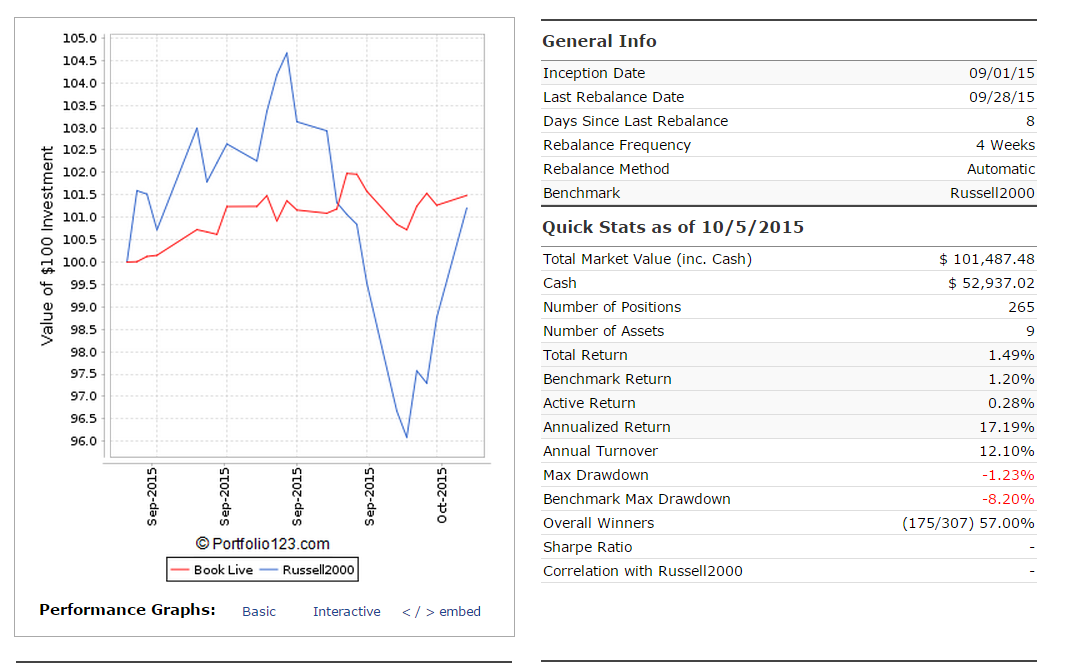

yury - I prepared an unhedged book simulation here: https://www.portfolio123.com/port_summary.jsp?portid=1385660

I would like to address some of your points.

“It doesn’t show consistency with sim performance.”

If you have read any of my past posts you will know that I have never claimed that OOS should compare with backtest simulation. My backtests are “optimized”, OOS is of course not. I am perhaps the only person making this statement, and I have been severely criticized for it, although I estimate 99% of R2G providers optimize their backtests, some to extreme levels. It is not “wrong” to optimize one’s backtest, it is only wrong that P123 presents backtest as “performance”, as it is not. Is it a bad thing that OOS does not show the same performance as backtest? Absolutely not. What is important is that the development process, which includes optimized backtest, has extracted some level of alpha.

“But out-of-sample alpha that I’m looking for is only 2%-6%.”

My first question for you is how much experience do you have trading the markets? Clearly you have some knowledge but knowledge doesn’t translate to experience. Some of the statements you make seem to be naive. For example “and at least zero ret (without market timing 1999-2015)”. Without market timing I doubt you will ever get OOS with no negative return years. And some years you won’t beat the benchmark. This is life. To address your point regarding performance, ANY alpha for largecap systems is an achievement. This is not to say there are not issues with my models, and will be addressed over time. I am mostly waiting for the new R2G to come out, it seems to be taking an eternity.

“There are four sources of returns (risk/return decomposition)”

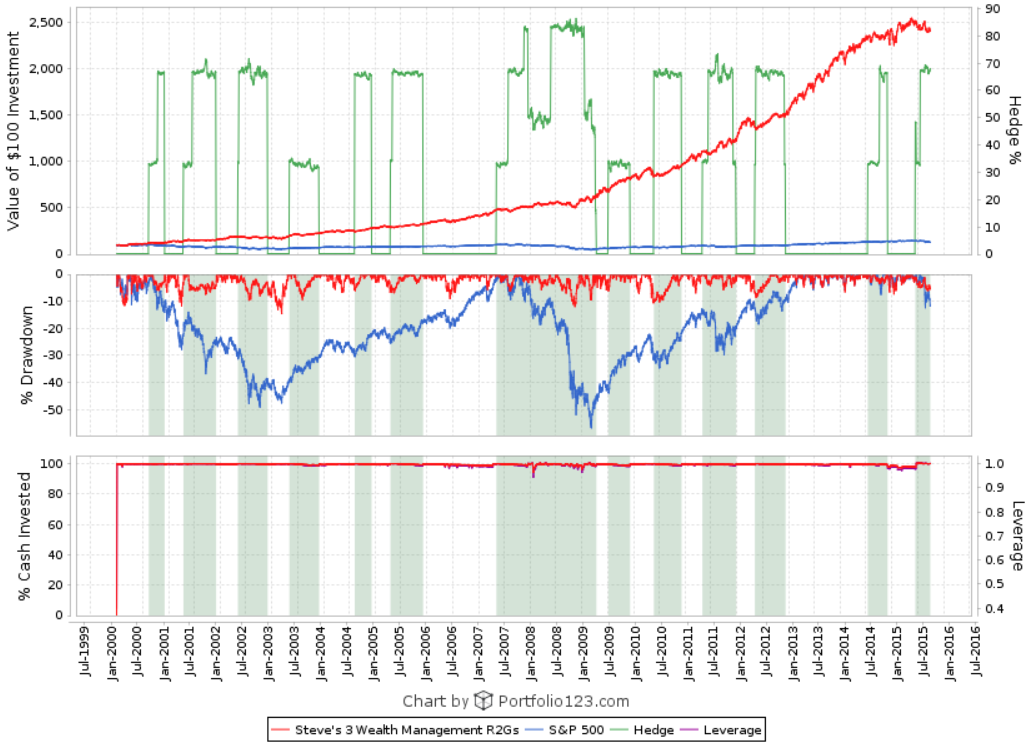

So your assessment of sources of return is very impressive. However, this pertains to the individual port (model) level. When considering Books, it is a completely one-dimensional argument. The fifth source of alpha is diversification from multiple independent strategies. Use of differing hedges with differing market timing, if done correctly, is an advantage over one model or three models with no market timing.

"I think you can make very good forward working models assuming that it would be designed not for R2G purposes (I mean an obligation to show good simulated results for the past 16 years to the detriment of the future performance "

I have been arguing this for a long, long time. However, don’t make the assumption that the market timing for three models is strictly there to impress people. As you pointed out, the OOS results are better with the market timing than without. And this is with Gold and TLT, neither of which makes a great investment vehicle at this time. I use these because P123 doesn’t provide other ETFs as alternatives (such as currencies).

Take care

Steve