To a large extent this is what was easy with the designer model downloads and not necessarily the best method for predicting returns. Still…

There is an interesting discussion about Backtests here: Why the poor live results versus backtesting?

This is related but a slight different topic. So I started a new thread. Summarizing the previous thread, and maybe over-simplifying when doing so, it may be fair to say there is a complex and not fully understood relationship between in-sample and out-of-sample results. Some have suggested that backtested results are not important for predicting future returns. I tend to agree with that.

In any case, that leaves open the question: How do we pick a model? Maybe we want to look at the relative performance of backtests, use validation sample results,, test sample results or even just look at the out-of-sample results of a live port for picking a model?

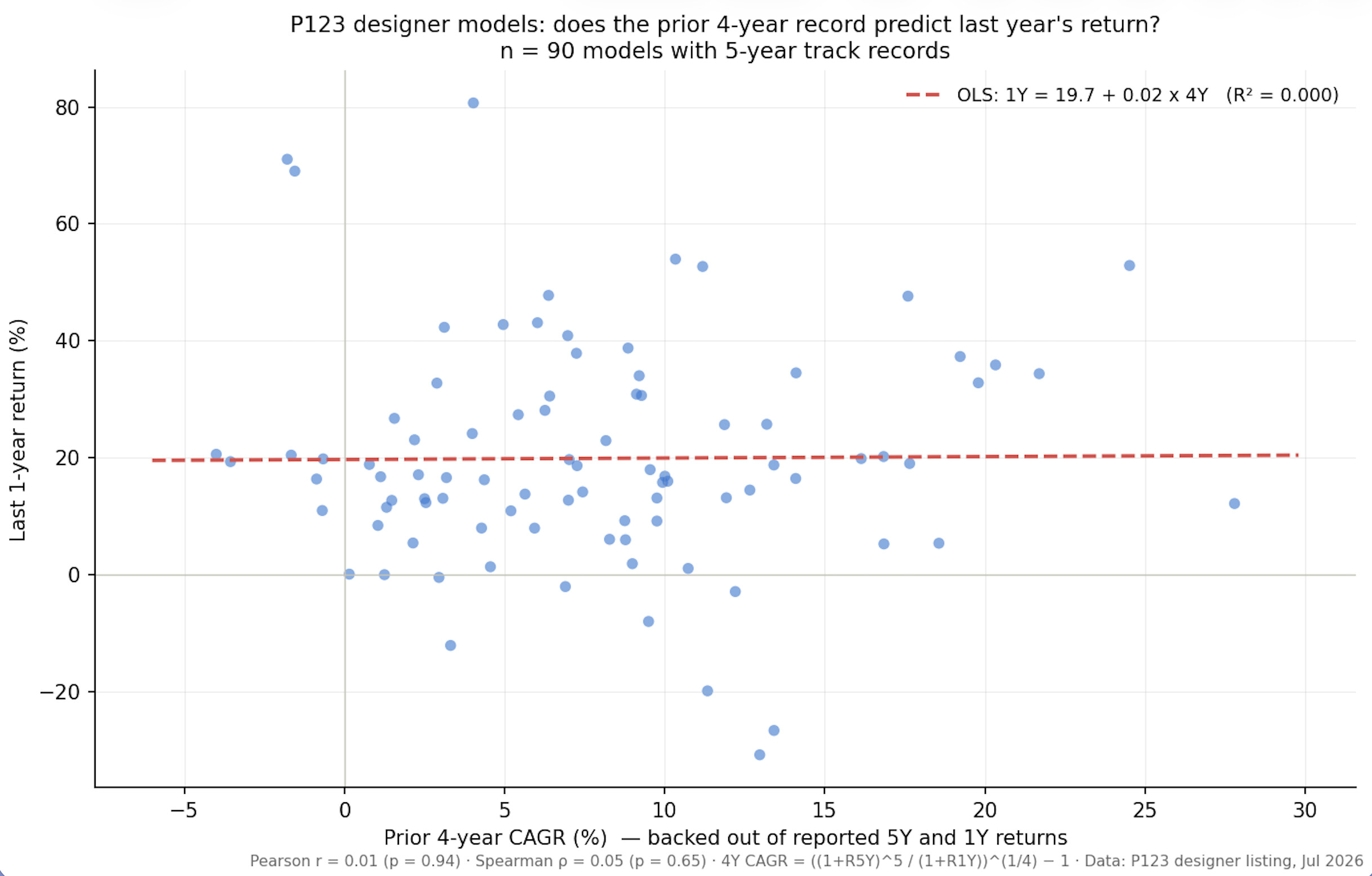

So lets try the last. I had Claude Fable 5 help me with this. But with download from the designer models of the 1-year and 5-year returns we already have the 1-year returns and the previous 4-years can be calculated from that data. And a clean graph and R^2 or coefficient of determination can be obtained.

Conclusion: Somewhat surprising to me. Enough to be without words at this time. Maybe someone else has comments. Maybe the possibility of survivorship bias is worth mentioning, but otherwise without comment: