Jim, I am a subscriber to ultra conservative. However I also subscribe to SZ and Stitts market neutral. All have strong points and weaknesses. That’s what strategy diversification is about.

Steve, A lot can happen to a quant strategy in 3 weeks, Remember we are suppose to be following the signals without developing a brain or an emotion. The daily signal to reduce exposure could occurr the 1st day of that 3week period and we all know what happened in the 1st 3weeks of Sept, and October and November 2008. That being said, SZ answer to that is a good one. Mutual funds tend to rebalance at the end of the month so it is wise to rebalance ahead of them. Like I said I am a subscriber to SZ and to your Market neutral S&P. I do not expect any strategy to be perfect or without downfalls. I have been at this a long time with some success, but beating the index is tough and doing that with market timing is tougher OS over a long period. Maybe impossible. Maybe because no one can hang in there long enough to get that small extra edge a simple timing strategy might produce. Mebane Faber has talked about this at some length. Short term timing is a fools game . Really most investors should not be timing at all. Its a graveyard of broken dreams. okay enough said.

John - we seem to have deviated from the issue, that only a few R2G models have beaten the S&P 500. As I have pointed out, there are lots of models that have… After reading Kumar’s statement again, I believe that he is referring specifically to smallcap models, which have generally underperformed in 2014. Reading between the lines, he’s upset because he didn’t get the 100% gain per year that he was expecting. Actual results are quite different than the promise.

We’ve never met and I do agree with many things you’ve said (but definitely not all).

Below are a few random notes based on some of your comments.

The biggest issue with 1 year rebalance is a) an insufficient number of holdings and b) maintaining an insufficient level of sector diversification. If holdings are 50 or more (possibly 30 if large cap spacE) and max. sector concentration is less than or equal to that of the broad index, I have found them to be stable over 3+ year periods. Below this, I have seen what you have.

The Dow Jones 30 is a weak form of ‘proof’ of this. It’s pretty close to an annual rebalance 30 stock large cap system. Not exactly annual rebalance, but fairly close (see:https://www.djindexes.com/mdsidx/downloads/meth_info/Dow_Jones_Industrial_Average_Methodology.pdf). It’s outperfomed the SP500 index with dividends, over the past 14 years with better risk characteristics. And it’s been around and done fine forever.

As far as avoiding month end rebalancing, you can fairly easily test this by creating a 100 (or 200) stock system choosing from the SP500 or R1000 or whatever universe you want and then using a random ranking, with trans costs and slippage set to zero, and a single sell rule, a forced sell based on the week of the month (i.e. MonthDay<=7 and NoDays>=28). Then run 20 (or more) iterations of it (use optimizer) and then average the results. There is no real statistically significant difference attributable to week chosen, at least for larger stocks (R1000) that I have tested. You will find differences on any single run, but if you run over the whole backtest period and run 20 or more iterations, the returns all converge.

Besides, mutual funds are, in aggregate, about average at picking stocks (about equal to dart throwing monkeys) and are generally not hedging or market timing, so they selling the same number of shares as they are buying at any point in time. Why would there be any effect?

But don’t take my word for it, run the tests. However, a 3 week rebalance also doesn’t achieve this ‘avoid month end’ desired result (as every 4th time the rebalance aligns with month end). A simple ‘week bracketing’ rule with in the sell rules with weekly rebalance would do this better.

As far as ‘market neutral’ and ‘timed’ or ‘hedged’ systems, the proper benchmark isn’t really the SP500, it’s some combination of stocks and bonds with a similar beta, st. dev and max dd. And/or a Barclay’s hedge fund index.

I’m on you side, as I think we can provide real alpha with P123. However, all R2G stats are currently close to meaningless, because R2G’s get deleted (for many reasons, but underperformance is a leading one). And there’s no way to estimate survivorship bias effects in the data.

There are also no easy ways to control for ‘true style indexes’ based on market cap or stock weightings or aggregate or other simple measures commonly used in benchmarking within the industry.

I have already spent 500+ hours over last 1 year to get knowledge thru forums and simulation in portfolio123, I agree i need to work hard 4+ more years to get more benefits from p123.

After following few micro and small cap R2Gs and intelligentvalue, i am not successful,

i have built my own simulation, it looks good. but previous failures on smallcap emotion is stopping me trade my own simulation;

in p123’s forum many of you suggested don’t trade with market open order on Monday it will gape-up or gape-down.

I. How, about trading micro & small cap (my own simulaton) on Fri day market close price?

(In simulation, friday close is 40% better than Mon day open)

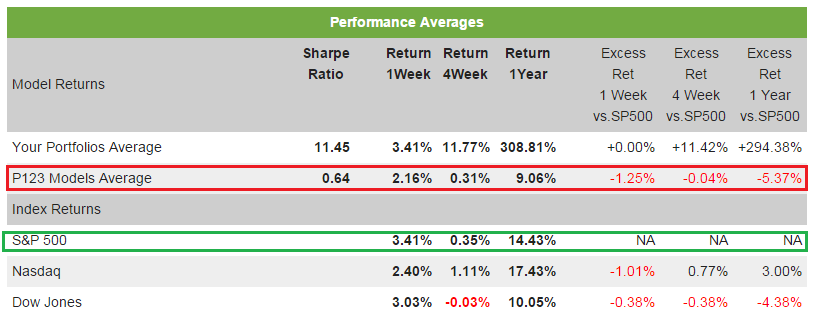

My concerns with Portfolio123 for this year performance (market is in bull)

a. S&P500 performance is better than Portfolio123 profile performance average.

(Screen shot is attached for the reference)

===========================================

I expect P123/Mgrstein/Steve/Denny and all real successful investor with p123 for 5+ years come up with 3 months manual pick holding strategy with big names as a shared R2G(20 stocks) similar to CNN 30 Technology stocks.

Beleive, it will benefit p123 subscriber with less experienced like me, it will raise the standard of P123 to next-level.

b. Foundation systems performance is better than Trading system in average.

c. Buy and Hold for a year well known market leaders are better than Foundation System (atleast for last 3 years)

(BRK.B, AAPL, GOOGL, AMZN, JPM, HD, BBY, HPQ, GS, AXP, WFC are able to double the money in 2 to 3 years since Jan 2012/Jan2013)

II. Any R2G/P123 systems has buy and hold for 6 months or 1 year strategy with 30% annual return ?

Biggest concern, I not able to decide to buy my favourite stocks (BRK.B, AAPL, GOOGL, AMZN, JPM, HD, BBY, HPQ,GS, AXN, WFC) during main market pullback (ie.,17th Oct and 16th dec 2014) using portfolio123.com tools.

III. Please, suggest, there is any way i am not aware of.

If you lower your expectations from the 100% + per year you spoke of earlier in this thread with significant rebalancing work or the 30% per year you spoke of in the last post with minimal rebalancing work to 10-20% per year with moderate rebalancing work then you will be satisfied rather than unhappy with p123. Obtaining a real 10-20% is much better than losing capital trying to make 100% or staying in cash.

I agree with the long term rebalance assumption except that the Dow 30 is more diversified than most R2G longterm rebalance and large cap stock ports. This to be expected in order to achieve alpha that we are all looking for. However in order to achieve alpha the risk has to go up by making the ports more concentrated. So what do we do as human beings, we try to take that risk off by hedging, timing, and leaving a hedge on untimed as in MN. All of these are not perfect . Timing assumes we can beat the random walk, again I repeat that is on shaky ground. Hedging assumes we can time we an index that mirrors our ports. Also shaky. Market neutral assumes that our port is directly correlated to the index and that our stock picking beats that index. That may or may not happen . There are mutual funds that are MN and there performance in general are small.

As far as the 3 week rebalance , all I said was that SZ reply was a reason he did it was his belief it was better to get rebalanced before the crowd and when I asked him to run the sim with a one week rebalance, it was almost the same DD and atr. This pretty much shows what you found over the long term . That however still dos’nt help the guy who bought into the market on Oct 1 2008 and rebalanced one month later at 17-20% lower. Assumming his port was not focused in financials and had a larger 1 month drop. I agree that the statistics sound accurate but the human emotion of selling panic could very well have over taken him.

Finally yes the MN would be better if it was not benchmarked to the S&P since they are always hedged. However , we still have to have a lot more OS to see if they will perform as excepted .

I’m not sure how you decided on this particular list of market leaders, but it is much easier to identify market leaders at the end of a period than at the beginning. If you are looking at the performance over the past 3 years, the question is what stocks would you choose at the end of 2011?

In any case, I took a quick look the results on stockcharts.com and get a return from 12/30/2011 of 97% for your list of stocks, 75% for SPY, 80% for RSP (equal wgt SP500), and 94% for QQQ. Assuming your list of stocks was selected with even a little hindsight bias, I don’t see a big edge there.

You could create a portfolio that buys an ETF on a pullback, or buys the stocks in your list on a pullback, or buys the stocks on your list on a market pullback. One problem with identifying a pullback is that if you want to have included Dec 16th, than you may have included Oct 2nd as well, and in hindsight that was not as good an entry. And if you are buying on a pullback, when are you selling? If you sell on strength you would likely have missed some of the broad market advance, when the market stayed overbought for some time.

Inspired by your post, here’s a quick presentation on the defensive sector pointing out some of the challenges in predicting forward period performance without really knowing ‘style index concentrations’ for casual retail investors:

Is the defensive sector really a good bet right now? Maybe, but there are some major risks. What do you think? I would be looking more at the energy sector if I wanted a sector bet.

Tom,

I will assume that because I subscribe to both SZ and Ultra Defensive R2G you are making this presentation to me to make myself aware or the risks of too much reliance on that one sector. I am also assuming that you want to show that the person devising a strategy that is heavily into healthcare has an immediate alpha above the S&P right from the get go without even being skillful . I was aware of where healthcare has done since 2009 . That does not mean it is way overvalued. As we all know the stock market in general and some sectors in particular can stay overvalued for longer than we believe, and stocks can stay undervalued for longer than your cash can hold out. The best example of this is the bond market. It has had an incredible 33 year bull market run. Does that men we should not buy bonds as a hedge. Those who bet against are still waiting. This is similar to the martingale betting system of doubling down on red or black on the roulette wheel when 3 reds or blacks come up in a row. The next roll will eventually come back to the opposite but the individual bet is still 50 / 50. You cant predict when it will revert back to the mean. Most people cant wait as the risk increases.

Again no strategy is without its pluses and minus. That is why it is better to diversify across sectors and strategies. Some would say maybe time frames also. Of course because of my previous statements you know I am not convinced of that. I am curious as to why you brought up energy. I own some energy but right now that is a contrarian play which is entirely another subject. Energy being a commodity is hardly defensive but those oil companies sure know how to make a profit and pay dividends in any climate. Now I am rambling.

If my assumptions about your post are incorrect please let me know.

There are numerous tricks that can be used to juice backtests without improving returns going forward. Other than what has already been said, I look at how the performance has been since launch relative to the backtest. That is another indicator of curve fitting.

As for market timing, the two systems that didn’t work for you seem to rely very heavily on timing. I understand that after getting burned twice you would like to write off timing altogether. But before you do so, please consider that there are different types of timing.

I divide timing into the following categories:

A. Shorting the market during timing signals.

B. Out of the market during timing signals.

C. Hedged during timing signals.

These different categories have completely different levels of risk. Shorting the market is like saying that you are sure that the market will fall. This is one way to juice backtests but it is very risky. If you are wrong in the prediction (and no timing system is 100% reliable) you can easily lose money both on your short and on the lost long opportunity if the market goes up. Since the market tends to go up most of the time, it is not a safe bet to be net short the market.

Being out of the market during timing signals does not risk losing money. It is like saying: “I don’t know if it is now a safe time to invest so I will stay out”. Although it does not usually risk losing money when wrong it still may underperform the market during bull markets as it whipsaws. This type of timing is often used (and has been used for decades) by trend followers such as Denny and O’Neil of Investors Business Daily to reduce risk. It is the best choice of timing for those who own high flying momentum stocks that tend to crash more than the market during corrections because hedging would still lose. The downside of this type of timing is that it may get whipsawed during strong bull markets and underperform.

The third type of timing is to turn on a hedge during timed periods. I use this type of timing in some of my portfolios to reduce risk during bear markets. I can afford to do this when even without the timer a system does about at least as well as the market during down markets. Therefore hedging is a win win situation: If the hedge turns out to be needed then it’s good for sure, but even if the market goes up during the hedged period then the system will beat the market and make something.

Another important thing to keep in mind when examining a hedged system is to see how well the system makes without the hedge. A system that relies on a hedge to make money is much more at risk of underperforming out of sample than a system that just uses a hedge to reduce risk.

It is something that needs to be cultivated, but it’s not so rare. Anything requires effort.

It takes effort to learn to invest. It takes effort to learn to drive a car. It takes effort to learn to cook. It takes effort to fly a plane. It takes effort to become an MD. It takes effort to become a software developer. It takes effort to be a parent. It’s hard to be an athlete (pro or recreational). Etc., etc., etc.

I can build p123 models and I can follow the market. But I still have no idea how to do things on Facebook. Does that mean Facebook is harder to master than p123 and the stock market? I very seriously doubt it. What it does mean is that I am interested in and care about learning to work with p123 and the market and that I have no interest in learning Facebook.

Aptitude is relevant, but to different degrees for different things. From what I’ve seen interacting with many successful and unsuccessful investors over several decades, I’d say that with investing, the aptitude required is much more widespread than is often acknowledged. Motivation and effort often trump natural talents. And I’m not talking about the sort of motivation one would expect of an investment professional. Lots of people are quite motivated and diligent in endeavors that have nothing to do with earning a living. Think of the degree of motivation needed to be capable at golf or tennis, widespread forms of recreation. Trust me, it takes a heck of a lot less grunt work to develop an understanding of how news events impact stock prices than it does to drive a golf ball and have it wind up within walking distance of the green.

That’s why I work with p123. I believe great top-quality tools and BS-free education can go a long way to helping people become successful investors. How successful? As with so many professional and non-professional endeavors, much depends on commitment and effort. And it doesn’t have to be all-or-nothing. At p123, for example, one can learn to be a great strategy designer. One can also learn to be a great R2G consumer.

As to being great at the markets, I can provide a good suggestion, but you’ll have to promise yourself to not react instantaneously and to approach it seriously – even though there will be enormous social pressure to act haughty and dismissive. Are you ready? Here it is: Go an Amazon and pick up (or download) and read some books by Jim Cramer. Yes, that Jim Cramer. The guy who shouts, flails, toots horns, rings cowbells, etc. on CNBC; the guy at whom everybody loves to thumb their noses. But don’t get caught up in that stuff. Cramer made his fortune running his hedge fund back when most people didn’t know there were such things as hedge funds and is now living large and having fun. But as dedicated as he now is to entertaining – others and himself – few who express thoughts publicly understand market behavior anywhere near as well as he does. And if you watch him on TV, you don’t have to agree with him; we’re forecasting the future so every human is going to often be off target. Focus instead on his thought process. Getting a feel for his process, and developing a basic understanding of what influences economies and stock prices can get you a long way.

I would be careful about well-known all-time favorites. They make for excellent conversation, but by the time they reach all-time-favorite status, their best days, in terms of return, are often done and gone and from that point on, it becomes a matter of hoping you’ll be able to get out before the market ditches them and moves on to the new group of all-time favorites, something many, especially those intrigued by all-time favorites, fail to accomplish. That’s why platforms such as p123 are so valuable – they help investors find stocks based on boa fide investment merit, as opposed to often ill-deserved reputation.

As to R2G, I think the most important thing you can do is manage your expectations. Be careful about high flying claims. It’s easy to time the market and generate 50%-plus annual returns in hindsight. Refrain from allowing yourself to be impressed by designers who are good at predicting the past. Focus on live performance (out of sample, post launch).

Inspiration and ideas comes from successfull investors of p123.

Most of the portfolio123 ranking systems favours the small caps.

Believe, no surprise people new to p123 addicted to smallcap until explore the other avenues.

I ran all the portfolio123 ranking systems with large cap > 5B market capital and AvgTot(60) > 20M$, most of them returning 10-12%(in top 2 percentile from the ranking system).

Any one can suggest ranking systems, which favours large-cap and medium-cap from public simulation/public screens or public community to start with ?

my email: asis.skumar@gmail.com

Kumar - I have just made public an S&P500 simulation for the staples sector. I developed it a couple of years ago (with 3 month rebalance) and it has continued to perform. There are no buy/sell rules and the sim “works” with 3/6/12 month rebalance. You can start with this and build on it if you wish. Please keep the “Stitts” name in the title.

Scott - I turned the sim private again as I don’t want to find my tax smart models (Stitts Defensive Sectors (Tax Smart)) competing against my own work if you know what I mean. If you made a copy, can to make it private?