https://www.portfolio123.com/port_summary.jsp?portid=1441858

Where can I find this model? Do you have a link?

I think I understand what you mean by diversification. But any danger to reduce overall alpha by mixing it up?

Help>Tutorials>Walk Through Guide. On this site. But this is just an example that you probably will not use, ultimately. Something I happened to be looking at recently in a book: it did reduce my drawdowns. I’m not using it now.

Reducing the volatility (Beta) should improve Alpha shouldn’t it?

Thanks I’ll take a look.

The funny thing about Alpha is that it is implied that it increases with higher Beta. But my experience is that a higher Beta actually decreases returns…an anomaly.

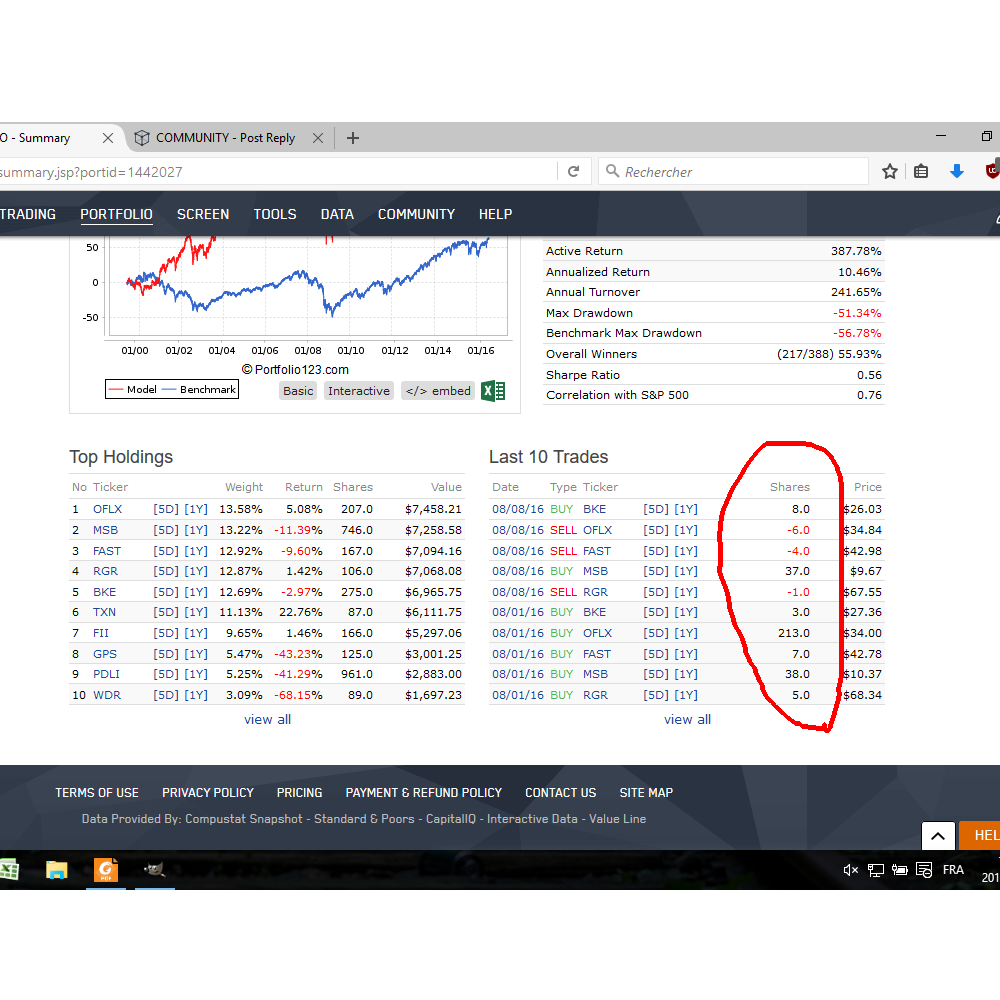

I tried the tutorial. Very interesting stuff. When running a simulation, however, I still get "Buy/Sell Difference " rules forcing me to buy like 6 shares at 30$ each of a company. I wonder how to get rid of this. Still, this is interesting.

Another thing I saw is that returns are down after 2013. Does it mean that quantitative system accessibility is making market more efficient?

The reason for the "Buy/Sell Difference " is in your buy/sell-rules:

Because you exclude some industries/sectors in the buy-rules, it can happen that the best ranked stocks are in these industries/sectors. So some of your holded stocks get below the sell-rank (and should sold) but also fulfill the buy-rules (and should be re-bought). Instead of process both transactions, the simulation buys/sells only the diff.

You can solve the problem, if you move your buy-rules to the universe-rules.

If you have a rule to sell if the Rank <97, then add a buy rule Rank>=97. This should eliminate the buy/sell difference transactions.

I’ll give you an absolute definitive “maybe.”

First, don’t focus on returns. No matter what we do, the most important factor is the market itself. Everything we do works at the edges. So if the market is weak, expect returns to be weak. We’re doing well if our returns are less weak. To try to defeat the market, we’d need to work with market timing (easy in simulation but difficult in reality because historical samples are not necessarily representative of the circumstances that will drive the next bear market) or a multi-asset approach (think in terms of a p123 “book” of models, some stocks and some etfs that offer different kinds of exposures).

We also have to be aware that the wold does change and one change we’ve seen in large measure has been the increasing use of automated tools since the beginning of our 1/2/99 sample period. While many members wish the sample could stretch back further in times and can cite much statistical authority in support of their views, I find the early part of our sample (1999-2005) largely useless and show it only when I must for cosmetic reasons. But, although we can’t assume early-winner models will still work due to crowded trades . . .

From what I’ve seen in the serious investment quant community, we’re years or decades away from having too many automaters completely wipe us out. To the extent they work with fundamentals at all (many don’t) they tie themselves to a Fama-French APT structure which we can use if we want but which is actually not all that good (and that’s why so many announce that they are passive indexers) and completely misses the boat on suc h things as why some value stocks work and others don’t,etc. etc. etc. Perhaps our best protections are the enormous emotional and ego-based investments the quant community has made in its approach . . . while they have the heft and technology to crowd out even the best of pour current ideas, they are probably at least a generation away (if not more) from having the emotional capacity to do it.

I feel like I should understand this, but for some reason I don’t. What do you mean by: “You can solve the problem, if you move your buy-rules to the universe-rules”? I already use a custom universe… I understand the part about ticker XYZ getting sold and rebought and it’s rebought for a little higher number of shares then sold. But wouldn’t it be possible to jut leave it alone: if it’s still in buy zone, don’t buy more, just leave it alone…

I made another simulation from the tutorial and it’s ridiculous: the model makes me buy/sell 1 to 3 shares. With 5$ per trade that’s like 10% right there, lol… In this simulation, I didn’t use rank to sell, but rather I simply switched numerators from buy side: e.g. Payratiottm<100 for buy and Payratiottm>100 for sell.

Precise rules are :

BUY

IndWeight < 30

PctAvgDailyTot(20) < 10

Frank (“Yield”) > 50

Payratiottm<75

FRank(“DbtLT2EqQ”)<50 OR FRank(“(DbtLT(4,QTR)/EqTot(4,QTR))/(DbtLT(0,QTR)/EqTot(0,QTR))”)>50

SELL

Frank (“Yield”) <= 45

Payratiottm>=95

FRank(“DbtLT2EqQ”)>=65 OR FRank(“(DbtLT(4,QTR)/EqTot(4,QTR))/(DbtLT(0,QTR)/EqTot(0,QTR))”)<=35

UNIVERSE = Prussell 3000 with YIELD > 0

So how will the market work then? Will it finally be efficient since any advantage that could be found has been found? Why should we continue to look for alpha if it’s a losing fight?

I believe, like you do, that data from 1999 to 2005 is nearly worthless (but I still use it at first, then I look for 2011-2016 approx.). A lot of things have changed… Strategies that worked well does not work that well anymore it seems.

FRank(“DbtLT2EqQ”)<50 OR FRank(“(DbtLT(4,QTR)/EqTot(4,QTR))/(DbtLT(0,QTR)/EqTot(0,QTR))”)>50

Should be:FRank(“DbtLT2EqQ”)<50 AND FRank(“(DbtLT(4,QTR)/EqTot(4,QTR))/(DbtLT(0,QTR)/EqTot(0,QTR))”)>50

There may be something else, in addition, but you want AND in the buy or just make them separate rules.

If you like the or in the buy rule–and want to keep it–you must make it AND in your sell rule. Or accept the buy sell difference.

When a stock is sold, it may be rebought if it satisfies the BUY rules, has sufficient high rank and ‘Allow sold holdings to be re-bought at current rebalance’ is set to Yes.

Cash available from a sell is allocated to a new position in a way that satisfies the equal weight algorithm. If a stock is rebought, it may result in a small adjustment of the number of shares held.

At least, that’s what I think is happening.

The way around these small adjustments is to instantiate your portfolio in a book. Book support minimum rebalance transaction thresholds.

Best,

Walter

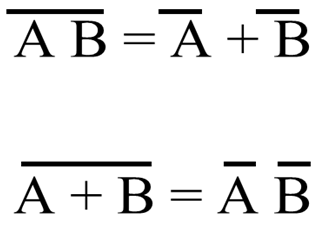

Thanks, it seems to work! In the tutorial they said to put “OR”. What’s the difference with “AND” ?

How do you do that?

Louis,

It is a logic thing. Like if I will hire someone if she has blond hair or is over 6 feet. But I fire her if she does not have blond hair or is not over 6 feet.

That poor 5 foot 2 inch blond has a high turnaround. “And” in the hire (buy) rules causes me to never hire her. “And” in the fire (sell) rules causes me to never fire her. Until she colors her hair or grows.

When in doubt use De Morgan’s Theorem;

That’s the number one thing I’ve found, and my advice to a newbie. Even when the model performs well out of sample, it’s never easy money. Those upward sloping backtested curves are very pretty, but those are from a 30,000 foot view with hypothetical money. They’re not as pretty in real life in the day to day. I agree with Marc’s comments earlier in the thread. Even if the market gets proliferated with robust quant tech, the emotional and pysychological adjustment to stick with a model over the long haul will take a really long time.

Thanks, great example, I understand.

I agree… As an example, I used the model in the tutorial and tried optimization. If I switched some variable by some numbers, the results changed a lot and even got negative. It’s very difficult in the end not to be curve-fitting.

Not sure what you mean by: “the emotional and pysychological adjustment to stick with a model over the long haul will take a really long time.”