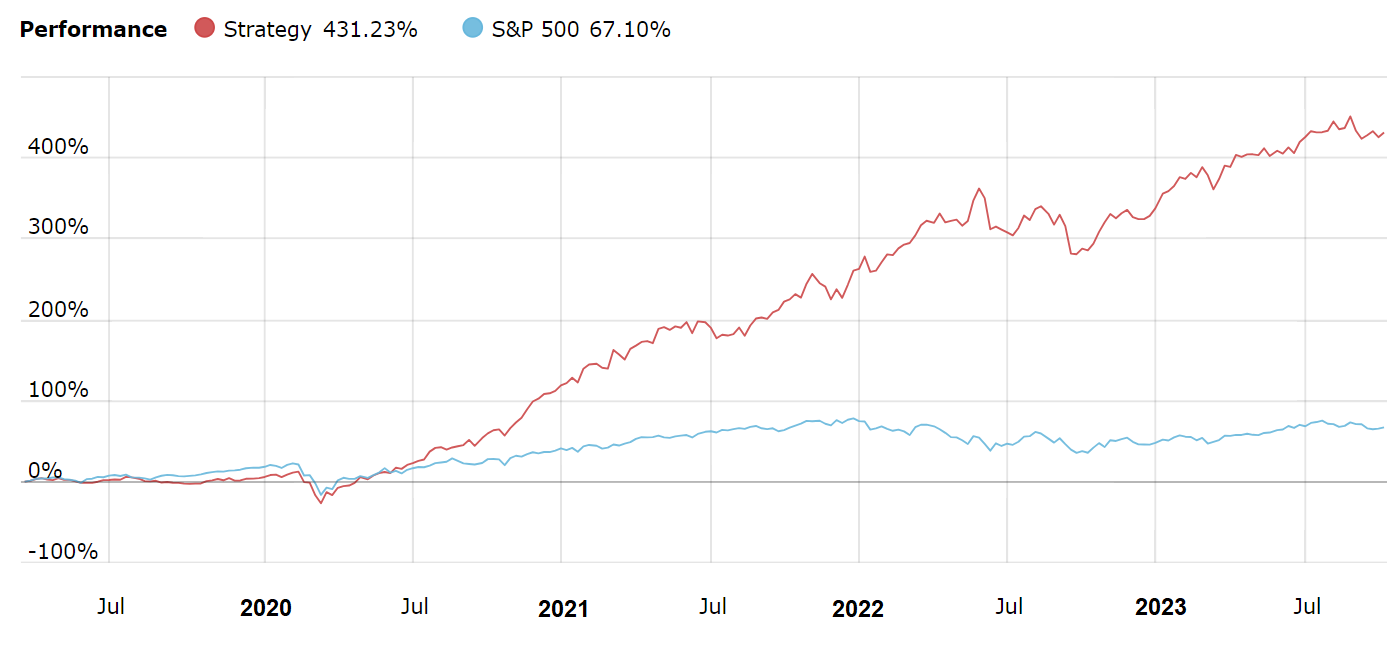

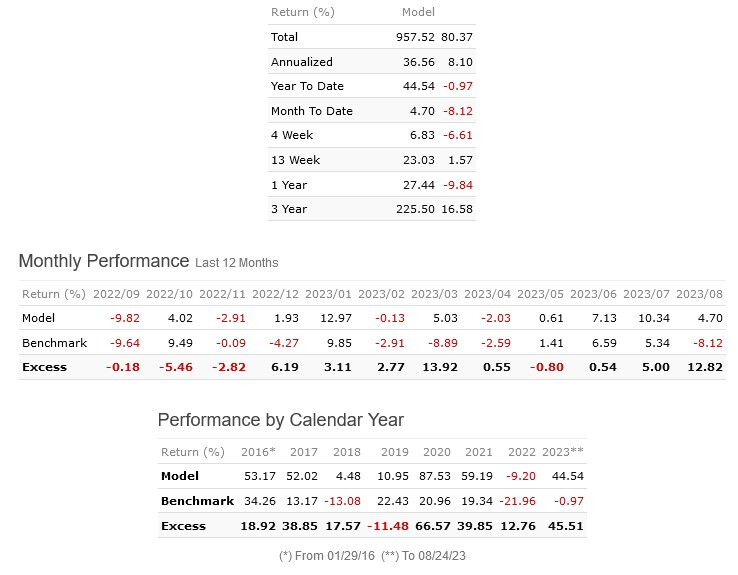

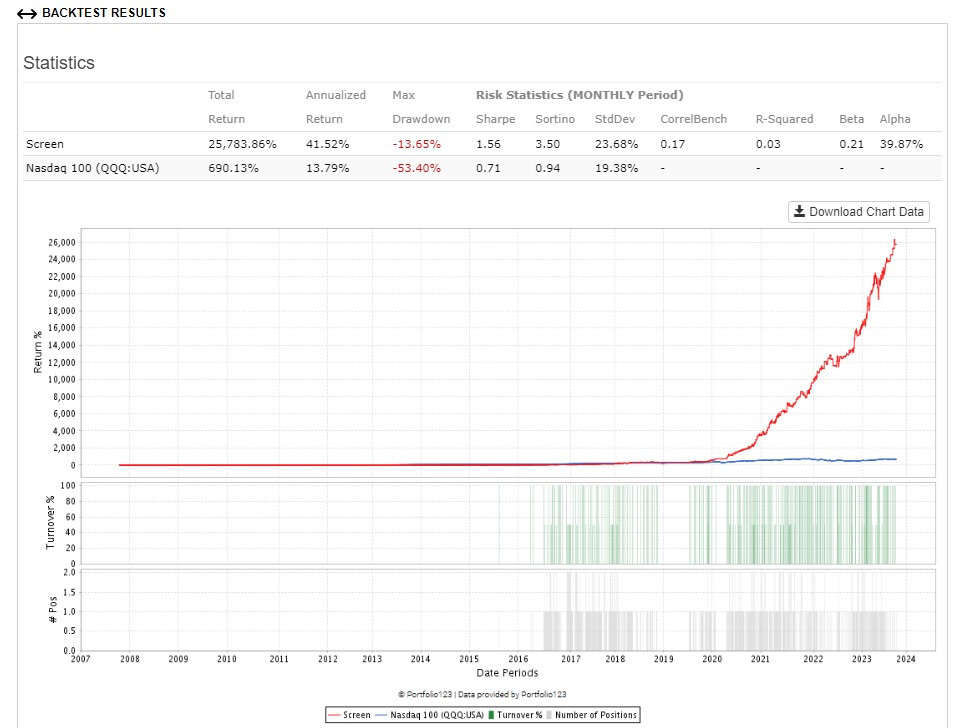

So through 2012, the total performance (CAGR) of GTAA 13 AGG 6 and AGG 3 were far better than S&P 500. So I tried to duplicate the results in P123. Because of my membership restricts me to going back 20 years from my join date (April 2022), then I could measure the performance over that period. Here is what I got for AGG 3 for 01/02/2002 … 12/31/2008:

CAGR: 11.07%, Annual turnover: 286.20%, Max drawdown: -25.33%, Sharpe: 0.59.

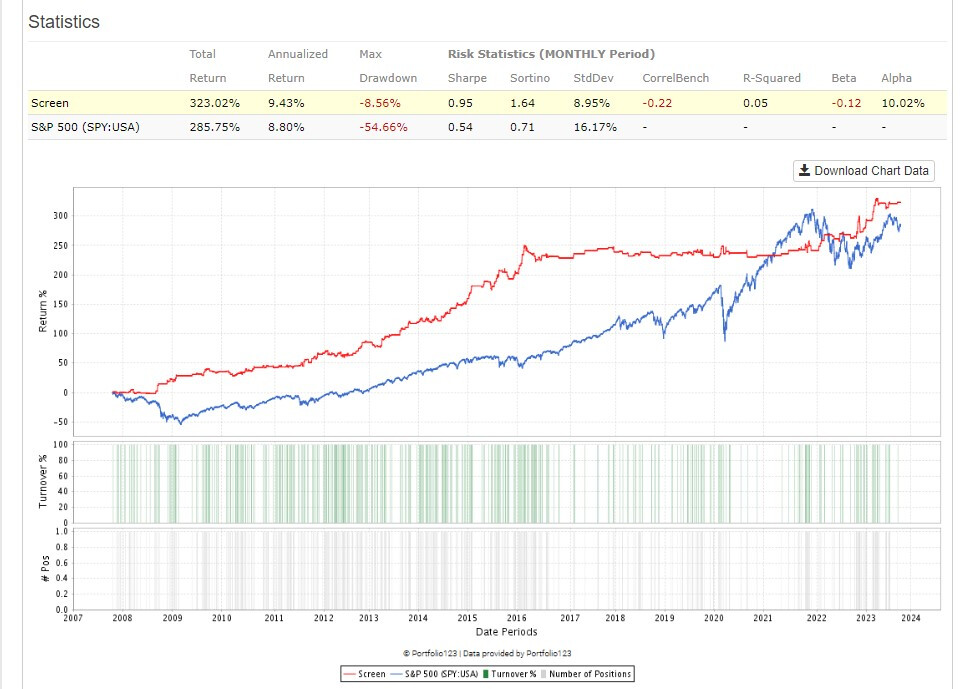

Not like the performance in Figure 20 of Meb Faber’s Figure 20, but still better than the S&P 500. But I then ran the AGG 3 system from 01/02/2009 … 12/31/2002. Here is what I got:

CAGR: 5.29%, Annual turnover: 426.19%, Max drawdown: -43.11%, 0.46.

The performance of the strategy was better than the S&P 500 until about 01/02/2015, and then it started downtrending, losing money.

Prior to coming to P123 I signed up with AllocateSmartly.com, a system that offers many different ETF strategies, from different forms of buy-and-hope such as the Permanent Portfolio, to different tactical asset allocation strategies. The first 2 strategies I signed up for was the Adaptive Asset Allocation (see Adaptive Asset Allocation - Allocate Smartly ) and the Vigilant Asset Allocation (see Vigilant Asset Allocation from Dr. Wouter Keller and JW Keuning - Allocate Smartly ). At the time they were among the best performing strategies. I followed them for 2 years, and both years they badly trailed the S&P 500.

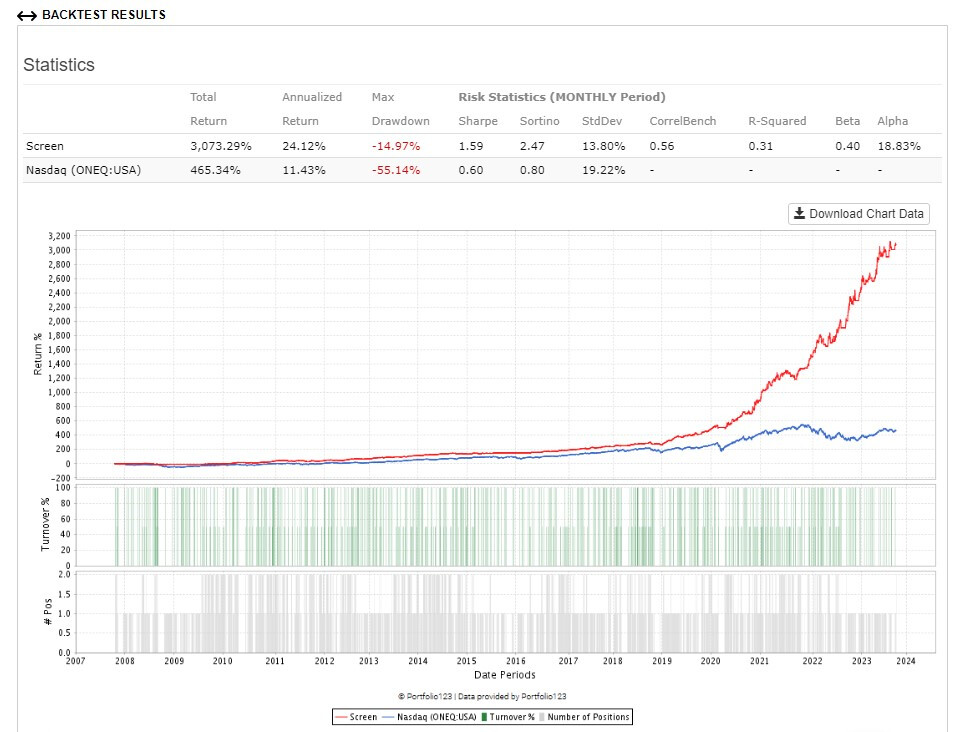

I am beginning to wonder if there is any ETF strategy that beats buy-and-hope. Looking at the designer models on P123 for those strategies that have been in existence for 5 years or more, almost all of them have terrible 3-year and 5-year returns. So perhaps investing in ETFs is not a promising approach.

Comments?

Cary