Denny and Peter (and also Fred Piard), thanks for the fast response, appreciate it.

There are four sources of returns (risk/return decomposition):

-

Beta - market exposure (cap weighted)

-

Smart beta - factor indexes (value, quality, size, or momentum etc) in the middle of active/passive approach. New thing on the investment market.

-

Exotic beta - catastrophe insurance, event-driven, arbitrage, short volatility, destressed etc. Compensation earned by investors for taking exposure to non-market risks or for providing liquidity. Very high Sharpe for stable market conditions and disastrous in other case.

-

True alpha. Limited and very valuable. Idiosyncratic risk.

A) Security selection. In our case stock picking.

B) Beta timing or smart beta timing (market timing in other words).

So now I’m looking for point 4A in our P123 universe.

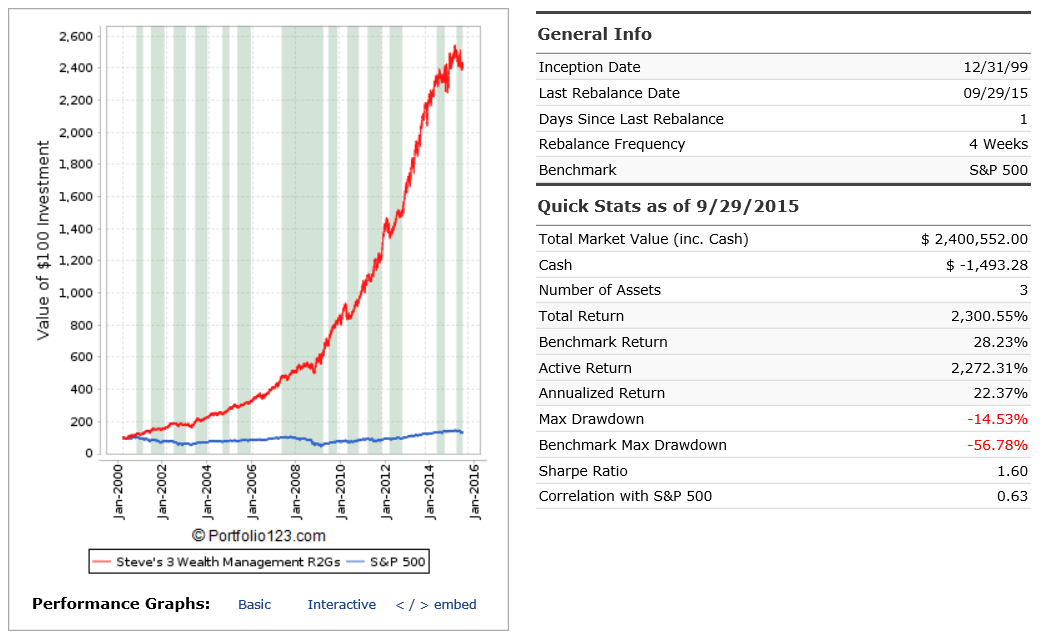

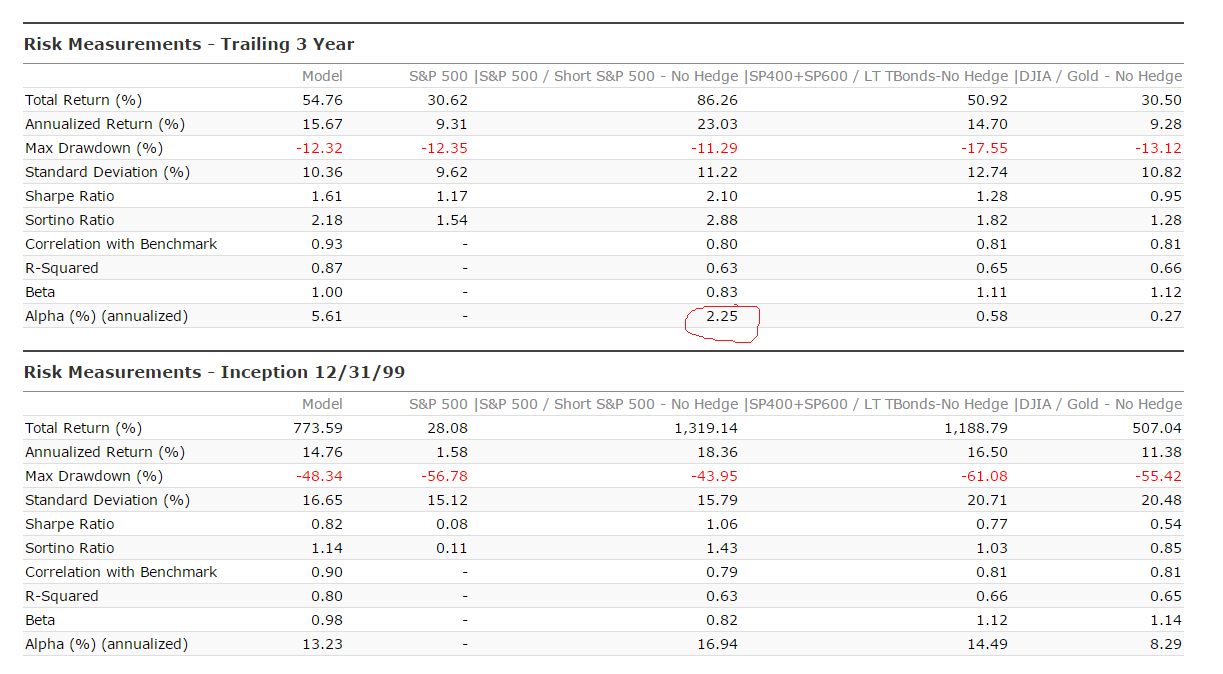

Denny. I saw these models. First two models. Very nice simulated performance (sharpe above 1, high liquidity, alpha etc). But out-of-sample alpha that I’m looking for is only 2%-6%. It doesn’t show consistency with sim performance.

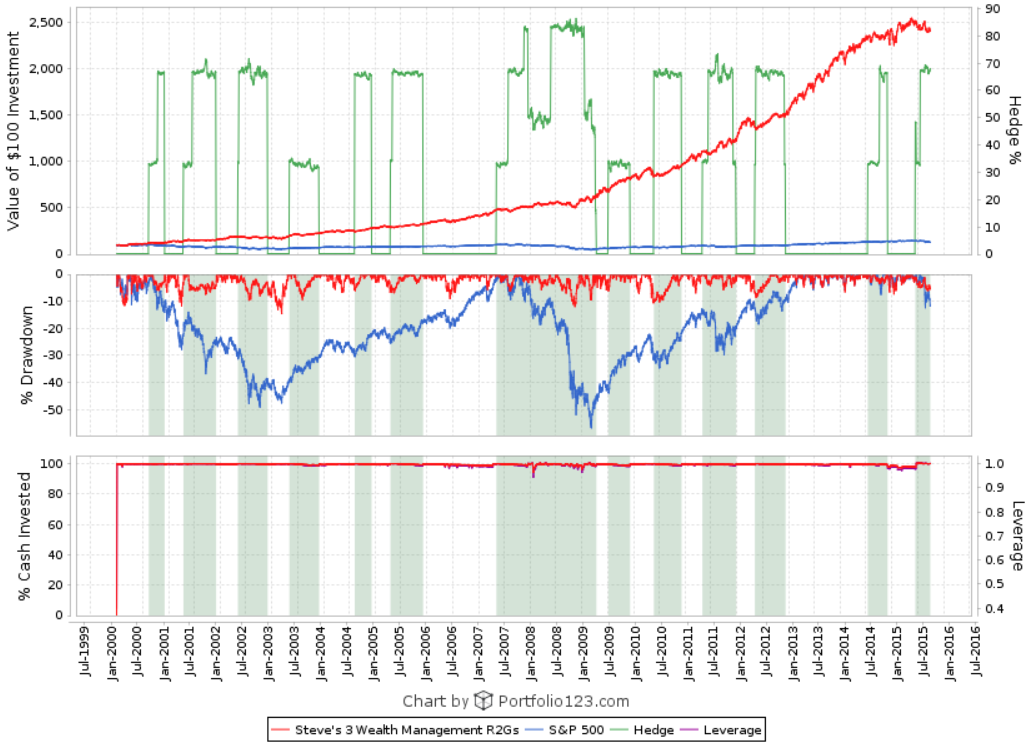

Third model shows outstanding out-of-sample results but relies heavily on market timing rules (that’s not what I’m seeking in P123). Therefore generated alpha is not mainly due to stock picking strategy in this case. What do all these models show without any hedging (or lets say TLT constant hedging)? I think you can make very good forward working models assuming that it would be designed not for R2G purposes (I mean an obligation to show good simulated results for the past 16 years to the detriment of the future performance :).

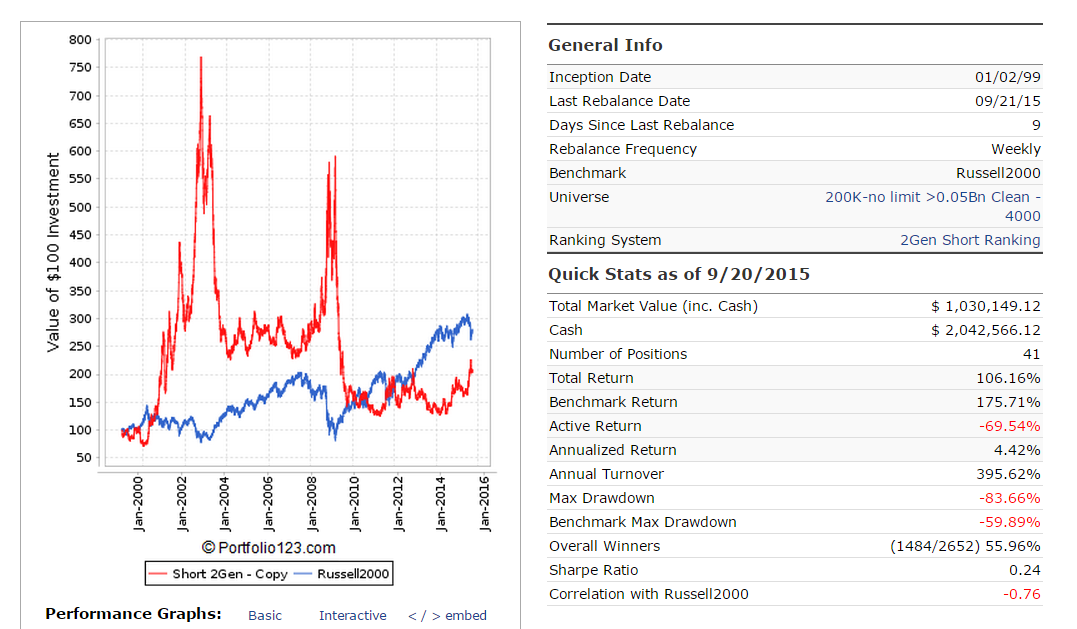

Dwpeters. Never saw this model. Is it private live? Could you please provide additional info about your system? It looks very interesting. I need additonal info.