I think the market is temporarily oversold. This morning I sold some covered calls to take advantage of the higher implied volatilities. Hopefully the time decay and decreasing volatilities will work to my advantage.

Walter

I think the market is temporarily oversold. This morning I sold some covered calls to take advantage of the higher implied volatilities. Hopefully the time decay and decreasing volatilities will work to my advantage.

Walter

More info on the historic the 4+ deviations away from the S&P500 50 day moving average. This time the comparison is 1940.

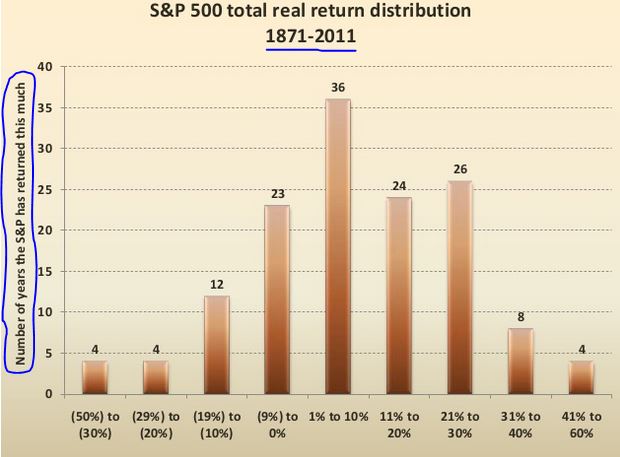

ImmanRoshi - What they aren’t telling you is that volatility is extremely low to begin with, thus using standard deviations as a measuring stick doesn’t make sense. This sell-off doesn’t even come close to 1987, 2001 or 2008. These talking heads have either never been through a bear market or they have some hidden agenda.

The real question is what happens now? Is the bounce the start of an uptrend or a head fake? One “rule of thumb” suggests that markets don’t bottom in August. But only time will tell.

Steve

I do not know if this was it, but standard dev is based on normal distribution curve and stocks do not fit to this, stock distributions have

long tails (and very low vola follows very high vola) and therfore has more black swans effect then standard dev seems to be able to predict.

That is the reason why shorting options models (45 Degree capital curve until you get bust) or using any leverage (in general) is a bad idea and I think LTCM got bust because there risk models based on

the Assumtion of a normal distribution curve of stocks and other financial instruments.

The other part of argumentation of Pisani though is good (especially for todays rally), also Jerry Wagner Comment.

Regards

Andreas

We must have hit a bottom. All of the financial web sites now feature photos of floor traders with smiling faces. All must be well. ![]()

Andreas - Here is what Pisani said yesterday: “The problem is, when there are true fundamental issues, you can stay very oversold for a long time.”

http://www.cnbc.com/2015/08/25/heres-the-new-factor-causing-problems-for-the-markets.html

It seems to me he is just another talking head swaying in the wind.

The truth be known, instead of saying we have a very rare event (or “historic event” as some other talking heads have worded it), they could just as easily have said that we have emerged from a period of historically low volatility, at least for a brief period of time. But I guess that is a lot less sensational ![]()

Steve

Steve you are right!

Okay to make it official:

I changed my hedge from short VWO on tuesday to short SPY, because I was afraid emerging markets would Rally harder then US Markets.

I am Back Short VWO, since it had a nice bounce.

Reasoning:

300k Hedge Short on VWO (with 300k small caps Long) because earnings specsy drift down (I could go flat, but where is the fun in that).

Hedge with VWO because Emerging markets are in bad shape (Dollar strength, Carry trades Need to be unwind and sooner or later

the fed has to rise, e.g. more Dollar strength.

So I hope now US small cap do better then emerging markets, and I can squese out some Alpha out of this.

Regards

Andreas

Very true…this graphic might help frame the discussion (source: What makes us bad investors? | PPT )

Cheers, Motu

Somebody mentioned the performance of value stocks. I bring here some remarks I made at Seeking Alpha, maybe they could be helpful.

Value has been under performing growth on a consistent basis over the last few years. The combination of value and quality somewhat alleviates that down performance as it allows you to pinpoint those stocks that are being punished without much of a reason. But value itself is being dismal.

Such down performance over the last few years has a lot to do with the low interest rates environment. Equity markets sell earnings growth and the low growth environment we have witnessed these years has made growth companies more attractive and, hence, money has pursued them.

Also, value metrics dispersion is reduced at market tops. That’s why it becomes increasingly harder to ride multiples expansion, which is the biggest reason of out performance for value stocks. I tend to think about this as a spring. The amount of energy contained in the spring when value metrics dispersion is bigger is higher and then value tends to outperform. It’s pretty obvious that’s not the case in this market. P123 provides you with tools to assess exactly this.

The fact that growth has been outperforming during the last years lends itself to a quite brutal reversal. It’s consistently happened along history and will take place once again. Most of the returns to be made over the next years will take place in the short side shorting expensive growth low quality of fundamentals stocks.

A market top is far from the point where one should try to outperform the market. Market tops are akin to when young people run their cars towards a cliff to prove manhood. Those are the moments when risk is higher as prices are too elevated and the risk/reward ratio reaches its worst point in the investment cycle.

I would not be much concerned about the track record over a few months and would not raise an issue because of that. Value tends to outperform growth over periods that span decades. Anomalies can persist over six months, eighteen months, thirty six months and even sixty months. It’s not unheard of.

The reason why I still believe value to beat growth over the long term is due to behavioral biases. I do believe that value investing is the only discipline that works over the long term as its foundations are rooted in human beings flaws and those do not tend to change over time.

I am sure this must have been debated before but I am honestly curious about this. I recall that somewhere in the forums it was explained but, whatever, here it goes: how is the blended estimates number calculated? I ask this because both CY and NY are going down and the blended combination is displayed as going up.

Mí no entender.

¡Gracias!

Jose,

See https://www.portfolio123.com/doc/doc_detail.jsp?factor=%23SPEPSCNY&popUpFullDesc=1

de nada (Is that correct Spanish?)

The SMI Indicator for China and some other European Countries went below 50 yesterday (= Contraction!), the sell off did not wait for Long.

Bad News wack the market, good News do not matter. The Sentiment is clearly negative.

Momentum Stocks (even NFLX) loose Leadership.

3 of 4 Earnings Indexes (for example Specsy) trend down.

Buy Rule

(close(0,#SPEPSCY)>ema(10,0,#SPEPSCY)) or (close(0,#bench)>ema(75,0,#bench))

Sell rule

(close(0,#SPEPSCY)<ma(10,0,#SPEPSCY)) or (close(0,#bench)<ma(75,0,#bench))

Emergin0 Markets have rolled over some months ago and lead the pace down…

Far more reasons to be out of the market then to hope to make Money…

Regards

Andreas

…Also earnings estimates: “Waiting for that data-point of the 3rd Quater” I hear a lot.

This “will then decide where the market is headed”.

If earnings start to trend clearer down, it is going to be very ugly in this Environment (= Bear Market)

If they suprise, it might be a hick up of - 10 - 15%

Regards

Andreas

Andreas - the problem is that companies tend to use this type of market to write off the skeletons in the closet, as they have an excuse to clean house while blaming it on China. It is a “get out of jail free card” as one would say in monopoly. I would not be surprised at all to see lower earnings.

Steve

For those interested, I have published Part 1 and 2 of a 3-part series titled, “Where is the Market Headed From Here?”

Part 1, posted on Aug 24, covered the following topics:

In Part 2 of the series, published tonight, I cover the following topics:

In Part 3 of this series, I will discuss the 1) risk of deflation in the world and US economy, 2) how central banks are losing control, 3) the threat of currency devaluation, and on a positive note, 4) the fact that there are no signs of an imminent recession in the US at this time. Also, I’ll discuss the positive benefits of a market collapse (yes, there are several).

These articles, like all of my Intelligent Value Alert newsletters, are now free to the public. I have also made our most recent, proprietary Intelligent Market Risk Analysis (IMRA) from the Member’s area available to the public. This page summarizes the technical aspects of the markets and helps determine our exposure. This system told us to ease out of the market starting back in late June, avoiding the downturn entirely. We now hold 100% cash and are ready to deploy it, perhaps as soon as this weekend, in the appopriate investments.

I invite constructive criticism. Enjoy!

Chris,

Cheers! I enjoyed both of your articles. I look forward to the third installment. Keep them coming. It was also encouraging to see the 8-year chart with the S&P uptrend and your analysis that the uptrend is still intact. Do you beleive we have seen the bottom, at least for now?

Unfortunatly, I was unable to access this section of your web site. It required a password.

Es perfecto, tanto el link como la respuesta. ¡Gracias!

(It’s perfect; both the link and the answer. Thanks!)

Anybody watching the general market ?

Something we can learn from the current rapid down move?

Timing rules? Formulas?

I think one of the most timing-rules-reelvantthings I’m learning, from the latest declines and others, is that the extreme institutionalization and technological-ization (Is that a word?) of the market is changing the game. More and more money is moving pretty much at the same time in response to fewer and fewer (human and/or automated) decision makers. That’s why I, once an advocate of market timing (something those ho joined p123 lately and didn’t see my posts from years back) turned very sour on the practice.

Speed and concentrated decision making are not an obstacle when the declines are tied to objective fundamentals (hence the reason why the standard SP estimates-based timing rules worked in 2001 and 2008). But haven’t and can’t work when the declines stem from sentiment and/or anticipation of not-yet-objective but-widely anticipated fundamentals.

That’s why two R23G models I recently introduced are addressed to risk. I don’t think we can time the market, but I do think we can do good things to position ourselves to withstand what happens.

The combination based on facts, not forecasts, works very well for me. I don’t believe in economic forecasting.

I am using a combination of different momentum, trend, vola, and fundamental models here on P123 all with different variations. 8/12 models timed the market down-turn correctly. Only 2 out of 12 are still fully invested in equities which are an unemployment-based model, and the other a S&P 500 EPS model (will soon flag risk-off market). Overall, the book is only 35% long equities (net of short ETF), 35% bonds/rates, 5% other alternative ETF, remainder cash (if long & short ETFs are netted out).