David,

The reason I posted is that I am an ignoramus and trying to learn. You saw the results of my first bootstrap.

From Wikipedia: “In statistics, bootstrapping is any test or metric that relies on random sampling with replacement.”

And: " It is often used as an alternative to statistical inference based on the assumption of a parametric model when that assumption is in doubt, or where parametric inference is impossible or requires complicated formulas for the calculation of standard errors."

So it does not assume normality. It does assume i.i.d. however.

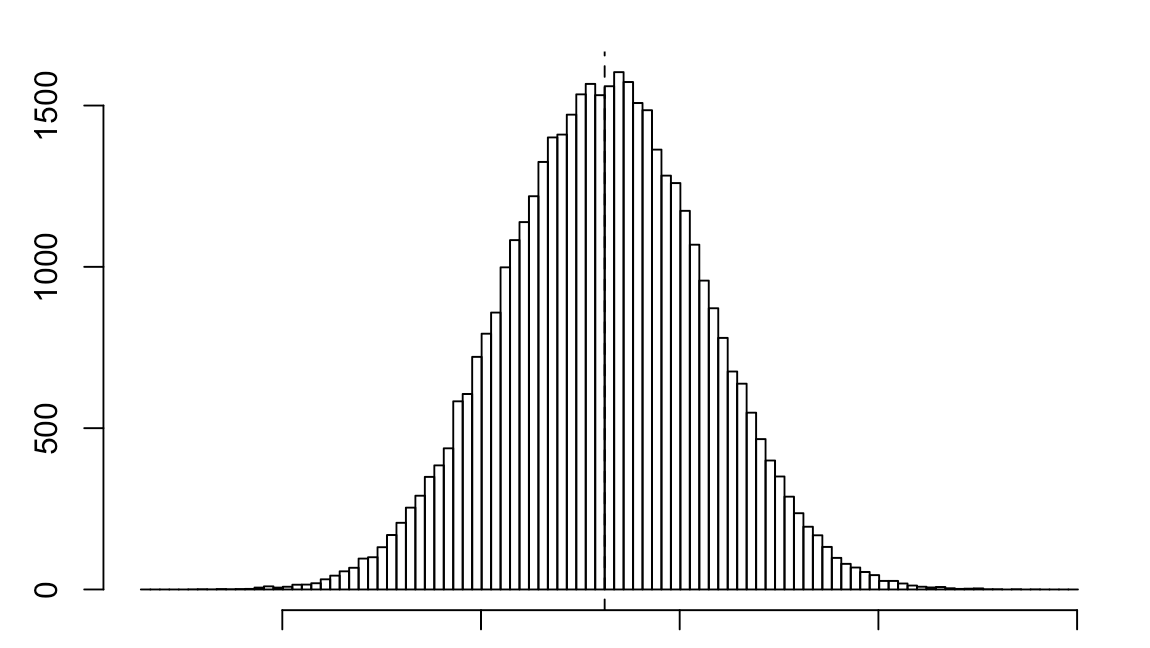

I am not sure Wikepedia is too clear. It takes the data and randomly selects one of the days returns and replaces it. So it is sampling with replacement. You keep it up until you have done it the number of times equal to your original sample: Max days for P123 in this case. Then repeat for a total of 5,000 resampled means in this test—which is the number that Aronson uses in his book.

I do not pretend to fully understand. And I certainly cannot do justice to David R. Aronson’s book: highly recommended for a clear explanation of this.

Truly looking for improvements on my technique.

One thing I did learn. They say it is very computer intensive. In a sense it is. It drew over one billion days in one of my subsequent runs: trying to get wider confidence intervals and thus a greater p-value for a mean excess return greater than zero. But on my MacBook it took about 40 minutes.

And, I thought my MacBook might take off as fast as the fan was going.

But it did it. And that was worth seeing.

Did it tell me anything different that a t-test. No actually, and that is something I definitely learned.

-Jim